The shortages have led Tesco, Aldi and Asda to limit purchases to three units per person in the UK while Morrisons has introduced a cap of two. Asda has gone the furthest with restrictions across tomatoes, peppers, cucumbers, lettuce, salad bags, broccoli, cauliflower and raspberries.

The UK’s Department for Environment, Food and Rural Affairs has insisted the country has a “highly resilient food supply chain” and that other countries are experiencing similar disruption.

British shoppers have shared images of empty shelves on Twitter while on the continent consumers in France, Netherlands, Spain, Italy and Bulgaria are showing photos and video tours of supermarkets with plentiful supply. On Thursday morning #BrexitFoodShortages was trending on Twitter.

However, Irish stores also have a shortage of some fruit and vegetables stemming from Spain and north Africa and retailers are looking at alternative sources of supply.

In Denmark, the second-largest supermarket chain Coop is short of cucumbers, tomatoes, lettuce, bell peppers and aubergines due to lower deliveries from Spain, though the grocer hasn’t started rationing. Another chain in Denmark, REMA 1000, has similar shortages and expects the issues to persist for several weeks.

There have been reports of higher prices due to supply constraints in the Netherlands, but Binard from Freshfel Europe insisted “there are not really any significant shortages” in the country, nor in France, Germany, Italy or Spain. “There may be a little bit less volume at a higher price,” he said. “But nothing is missing.”

In Sweden, supermarket ICA Gruppen is finding it challenging to get full volumes of fruit and vegetables but the situation is manageable, said Jonas Andersson, head of fruit and vegetables at ICA Sverige.

In the UK, it’s the second instance of widespread rationing in the space of four months. In November almost every major supermarket capped purchases of eggs after the higher cost of chicken feed and an outbreak of bird flu led to a dearth of supply.

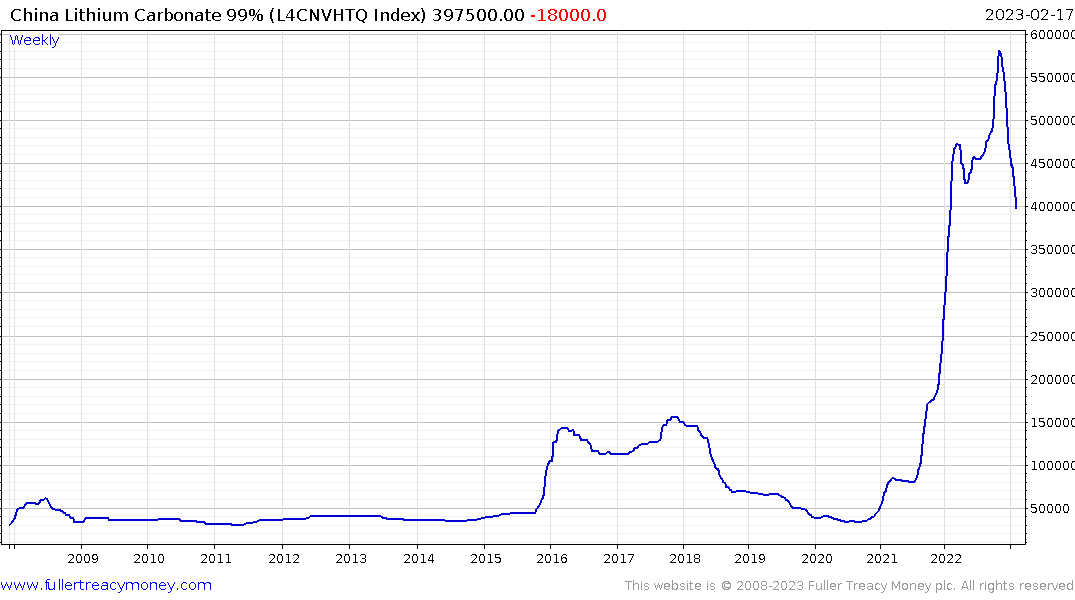

Eoin Treacy's view - There are obvious efforts to lay blame when consumers cannot buy the products they are accustomed to having access to. However, the fact many of these plants are grown in greenhouses. In colder countries those greenhouses need heating and we have just been through one of the most uncertain winters in history from an energy availability and cost perspective. As natural gas becomes truly globally fungible, that will be less of an issue in future.

This section continues in the Subscriber's Area.

Back to top