The Overlords of Finance

Thanks to a subscriber for this article by Danielle DiMartino Booth which may be of interest. Here is a section:

Well ain’t that a thing! Now we know why the dialogue shifted just after former chair Ben Bernanke made his way out the door in January 2014. The exit from unconventional monetary policy, you may recall, was originally set to begin with the tapering of purchases, being followed by allowing the balance sheet to run off and then prompt the first rise in interest rates – in that order.

A funny thing happened on the way to the exit, though. Bill Dudley is not only the president of the Federal Reserve Bank of New York but also the vice chairman of the Federal Open Market Committee and coveted holder of a permanent vote. Back on May 14, 2014, in a question and answer session with reporters following a speech, he literally stood the preexisting exit principles on their head.

“Delaying the end of reinvestment puts the emphasis where it needs to be — getting off the zero lower bound for interest rates,” explained New York Fed president Bill Dudley. “In my opinion, this is far more important than the consequences of the balance sheet being a little larger for a little longer.” Luckily for investors in any and every risky asset, his opinion holds a lot of sway. Dudley’s central banking peers in developed countries have followed his lead and peace on earth has held ever since.

As for those pesky financial stability concerns, we’ve been instructed to look the other way. Some have even gone so far as to suggest that the time has come to devise a new term to replace ‘bubble.’ No doubt, it’s an unseemly word given the nasty images it conjures. But what if the word ‘bubble’ is not substantial enough to capture what’s been created before our very eyes, across the full spectrum of asset classes?

This article offers an erudite exposition of the problems residing in the fixed income markets and the extent to which leverage now plays a role in just about all asset classes. The simultaneous asset price inflation of the stock, bond and property markets, particularly since 2011, is a testament to the fact that a potential problem is brewing.

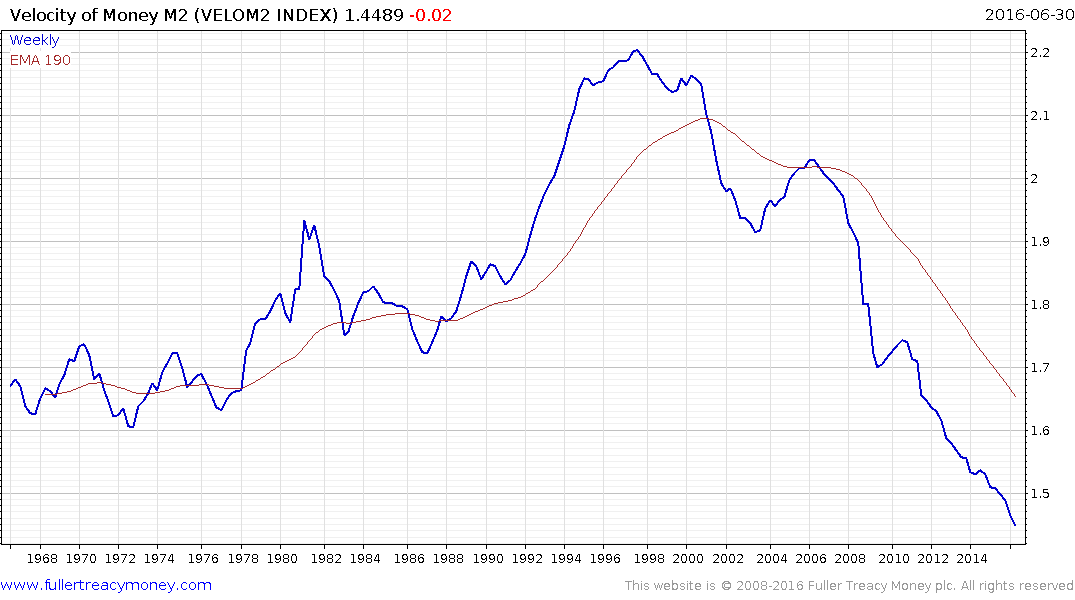

The Velocity of Money is on a steady downward trajectory, and in fact has been declining since 1997. That goes a long way towards explaining why monetary policy has been so easy and why central banks are reluctant to withdraw the additional liquidity from the market. The only reason a problem might arise is if the status quo changes.

I suspect the reason so much alarm is being sounded in the bond markets at present is because the Fed is talking about how uncomfortable it is with the perceived complacency of the bond market. This has raised the hackles of bond traders because they had enjoyed a powerful momentum trade; riding on the coattails of Fed purchases and rollovers.

By raising interest rates the Fed is sending a signal to the bond market that it is willing to tolerate higher refinancing costs for the massive quantity of bonds on its books, that have a duration of around 6.5 years. This might be construed as its belief that the economy is strong enough to tolerate higher interest rates which is positive for the stock market and the banking sector overall. However it also suggests that the Fed wants to target some of the leverage in the financial system. Raising interest rates means margin gets more expensive so positions sizes cannot expand as rapidly which is a headwind for the same assets. .

An additional factor is that because interest rates are so low, coupons have contributed relatively little to total return for bond investors. The surge in prices has been the primary contributor. In order for total return to continue to trend higher, prices would have to come down no faster than yields rise.

As bond investors begin to do the calculations a 25 basis point hike is a 50% increase in the base rate. Therefore convexity (the sensitivity of price/yield to interest rates) can be expected to be high at these levels. Convexity, as a risk factor in bond pricing, has been absent for a decade but I suspect we are going to be hearing a lot more about it if the Fed continues on its path to raising interest rates.

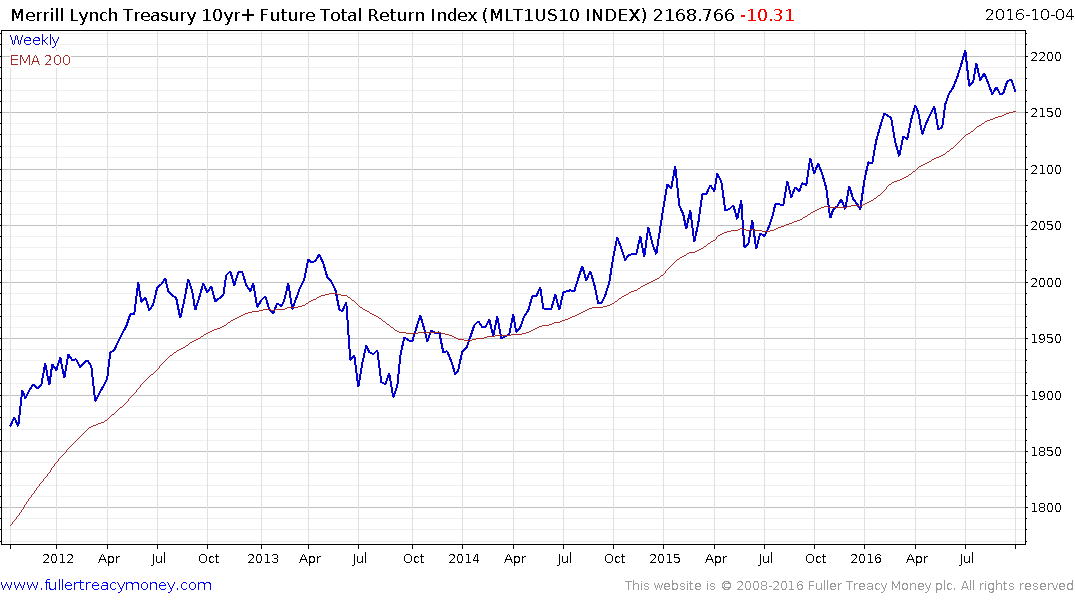

With yields having bounced back for the last five days the Merrill Lynch 10-year Total Return Index is back testing its 200-day MA. A sustained move below it, subsequently encountering resistance at the MA and breaking to a new low will be required to signal a completed top in what is perhaps the most persistent bull market in history. That is the most likely scenario for an eventual ending but it should also be pointed out that the Index has yet to even drop below the MA on this pullback.

It also occurs to me that the same bond investors who are now worrying about a change to the status quo were highlighting the risk of recession (bond positive) not so long ago. Therefore the consistency of the above chart is really the only arbiter of investor actions.