BHP Billiton: Oil a benefit not a drag

Thanks to a subscriber for this report from CIMB which may be of interest. Here is a section:

The world isn’t ending after all

BHP’s share price has risen 28% so far in 2016, versus a broader market that has largely stalled (ASX 200 up 3%). Although sizeable gains have already been posted, we expect we are still in the early stages of a significant upgrade cycle for the resource sector. For the majority of the year we have been at the top of consensus on BHP, on the belief that expectations had become unrealistically pessimistic on commodities/miners. This thematic of an impending ‘relief rally’ across commodities continues to play out, with oil and bulk resources (coal and iron ore) the key gainers.Oil adds x-factor to cash flow upside

While we have already seen a significant recovery in oil prices so far in 2016, we expect there is still further upside potential. OPEC’s decision to announce an output cut of 750kbopd is important fundamentally for oil given it indicates that OPEC’s strategy to defend market share by squashing oil prices has essentially been accomplished and the cartel is returning to its traditional role of supporting oil prices as a swing producer. We expect the downturn has caused permanent damage to US shale’s ultimate potential.Petroleum investor briefing

BHP’s petroleum team is conducting an investor briefing in London on 5 October and Sydney on 10 October. The briefing will provide significant detail on BHP’s petroleum strategy (both conventional and onshore), which has been in a state of transition from gas to liquids. In particular, we expect a lot of focus to remain on BHP’s US onshore assets, where its cash flow performance has been pressured by depressed oil and gas prices.Good mix of exposures to ongoing recovery

Our preference for BHP amongst our large-cap Australian resources coverage is driven primarily by the cash flow upside potential it holds from recovering volumes and commodity prices in FY17. We see the big miner as being ideally positioned to pursue growth at the low point in the cycle while supported by a strong balance sheet and the potential for additional upside in near-term cash flow. We maintain our Add recommendation with an unchanged A$25.30 price target. The key risk to our call is commodity price risk.

Here is a link to the full report.

The performance of the FTSE-350 Mining Index and the S&P/ASX 300 Resources Index has been broadly similar highlighting the broad based appeal of the mining sector this year. It is also notable that the performance of the industrial metals has been considerably less volatile of late than the precious metals, which highlights the quiet different internal dynamics of the respective markets.

The London Metals Exchange Metals Index broke out to a new recovery high last week and has paused this week. A sustained move below the trend mean would be required to question medium-term scope for continued higher to lateral ranging.

BHP Billiton (Est P/E 24.13, DY 1.81%) has benefitted from the strong rebound in its primary markets namely oil, iron-ore and coal. Copper, which represents over 20% of revenue has been a laggard so far and will need to sustain a break to new recovery highs to signal a return to medium-term demand dominance.

BHP Billiton (Est P/E 24.13, DY 1.81%) has benefitted from the strong rebound in its primary markets namely oil, iron-ore and coal. Copper, which represents over 20% of revenue has been a laggard so far and will need to sustain a break to new recovery highs to signal a return to medium-term demand dominance.

South 32 (Est P/E 21.63, DY 0.53%), which was spun off from BHP Billiton last year primarily focuses on aluminium, both thermal and coking coal, and manganese. The share has been trending higher all year and the pace of the advance has picked up of late, so some consolidation is looking increasingly likely.

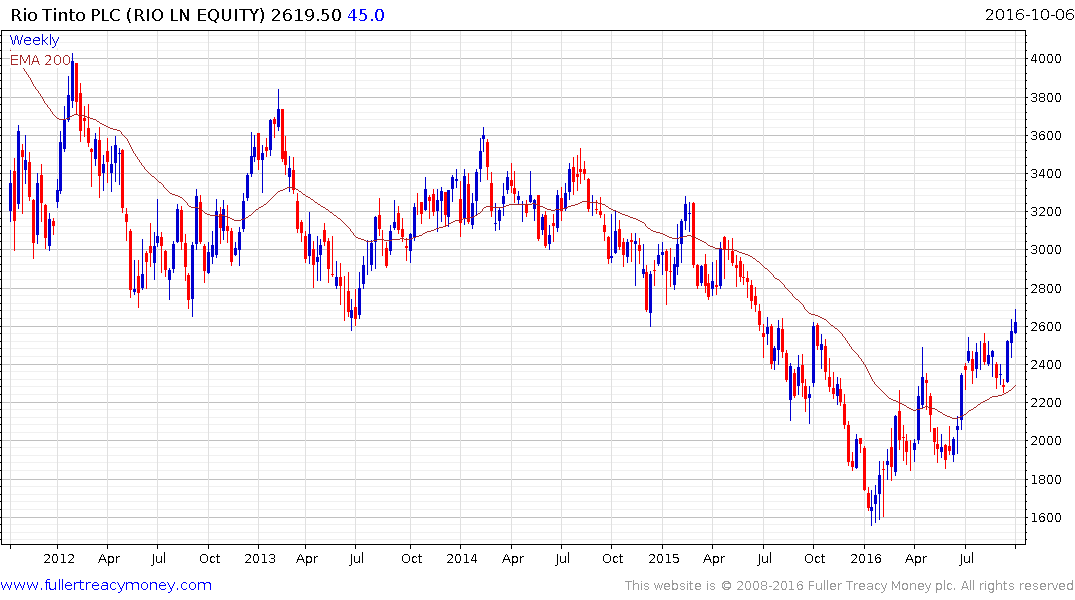

Rio Tinto (Est P/E 15.64, DY 4.12%) found support in the region of the trend mean from three weeks ago and a sustained move below it would be required to question medium-term recovery potential.