Tapping into growth

Thanks to a subscriber for this report from Deutsche Bank focusing on European brewers. Here is a section:

Beer takes share from a readily addressable market in the form of cheaper, often illicit and non-commercial alcohol. The level of local alcohol in a market is strongly correlated to national income as per Figure 9.

This readily available market accounts for over 50% to 90% of alcohol consumption in Africa, with growing markets like Nigeria, Democratic Republic of Congo and Ethiopia particularly attractive. Other emerging markets have lower, but nevertheless interesting figures which range from 15% to 40%. Markets like Latin American Ecuador and Peru and Asian markets such as Myanmar and Cambodia looking interesting to the brewers.

Beer is a luxury

The barrier to conversion from illicit alcohol to beer is the affordability of beer. Per capita consumption in a market is relation to the amount of time a consumer has to work to afford a beer. As seen in Figure 11, the first inflection point for growth acceleration is around 120 minutes of work to afford a beer.A second inflection can be found at 30 minutes worked for a beer. Not only does beer consumption accelerate to the levels seen in developed markets, consumers also move up in the portfolio towards more premium brands.

There are market dependent limits to per capita growth

There is a limit to how much alcohol and beer one can drink. For beer, the per capita average of 10 liters of pure alcohol translates to 200 liters which approximates consumption in core beer markets such as Germany and Czech.?As markets mature, our analysis indicates a range of 70-90 liters per capita being the developed market norm over time. For most emerging markets with favorable population and illicit alcohol profiles, this is a growth destination; for developed markets this may translate into more declines.

Here is a iink to the full report.

The last few paragraphs above highlight just how important international expansion is for larger brewers. The profile of consumption in emerging middleclass economies represents where they have the best potential to grow their businesses. The pace of M&A activity within the sector highlights the fact that international expansion and establishing brand loyalty remains a priority.

Heineken’s acquisition of Asia Pacific Breweries in 2012 represented the company’s efforts to increase its footprint in Asia. Diageo already has a substantial Asian operation and maintains a number of listings in Africa which represents another potent growth region. An issue for brewers is that their shares are generally priced for growth so they will need to continue to succeed in their objectives to justify the valuation.

Heineken (Est P/E 18.21, DY 1.66%) continues to rebound from the January low near €45 but it will need to demonstrate support above €50 if potential for higher to lateral ranging is to continue to be given the benefit of the doubt.

SABMiller (Est P/E 21.21, DY 2.11%) has a relatively similar pattern.

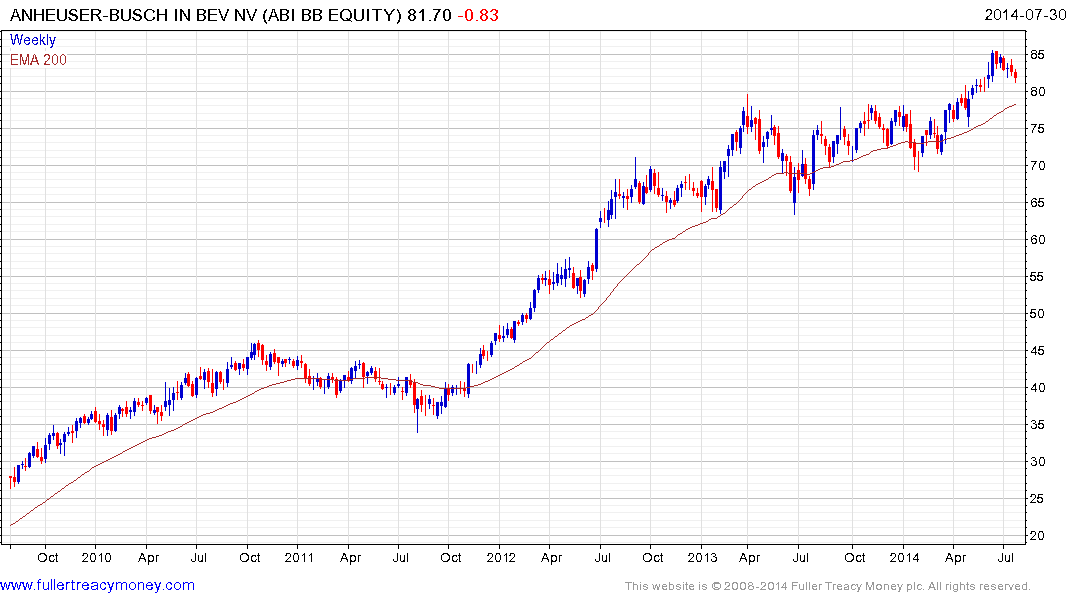

Anheuser Busch InBev (Est P/E 20.63, DY 3.55%) broke out of a yearlong range in May and is now returning to test the upper side. A sustained move below €78 would be required to question medium-term potential for continued higher to lateral ranging.

Diageo (Est P/E 18.29, DY 3,04%) has posted a progression of lower rally highs over the last year and encountered resistance in the region of the 200-day MA from May. A sustained move above 1900p will be required to offset top formation completion characteristics.

Back to top