If Not Normal, Where Are We in the Cycle? Late

Thanks to a subscriber for this note from Wells Fargo which may be of interest. Here is a section:

Credit Standards: Move to Tighter Standards

Over the economic cycle, banks adjust their lending standards but, unfortunately, the dynamic adjustment of credit standards appears to impart a very pro-cyclical bias to the credit cycle. From the middle graph, we can see that the percentage of banks that tighten credit drops dramatically in the early phase of an economic recovery (1992-1994, 2002-2004, 2010-2011) and remains low for most of the economic expansion. Then the percentage of banks that tighten credit rises sharply just before a recession (1999-2000, 2007-2008). This credit cycle, while certainly rational from an individual bank’s point of view, becomes quite pro-cyclical when viewed in the aggregate. We have entered the tighter credit phase of this cycle.For Whatever the Reason: A Flatter Yield Curve

Ever since the taper tantrum in 2013, there have been two distinct moves in the yield curve as illustrated in the bottom graph. The long-end of the yield curve has exhibited a bullish flattening trade with the decline in the 10-year/two-year spread. This reflects the yield pick-up for U.S. Treasury debt relative to what is available for investors in Europe and Japan, while also reflecting the incentive of a stronger dollar to attract foreign inflows. Meanwhile, the short end of the yield curve reflects the anticipation of a FOMC increase in rates or at least some form of tighter policy going forward.Uncertainty in financial markets provides the motivation for two distinct

moves. First, investor uncertainty at the global level has prompted a safehaven move into U.S. Treasury debt. Meanwhile, uncertainty on the economic outlook limits the extent of Fed tightening of policy as well as the private market discounting of future fed funds moves.

Here is a link to the full report.

With interest rates so low there is very little margin for error when trading in bonds and not least when so many are sporting negative yields. An increasing number of seasoned bond investors are expressing emotions ranging from caution to fear and frustration at the destabilising influence of central bank policy on the markets. They are in a difficult position because pre-empting an end to the 35-year bull market has resulted in underperformance while overstaying one’s welcome, when it eventually does peak, will result in ever larger underperformance.

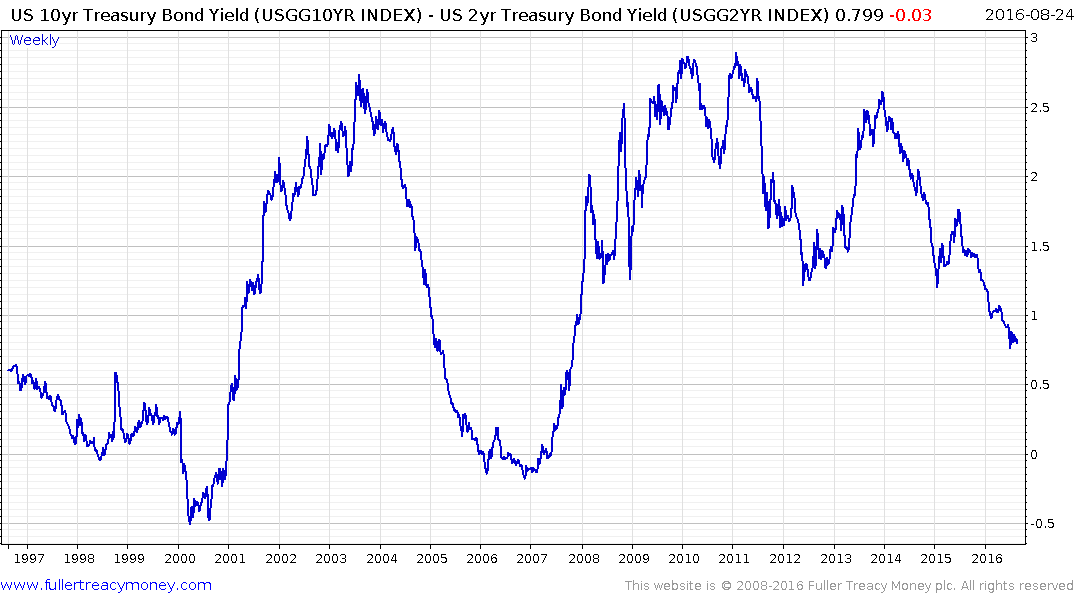

The US yield curve spread (10-year – 2-year) has contracted from 250 to 79 basis points since 2014 and continues to trend lower. There has been much debate about whether an inverted condition, when it trades below zero, will have the same efficacy as a predictor of recessions, the next time it occurs, because interest rates are already so low.

There are two arguments to support the view it will remain an important Rubicon for investors. The first is simply why on earth would one borrow short to lend long when there is a certainty of losing money. If the yield curve is inverted you have an incentive to do the opposite which increases interest rate risk and that is something which has been largely absent for nearly a decade.

The second is to employ a lesson from the equity market. When central banks eventually raise rates, in an effort to withdraw the punchbowl, it raises the cost of leverage which retards the ability of traders to increase positions. That withdraws a source of demand from the market and contributes to top formation development. There is no reason to believe that a similar process cannot playout in the bond markets when central banks remove support.

.png)

US Treasury yields hit a new all-time low in July and a process of mean reversion is now underway. However a sustained move above the trend mean will be required to signal a return to supply dominance.