Goldman Sachs Sees More Value Outside of Stretched U.S. Stocks

This article by Michael P. Regan for Bloomberg may be of interest to subscribers. Here is a section:

How stretched is too stretched? Who knows. At Goldman Sachs, Kostin and company believe things are as stretched as they’re going to get on the macro level. In their view, the S&P 500’s price-to-earnings ratio should contract as the Fed begins to raise interest rates in September and the index will end the year at about 2,100, right around where it is now.

“The proverbial ‘smart money’ is selling, not buying,” they write, adding that completed private equity sales through mergers and acquisitions and follow-on offerings have reached record levels.

Investors looking for more attractive valuations need to go outside the U.S., according to Kostin’s team, provided they use currency hedges. (That seems to be a popular trade du jour, given the surging popularity of the WisdomTree Europe Hedged Equity Fund.) Goldman is forecasting 12-month, local-currency returns of 19 percent for Japan’s Topix Index, 17 percent for the Stoxx Europe 600 Index, where central bank easing is about to heat up big time, and 15 percent for an index tracking Asian nations besides Japan.

I’ve heard the sentiment expressed that US valuations are stretched from a number of sources over the last few weeks. Everywhere from the media to dinner with friends I hear the same thing which suggests people are worried. Bonds have done spectacularly well and yet we do not hear that valuations are stretched. I find the divergence interesting.

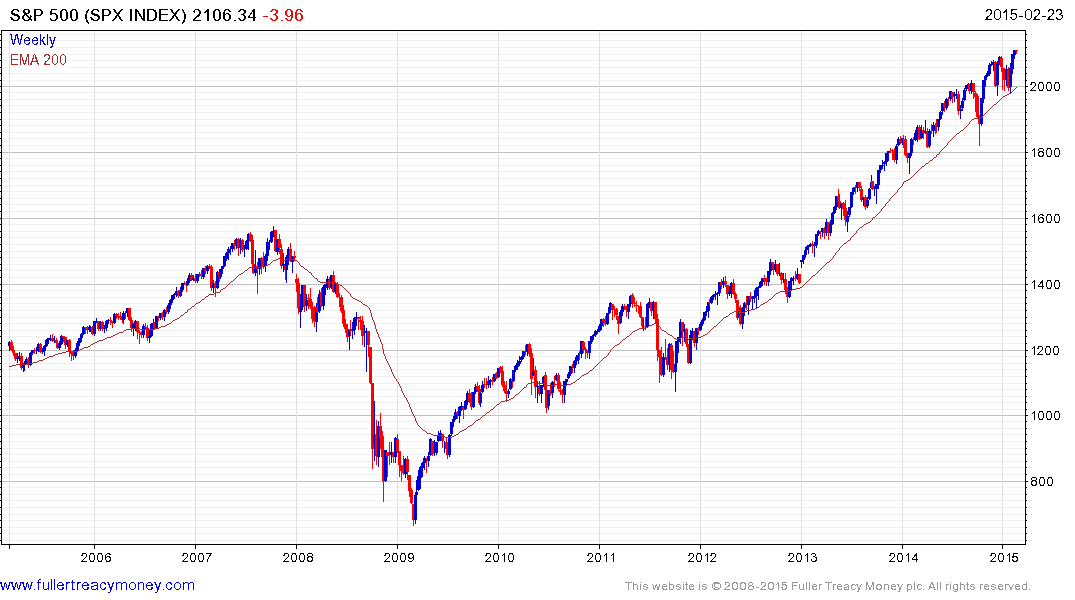

A consistent trend is a trend in motion and Wall Street indices continue to post new highs as they reassert their medium-term uptrends. How valuations are calculated is a movable feast and is open to interpretation based on whether one looks at P/E ratios or earning yield and cash balances. What we can conclude with certainty is that the search for cheap valuations has become a lot harder.

Taking a step back, the wider market bottomed in 2009 and we are almost six years into a bull market on Wall Street. Europe is now playing catch up and has the potential to continue to outperform. The same can be said of Japan and China. Part of the reason for this is because bargain hunters have been forced to expand their search to global markets following the persistence of the rally on Wall Street.

We have long described this rally as liquidity fuelled. Little wonder when central banks have been printing trillions of Dollars. The expansion of the Fed’s balance sheet may have stabilised but the ECB is about to engage on a massive printing program, Japan is still engaged in QE and central banks globally are still cutting rates to avoid deflationary pressures. There is no shortage of liquidity, quite the opposite, and there is little prospect of the situation changing anytime soon. Capital is global and mobile so there is still fuel for equities to move higher. This means that there is a risk of a bubble developing; suggesting monitoring the consistency of trends is more important than ever.

Back to top