Global Strategy Weekly

Thanks to a subscriber for this report by Albert Edwards for SocGen. Here is a section:

The commodity complex is now seeing a collapse in prices, and this shows great similarity to what we saw in mid-2008. Although the oil price decline is slower and lagging, likely because of the Ukraine war, other industrial commodity prices are in virtual freefall. Soft-landing advocates must now face the overwhelming evidence of economic collapse and extricate their heads from the sand. ¢

Despite the fallout from the Ukraine war, agricultural prices too have also imploded, and that will sound a note of caution for those who think the oil price cannot fall as quickly as other industrial commodity prices. With the oil price having slid from $125/b to under $100 in a month, it should not be long before the yoy comparisons are negative, as with food prices.

Headline CPI inflation will likely turn negative, and the inflation narrative will then evaporate (temporarily), so trigging a collapse in US 10y yields back below 1%. What a shock that will be!

Here is a link to the full report.

This characteristically bearish perspective should be contrasted with that of Henry McVey at KKR who believes the outlook is still benign and a soft landing is the most likely scenario. Here is a section:

Strong job reports do not change our view that we are going to see a profits recession, including also a potential technical economic recession. Every cycle is different, and this one will likely be remembered for the reality that one of the supply side shocks is a shortage of labor. As such, this slowdown could look more like the 2001 slowdown. What happened then? Unemployment went up, but less than the 2.5% average for a recession, and growth slowed but did not collapse. For structural bears, we agree that we put too much money in the system and there are some supply-side issues on which to focus, but we just don’t see the major de-leveraging that defined the 2008 crisis or the 1989/1990 downturn.

The main point is that the “soft landing” in the early 2000s coincided with a crash in the technology sector, valuation contraction, an exogenous shock that prompted monetary and fiscal stimulus (9/11), and the recoverty began with lower valuations for everything outside of tech. Today, valuations are high for just about everything.

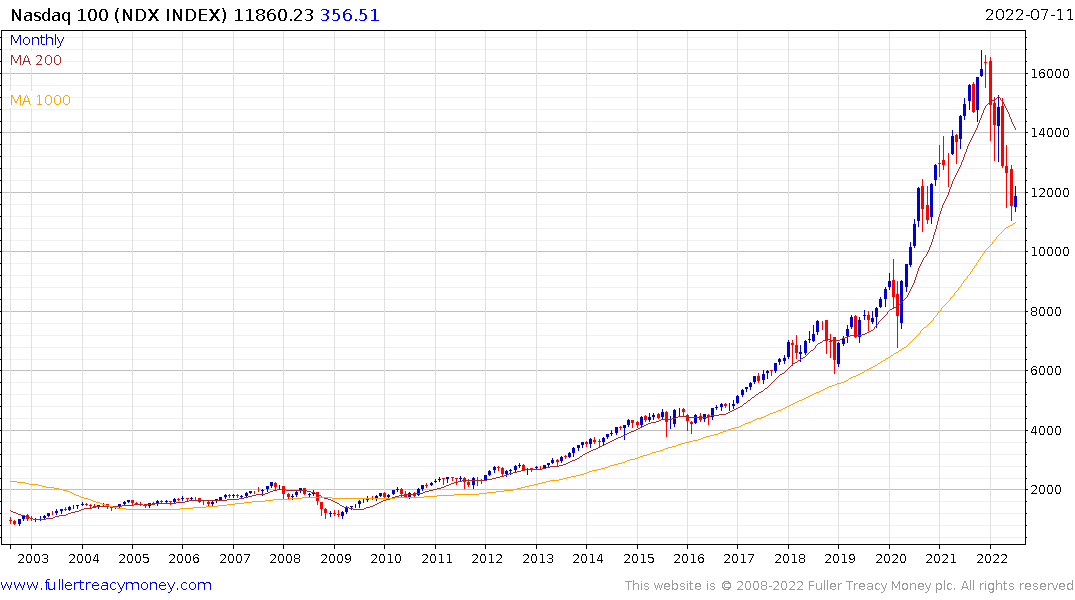

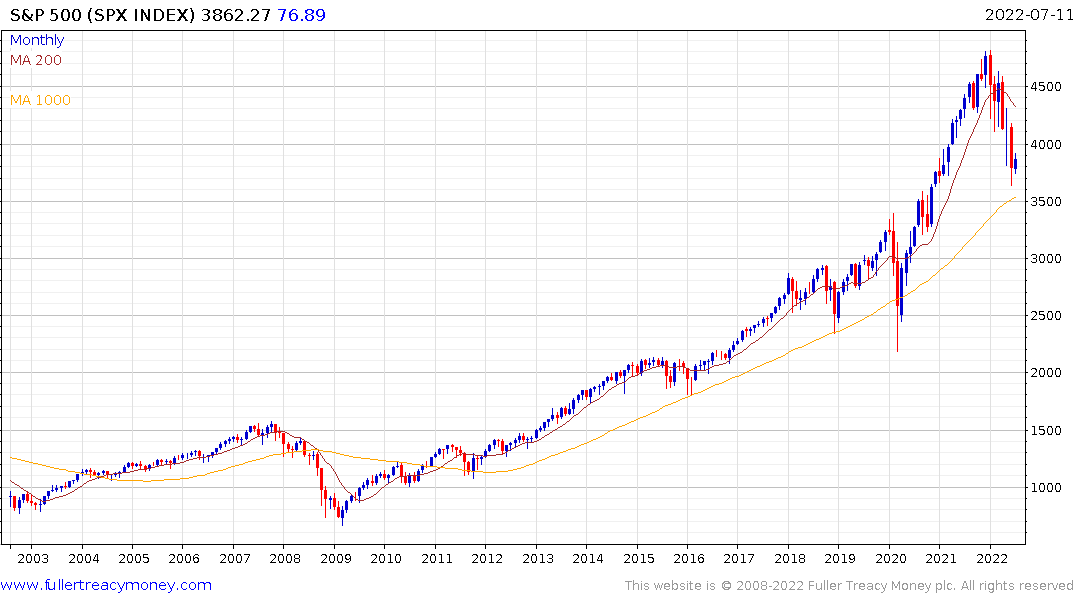

The major Wall Street indices are pausing in the region of their respective 1000-day MAs. This is where a buy the dip investor is most likely to be active so we have seen some steadier action. The challenge to that line of thinking is the hit to earnings has not begun yet. Valuations are set to rise rather than fall over the coming quarter, in the absence of an additional fall in prices.