BOE Sees Inflation Pickup as Labor Market Strengthens

This article by Tom Beardsworth and Scott Hamilton for Bloomberg may be of interest to subscribers. Here is a section:

The Bank of England said U.K. inflation may accelerate quickly in 2016 once the impact of plunging oil prices fades as wage and unemployment data showed labor-cost pressure is starting to build.

In the minutes of its February meeting published Wednesday, the Monetary Policy Committee said its nine members voted unanimously to keep the benchmark interest rate at a record-low 0.5 percent. It also said the slowdown in inflation will be temporary and that, for two of its nine members, the decision was “finely balanced.”Combined with an improving labor market, the outlook for inflation is causing divergences on the MPC about when policy tightening should start. While the bank said last week it could respond to record-low inflation with an interest-rate reduction or more bond purchases, policy makers are pushing the message that such an outcome isn’t the most likely.

For the two members whose decision was “finely balanced,” the outlook means there may be a case to increase borrowing costs later this year. For the committee as a whole, the next most likely move in policy over the next three years is tightening, though one said there was a “roughly equal” chance the next shift would be a loosening.

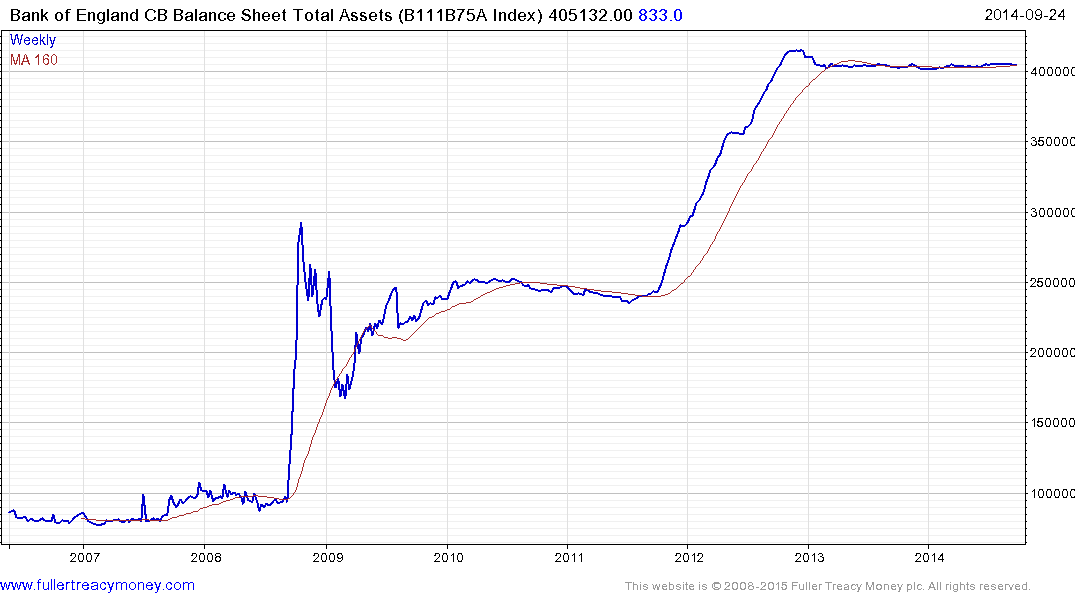

The Bank of England has played a vital role in steering the UK through what has been a challenging decade to date and has so far excelled. By being among the first central banks to allow its currency to collapse during the financial crisis, the BoE insulated the economy from the global economic difficulties that were to come.

Adopting a quantitative easing strategy in an environment where inflation was coming in ahead of expectations achieved what many central banks have failed to do which is to inflate away some of the outstanding debt load. Its balance sheet has remained steady since the end of QE in 2012 and any move to remove liquidity will be gradual.

At the present moment while the majority of countries are expressing deep concern about deflationary pressures the Bank of England is rightfully pointing out that this is a disinflationary phenomenon and will wash out of economic figures over a number of quarters once commodity prices stabilise.

UK Gilts hit a new all-time low yield in January and are rapidly unwinding the overextension relative to the 200-day MA. If yields find support above the 1.7% area on the next price rally, we can begin to conclude base formation development is underway.

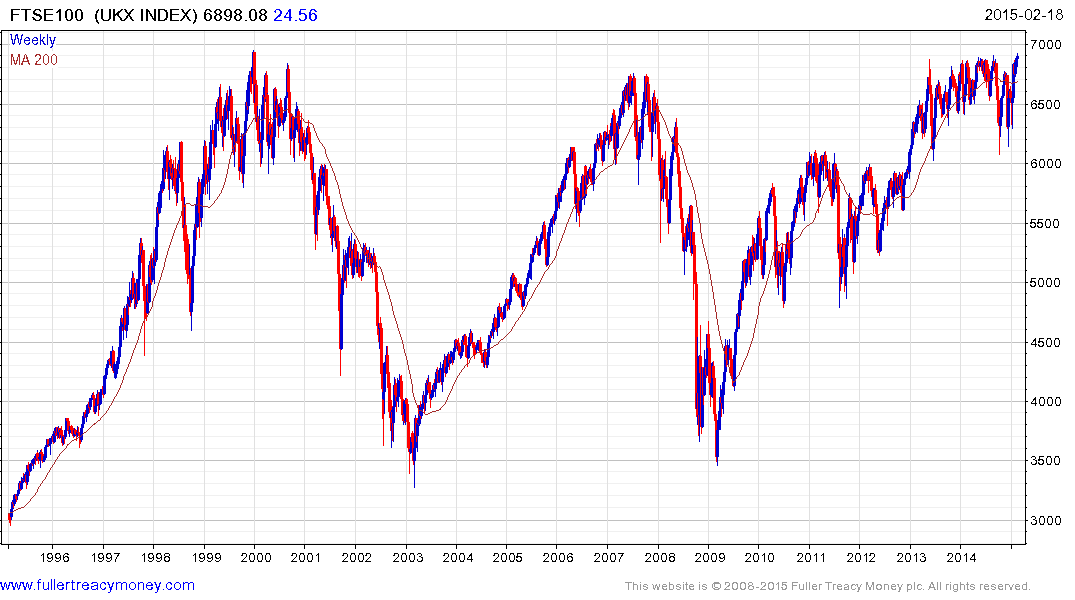

The FTSE-100 is within 32 points of hitting a new all-time high, having rebounded impressively from its October low. A clear downward dynamic would be required to question medium-term scope for additional upside.

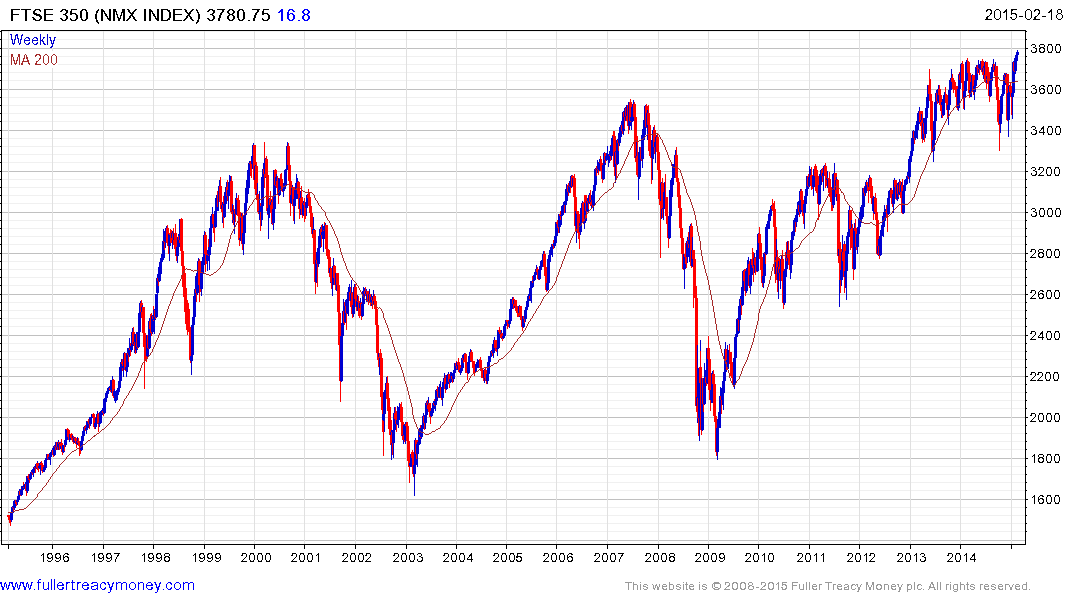

While the FTSE-100 is the most popular UK benchmark, the FTSE-350 is probably more reflective of the UK economy since the large cap Index is loaded with internationally oriented companies. The FTSE-350 has been consolidating above its 2007 peak for the last 18 months and is currently breaking out of this medium-term consolidation.

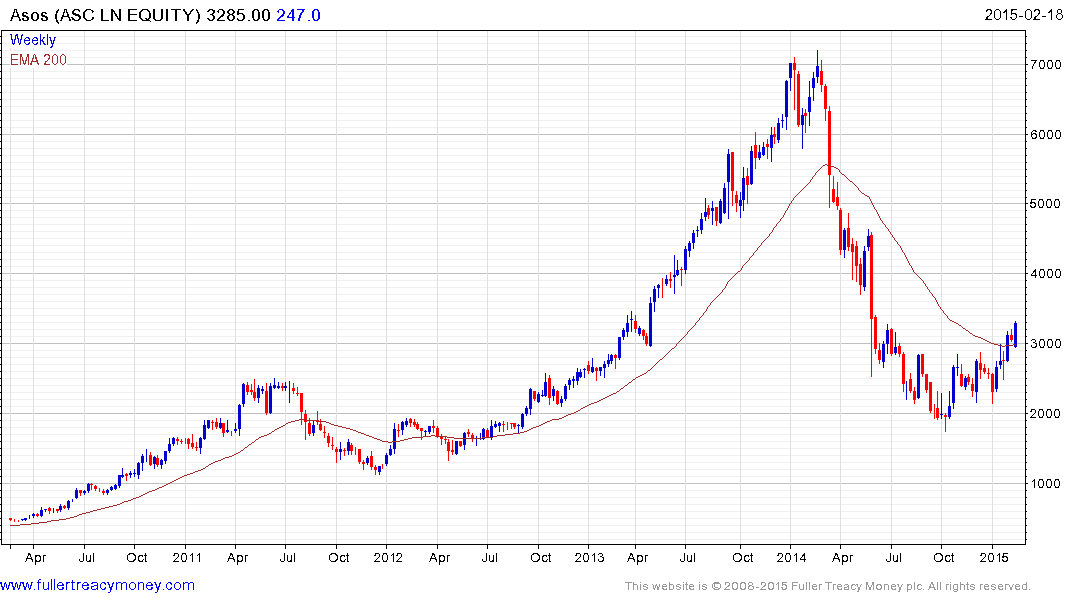

The FTSE AIM 100 Index of the better capitalised small caps has been moribund when compared to the above indices. However it is currently firming in the region of the lower side of a four-year range; holding a progression of higher reaction lows since October. Its largest constituent Asos Plc, the online retailer, unwound its entire bull market advance by October but has bounced and is now trading back above the 200-day MA