S&P Europe 350 Dividend Aristocrats

Following yesterday’s review of the outlook for the Eurozone’s QE program I thought it would be instructive to look at the upside potential for Eurozone companies with reasonably reliable records of increasing dividends. The Eurozone does not have the same regard for dividend sustainability as the USA and therefore the qualifications S&P imposes for membership of the European Dividend Aristocrats is not as stringent as for the USA, being only 7 years of consecutive increases versus 25 years.

Some of the more interesting chart patterns where companies are paying reasonably competitive yields include:

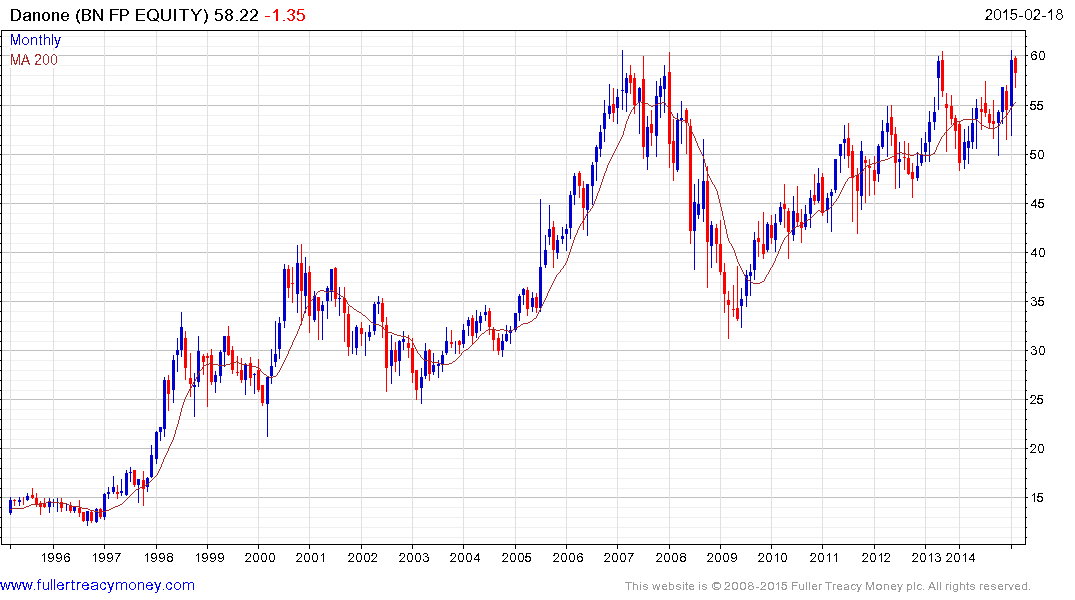

In the processed foods and infant nutrition sector Danone (Est P/E 22.23, DY 2.49%) is currently testing the upper side of it an 8-year range and a sustained move below €54 would be required to question medium-term scope for a successful upward break.

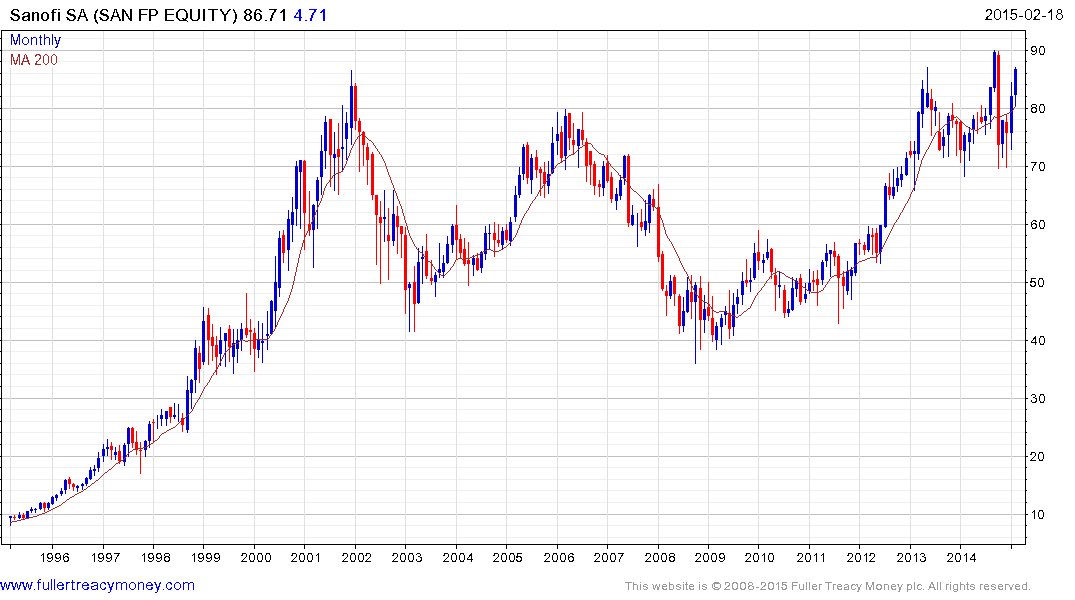

In the pharmaceutical Sanofi (Est P/E 15.83, DY 3,29%) has so far lagged its competitors but is also testing the upper side of a long-term range.

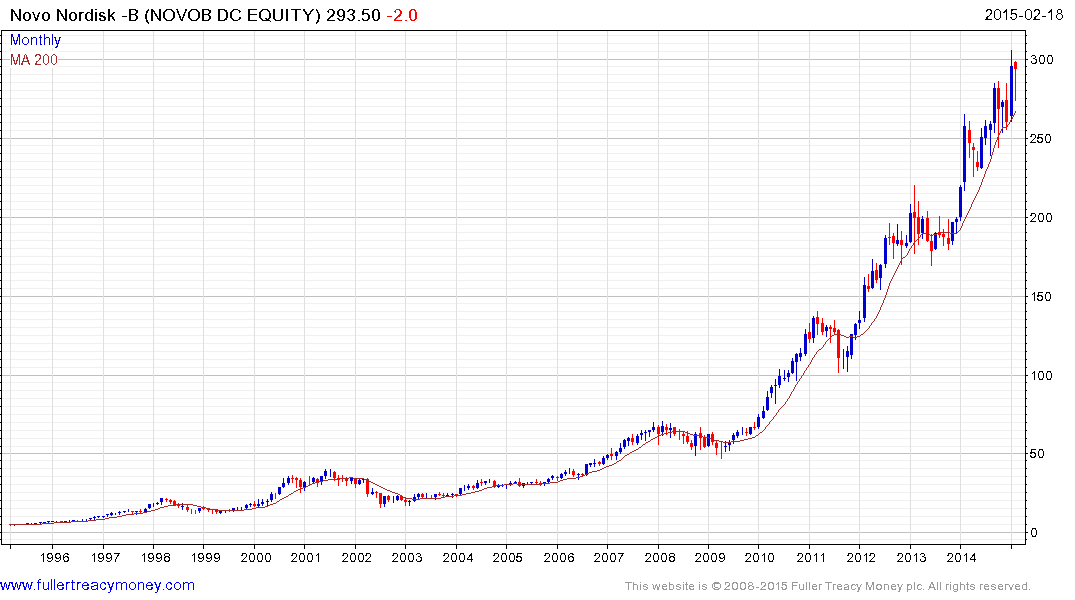

Novo Nordisk (Est P/E 24.8, DY 1.7%) is denominated in Danish Kroner which is pegged to the Euro. The share remains in a reasonably consistent uptrend.

In the utility networks sector Spain’s Enagas (Est P/E 16.11, DY 4.77%) continues to find support in the region of the 200-day MA following pullbacks.

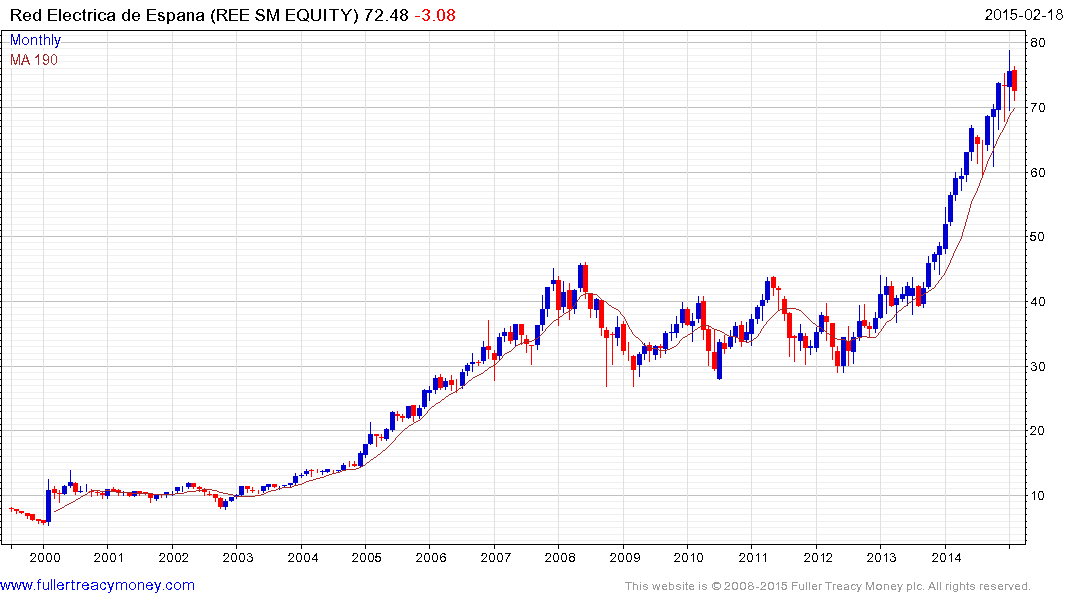

Red Electrica Corporacion (Est P/E 16.85, DY 3.66%) has a similar pattern with the same sector.

In the cosmetics sector L’Oreal (Est P/E 25.63, DY 1.74%) is susceptible to mean reversion following an impressive breakout which should help to improve its valuations.

Generally speaking former members of the Dividend Aristocrats often represent companies that had a bad quarter or have slightly less reliable cash flow so that they drop in and out of membership. This is particularly true of companies with a declining free float since liquidity is a criterion for membership in addition to dividend increases. It is for this reason that I created a list of former members of the Dividend Aristocrats in the Chart Library.

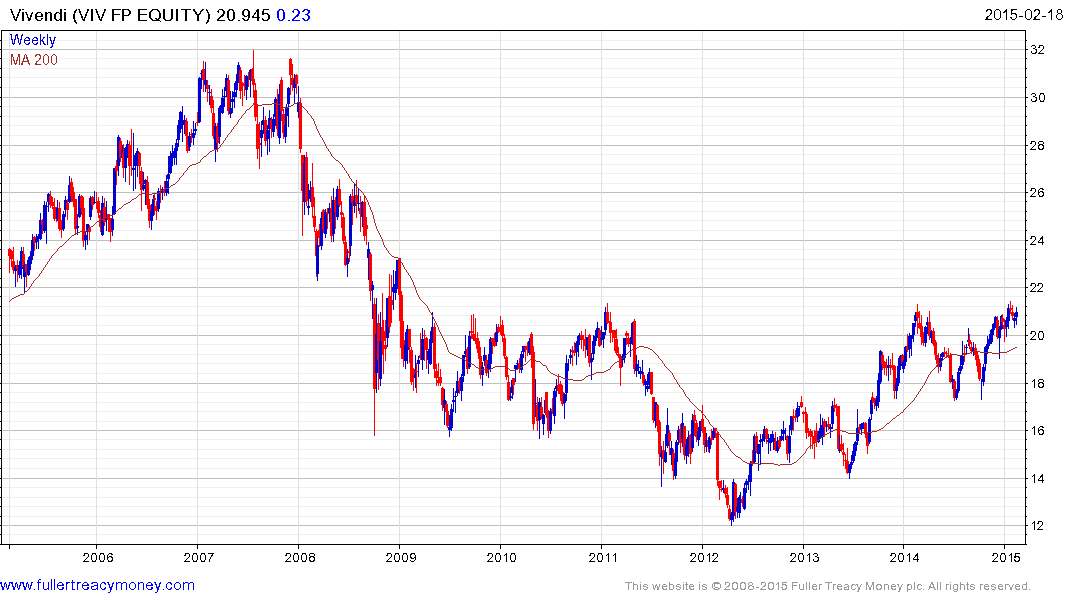

Vivendi (Est P/E 45.43, DY 4.77%) broke out of a six-year base in November and the benefit of the doubt can be given to the upside provided it continues to find support in the region of the 200-day MA following reactions.

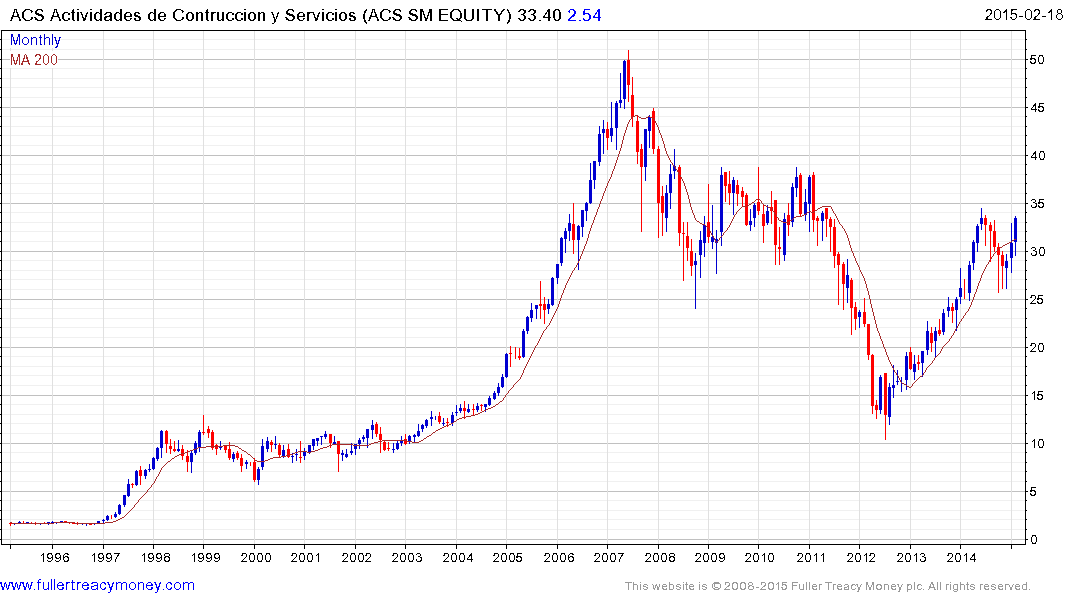

In the construction sector Italy’s Atlantia (Est P/E 24.54, DY 3.28%), France’s Vinci (Est P/E 14.77, DY 3.37%) and Spain’s ACS Actividades de Contruccion y Servicios (Est P/E 14.15, DY 3.46%) share similar chart patterns. They may benefit from Eurozone stimulus not least because the region needs to focus on getting people back to work and infrastructure development tends to be favoured by politicians.

Back to top