Oil Market Outlook

Thanks to a subscriber for this detailed report from DNB Markets which may be of interest. Here is a section:

Two years ago we warned that the shale oil revolution might be a threat to the most expensive oil projects around the world. We argued that the most expensive barrels risk being pushed out of the market by shale oil, just like the Russian Shtokman project was pushed out of the market by shale gas. Shale oil is not particularly cheap, it seems to require Brent prices in the 60-105 $/b range in order to be developed, but the cost curve is very different from the other resources out there.

According to the Goldman Sachs report “400 projects to change the world”, which was released on May 16, the cost curve for the shale projects range from 60-105 $/b, however 90% of the curve is flat at 80-85 $/b. According to the Goldman report, it would require an oil price of 40-100 $/b to develop 4 Million b/d of peak production from Deepwater projects, 20-110$/b for Traditional projects to reach 4 Million b/d, 40-110$/b for Heavy oil projects to reach 5 million b/d at peak and 35-110$/b to develop Ultra deepwater at peak production of 8 million b/d. It would however not require a higher oil price than 85 $/b to see peak production of US shale oil reach 10.5 million b/d. This changes the whole industry as there is no longer a requirement for oil prices to increase anymore in order to cover the market need for the rest of the decade. We hence maintain our view of the oil market that we launched two years ago when we claimed that the shale oil is a game changer for the global oil industry.

There are several quotes from Goldmans’ top 400 report we would fully agree with. Here are some of them: “As shale supply continues to grow from the US with no potential upside to oil demand, significant downside risks continue to plague oil prices”. “Shale dominates volumes and pushes high cost developments into irrelevance”. “Assuming the pace of activity in developing US shale oil reserves remains high – a scenario that is likely with oil prices above 85 $/b – the global oil market will continue to be well supplied in our view. We believe this could have material consequences for oil discoveries that sit at the top of the cost curve, which may not get developed”. “The consequence of shale developments is a displacement of projects with break-evens above 85 $/b Brent”.

It seems the oil majors are now responding to this new situation after pressure from their shareholders. The focus is shifting from volume to project economics and return focused capital discipline. Why would you in the new resource world invest billions of dollars to develop a project that requires 100 $/b or higher to break even? Studies have shown that more than 400 billion USD of global CAPEX is at risk if oil majors choose not to invest in projects that require a higher oil price than 85 $/b in order to be developed. According to Barclays Capital’s E&P spending report published in June, the oil majors will be cutting their spending by 1% in 2014. Total global E&P spending will still grow 6% to 712 billion USD according to the report, but the increase is coming from US independents and from National Oil Companies and not from the oil majors. US CAPEX E&P spending is set to increase by 9.6% as focus continues to shift towards US onshore. US CAPEX spending has now increased from about 100 billion USD in year 2010 to an estimated 164 billion USD in 2014.

Here is a link to the full report.

We have long defined the bull market in oil prices from the perspective of the rising cost of marginal production. There is plenty of oil to be brought to market if the price is right. Over the last decade, as demand has increased, the marginal cost of additional barrels has risen to meet it. Shale oil represents a truly important development since it was not previously thought possible to extract oil from these formations directly and they are very large. With increasingly large volumes coming through, shale oil represents a significant marginal supplier for the global market.

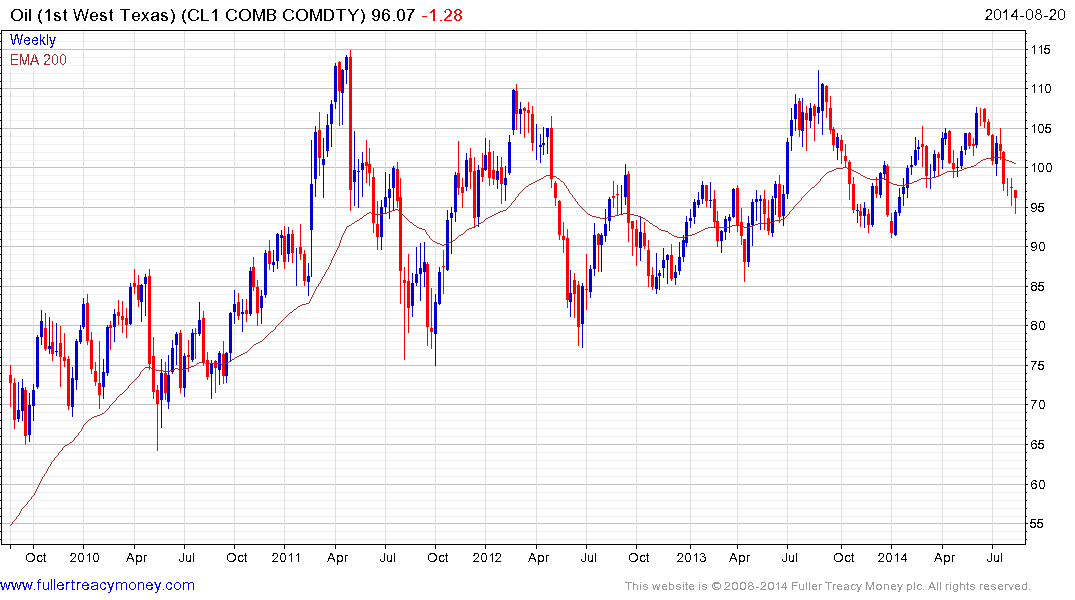

WTI Crude Oil found support in the $80 region twice between 2011 and 2012 and has held a progression of incrementally higher reaction lows since. It has pulled back sharply over the last couple of months to test that progression. A clear upward dynamic, with follow through, to break the two-month progression of lower rally highs will be required to confirm support in the current area.

Brent Crude has the additional pressure of Saudi Arabia’s unwillingness to see prices trade below $100 on a sustained basis. Brent has been ranging with a mild downward bias since 2011 and is once more testing the psychological $100 level. Some steadying in this area is to be expected but a break in the short-term progression of lower rally highs will be required to signal a return to demand dominance in this area.

If we conclude that the marginal cost of production is $85, then the Canadian oil sands where the cost of production is in the region of $50-60 continues to represent a powerful growth story subject to transportation. Alberta is a landlocked province with the Rockies between it and the sea. It has relied on the USA as an outlet for its exports and due to issues with the Keystone pipeline has had to rely on rail and smaller pipelines to transport cargoes. LNG export facilities are already being built in British Columbia and it would seem to be only a matter of time before Canada goes ahead with an alternative Western pipeline route for crude oil.

Canadian Oil Sands completed a more than two-year base in March and continues to form a first step above it. It has returned to test the region of the 200-day MA and it will need to hold the $22.50 area if medium-term potential for additional upside is to continue to be given the benefit of the doubt.