Email of the day on oil prices

Today I listened to a presentation by Torbjørn Kjus, oil analyst at DNB Markets. He has become quite a guru in the last years so it was interesting to hear what he had to say. Interestingly, after having been possibly the most bearish oil price analyst for quite some time, he is now among the most bullish forecasters, see pages 7-9 in the presentation. He believed that the oil producers would continue to cut investments and particularly exploration costs, even if we see a move to $70-80 bbl. The majors will prefer to maintain dividend payouts. This will be particularly painful for oil services. As such one should expect oil producers to gain more from any oil price rise, rather than oil service companies.

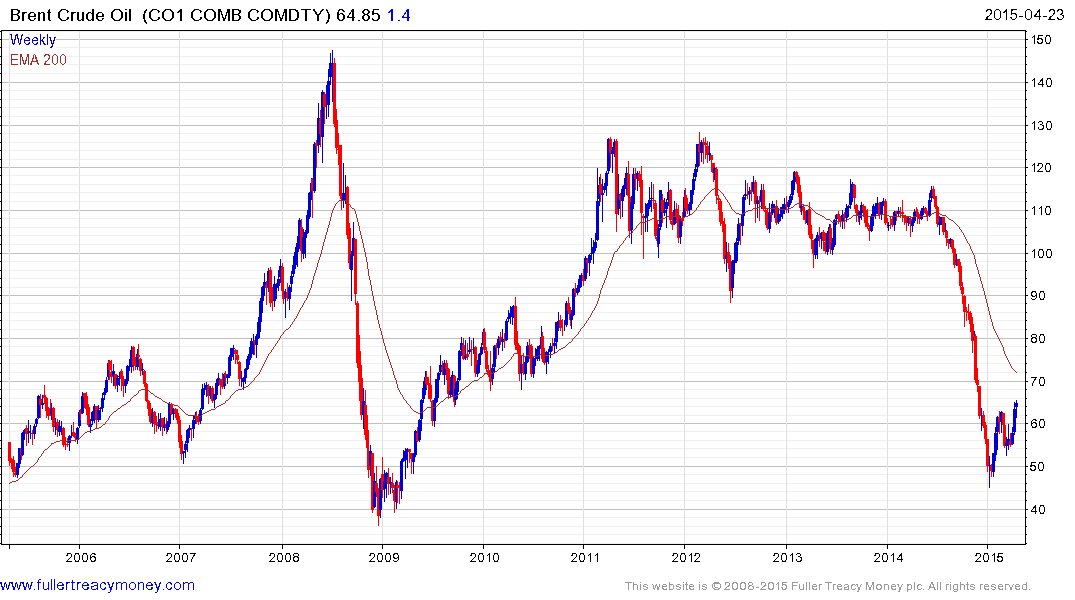

Thank you for this topical report and informative email. With oil prices stabilising above the psychological $40 level and as the Dollar unwinds its short-term overbought condition it makes sense to be more positive on the oil prices for at least as long as it takes to unwind the oversold condition relative to the 200-day MA, which at present is near $72.

Here is a summary of the arguments set out in the above report:

Bullish Arguments

Large cuts in global oil investments

Even larger cuts in US shale oil companies –US shale oil growth finance by debt, so CAPEX cuts now needs to be huge

Rig count in the US is collapsing

US liquids production growth of 1.5 mbd will cease to about zero within 12-18 months

Decline rates set to accelerate already into 2016

Demand is performing very strongly in US and China on lower prices

Record car sales in China in December

Americans driving more and buying more gasoline thirsty vehicles again

65 $/b vs 110 $/b is worth 1500 billion USD to the global oil importers –Translates to better global GDP-growth

Geopolitical risk in OPEC countries is increasing at low oil prices (and remember we are coming from average 110 $/b)

Key risk is Venezuela and Iraq

Spare capacity is only 3% compared to 17% in the middle of the 1980’s

Oil price will move higher before supply/demand-balance is moving to stock draw modus

Bearish Arguments

Over supplied supply/demand-balance in 1H2015

Global oil stocks are already high and continue to build rapidly –Particularly in the US

Shale oil resource base looking to be much larger than everybody though just a few years ago

Shale oil production has only surprised to the upside so far

Delayed response from drop in rig count to drop in production –High grading of acreage Productivity improvements

Global demand growth last ten years protected by subsidies –What now when subsidies are removed in many EM?

Saudi Arabia not set to protect a high price –targeting market share instead

Costs in the global oil industry set to drop significantly –Slack in the service industry as CAPEX is cut

The marginal 2-3 million most expensive barrels are set to be cheaper = lower oil price required

Libya is already out of the market and cannot get any worse –Can only see barrels returning from here

Iran already shut out with 700-800 kbd, more chance of barrels coming in than more out

There is a great deal of overhead resistance, represented by the almost four-year type-3 top that ranged between $90 and $130 for Brent. Based on the slides on page 8 and 9 of the report very few analysts are anticipating a return to those high prices and tend to agree. If we take the above arguments into account the prognosis is for potentially volatile ranging over the next number of years.

Among related stock market sectors those most sensitive to oil prices experienced the deepest declines.

For example Tullow Oil which has major exposure to development costs experienced a deep decline but has found at least short-term support.

Offshore drillers such as Subsea 7 have broadly similar patterns to the oil price of late.

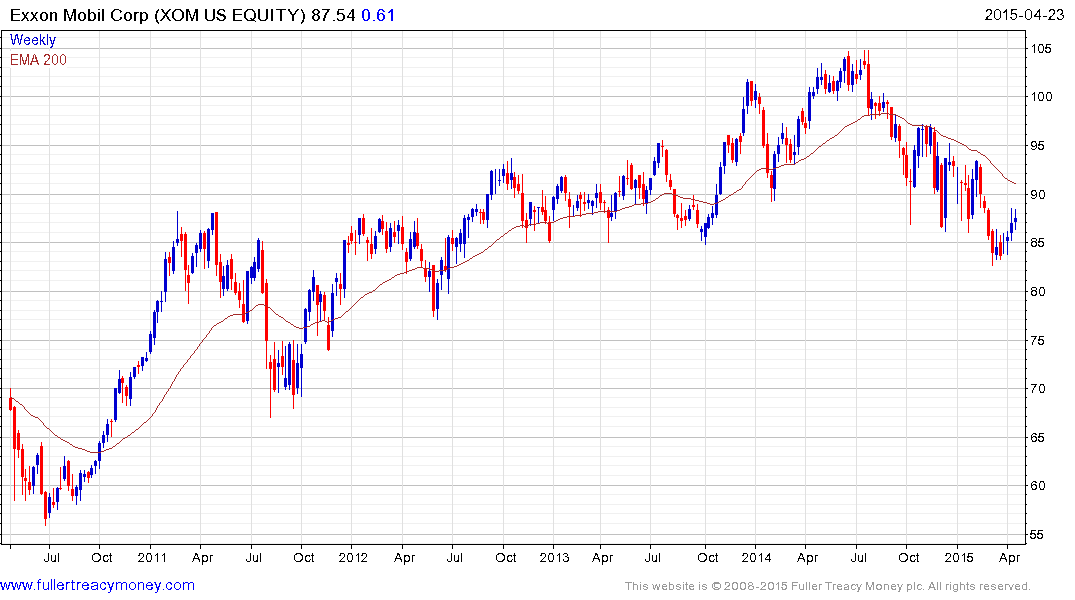

Major oil companies such as Exxon Mobil were relatively insulated from the decline in oil prices and subsequently are likely to be less sensitive to any rebound.

One consideration that is not included in the above report is the rapid improvement in solar technology which is likely to have far reaching consequences for the entire energy sector. It is not sufficient to think simply of this conundrum in terms of one energy source supplanting another. Solar is a technology and therefore there is no limit on its expansion or the scale of competition with any extractive energy source. This story today from Extreme Tech highlights how quickly the sector is evolving.

Back to top