Reckitt Benckiser Sees Pricing Squeeze After Worst Year Ever

This article by Thomas Buckley for Bloomberg may be of interest to subscribers. Here is a section:

In an effort to sharpen Reckitt Benckiser’s focus on brands such as Strepsils and Mucinex cold remedies, Kapoor has moved to separate the company’s home-care and health businesses. Reckitt also became a leader in infant nutrition with the acquisition of Mead Johnson Nutrition Co. last year.

On Monday, it increased its forecast for synergies from the deal to about $300 million from $250 million. This year’s savings will only “slightly exceed” additional infrastructure expenses associated with the new health and home-and-hygiene business units, the company said.

Morgan Stanley analysts led by Richard Taylor described the company’s outlook as conservative.

A question someone asked of Charlie Munger at last week’s Daily Journal AGM stuck with me over the weekend. It was how he thought the established brands would fare with increased competition from the likes of Costco and Amazon who are pioneering their own products often in direct competition. His answer was that white- labelling and own-brand selling would have an effect, but if one were to take a long-term view the established brands would still have value.

Kapoor’s statement in the interview on Bloomberg that Reckitt Benckiser is doing 50% of its Chinese sales via online vendors is a testament to the fact that consumer companies can rise to the challenge of the online sector but the transition is likely to be lengthy and not without hiccups.

The consumer staples sector benefitted inordinately from the rise of the global consumer and the reliability of their cashflows over the last decade. Since they are considered bond proxies, their yields compressed and valuations increased. The tailwind of continued growth in the emerging markets is unlikely to abate any time soon but rising interest rates are having a knock-on effect for how investors regard valuations.

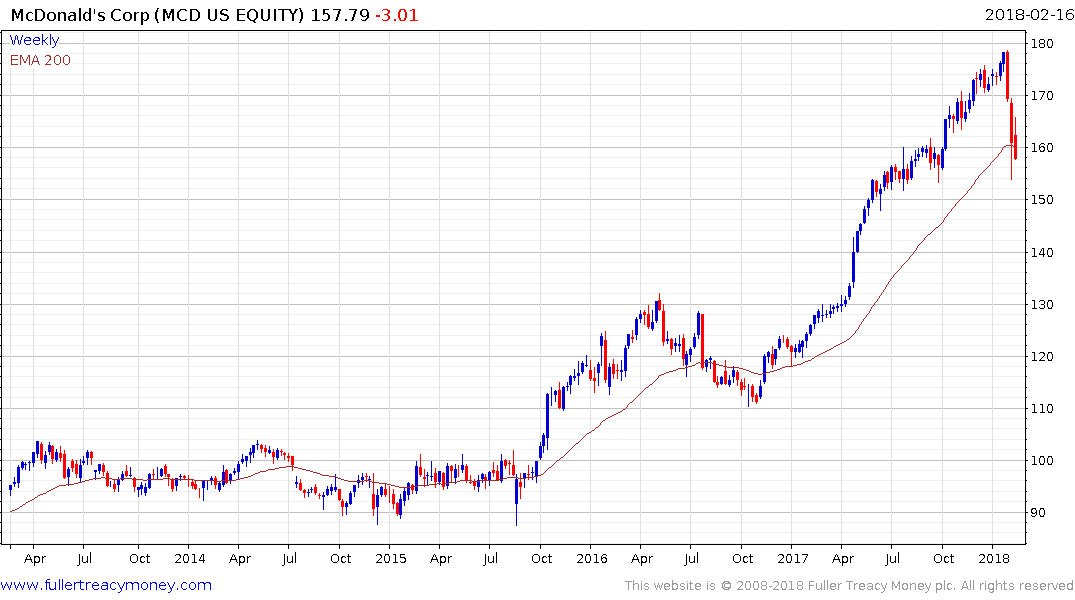

3.5% seems to be a level many income-oriented investors think of as value when they look at the value proposition presented by consumer companies. Within the consumer discretionary sector McDonald’s share price tends to bounce when the yield hits 3.5%. The same is true of Coca Cola.

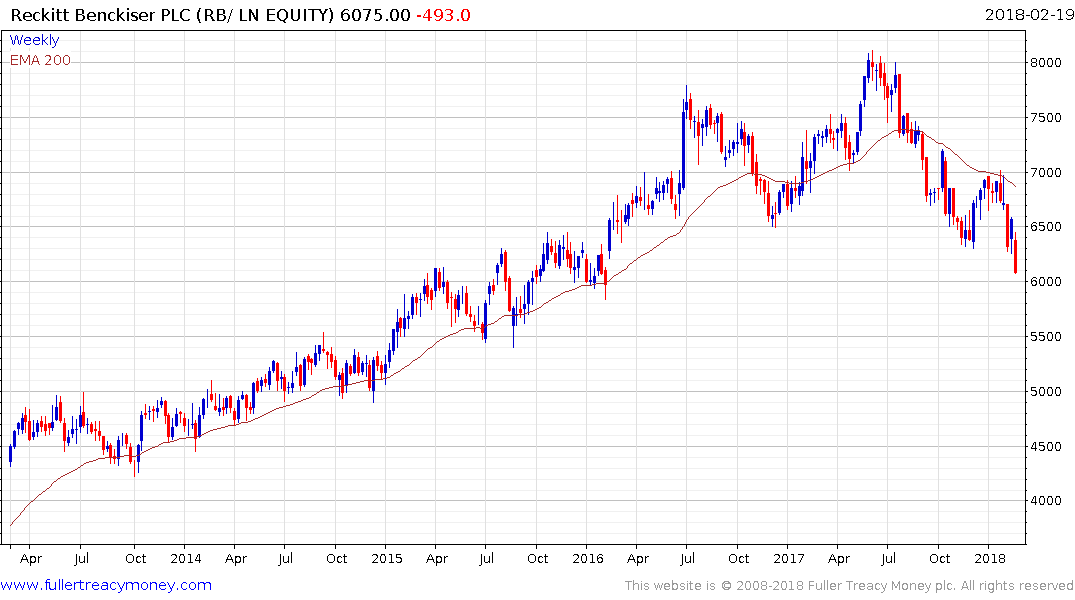

Meanwhile, Reckitt Benckiser’s yield last peaked at 3.86% in 2011 and the yield is on an upward trajectory once more as the share corrects.

For Unilever 4% seems to represent an area of support.

L’Oreal tends to bounce from the 2.5% level.

More often than not Henkel tends to bounce from the 2% level.

These levels represent potential yield areas where value investors might be tempted to initiate positions. In the meantime, there is evidence that the above trends for European household goods companies have lost consistency.