End Game

Thanks to a subscriber for this report from Myrmikan Research which favours gold. Here is a section:

Here is a link to the full report.

Here is a section:

In 1969, at the beginning of the previous inflation-induced default on American obligations, 23% of the Federal Reserve’s Treasury bond holdings had a time to maturity of less than 90 days and 1.2% had a maturity date greater than 10 years. The Treasury bond portfolio itself comprised 68% of the Federal Reserve’s assets, the balance being “cash items in process of collection,” foreign currency, and gold. That was a resilient balance sheet.

Currently, 6% of the Federal Reserve’s Treasury bond holdings have a time to maturity of less than 90 days and 26% have a maturity date greater than 10 years. The Treasury bond portfolio itself comprises 55% of the Federal Reserve’s assets, and another 40% is comprised of mortgage-backed securities. That is not a resilient balance sheet—it is highly sensitive to interest rates.

Myrmikan has argued for eight years that it is rising rates that will destroy the value of the Federal Reserve assets and, therefore, the value of its liabilities, a unit of which is known as a “dollar.” Gold, having the most stable value of any substance in nature, must rise as the dollar falls. Therefore, gold naturally correlates with interest rates, as the following chart of the inflationary 1970s illustrates.

The USA has a lot of debt and a great many unfunded liabilities. The only way countries have gotten themselves out of problems like this previously is to either default or inflate the debt away. Procyclical polices and debt fueled infrastructure spending suggest the USA is going for the latter option. Doubling down on the military is a none too subtle move designed to emphasise the world’s pre-eminent military power might be withdrawing from overseas commitments but it is not going away.

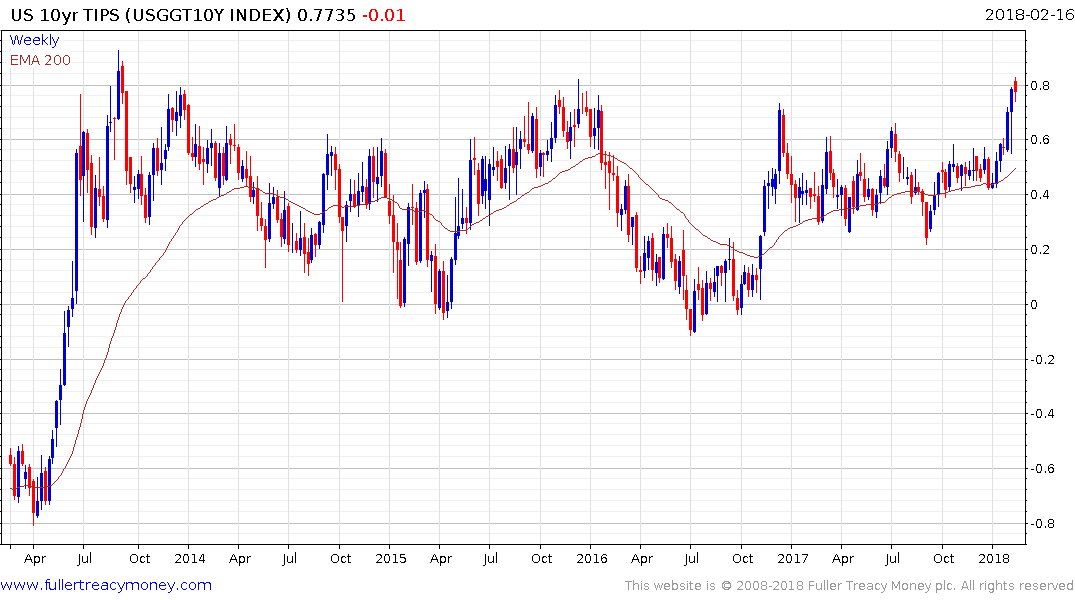

10-yr TIPS yields have been ranging below 80 basis points since 2013; since unwinding the negative yields environment that prevailed from 2011.

Generally speaking, when 10-year yields are spread over TIPS the difference rarely gets above 250 basis points, suggesting a breakout in either chart is likely to be accompanied by a similar move in the other.

.png)

It’s all well and good to talk about the Dollar taking the brunt of inflationary pressures but we can’t forget that the currency does not exist in a vacuum. If fiscal stimulus finally succeeded in getting stubbornly low inflation back into expansionary mode, other countries will follow suit.

As a monetary metal, gold does best when it is appreciating against all currencies. That condition has not yet been satisfied. However, it does have some of the clearest base formation characteristics when denominated in US Dollars.