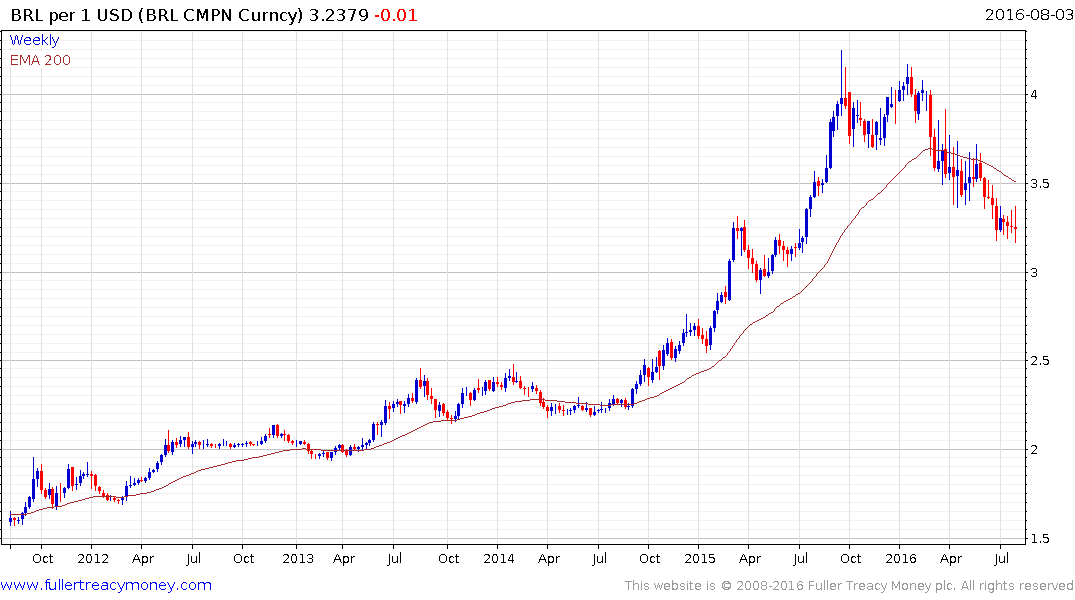

Brazil Real Rises to One-Year High as High Yields Lure Investors

This article by Paula Sambo for Bloomberg may be of interest to subscribers. Here is a section:

Emerging-market currencies rallied after the Bank of England cut its key rate for the first time in more than seven years, boosting speculation that policy makers around the world will continue to ease monetary conditions and the U.S. Federal Reserve will delay rate increases. After keeping its Selic rate at 14.25 percent at a meeting last month, Brazil’s central bank said there is no room for monetary flexibility, citing the need for further fiscal adjustment and an unfavorable climate that is harming global food production.

"The real is gaining momentum as most central banks across the globe continue to ease further their monetary policy," said Arnaud Masset, an analyst at Swissquote Bank SA in Gland, Switzerland. "Investors are desperately chasing higher returns, while volatility in the FX market is at multi-month low, which creates an enabling environment for carry trade and definitely drove the real higher over the last few months."

Buying the real with borrowed dollars in a carry trade has returned 32 percent this year, the most among 42 currencies tracked by Bloomberg.

Bank of England officials voted to reduce the benchmark rate to a record-low 0.25 percent and also to expand quantitative easing, as they slashed economic growth forecasts by the most ever.

"The BOE actions help foster expectations that other central banks might follow and improve liquidity worldwide," said Mauricio Oreng, a senior strategist at Rabobank in Sao Paulo. "And when the general market mood improves, the search for returns causes the high yielding real to outperform."

Brazil has an overnight deposit rate of 14.15% which is attractive to investors, particularly those residing in negative interest rate jurisdictions, despite the obvious issues the economy is subject to that require such a high rate.

Governance is Everything has been a mantra at this service for decades. Brazil represents another great example of how a failure to improve standards of governance during the good times means the drawdown during the bad times is often worse than anyone might have expected.

The Dollar hit a medium-term peak against the Real in September and continues to extend its downtrend. A change of leadership and the prospect that since so many politicians have been implicated in corruption that they may now face closer scrutiny means the new administration has the opportunity to implement the kind of reforms the country so badly needs.

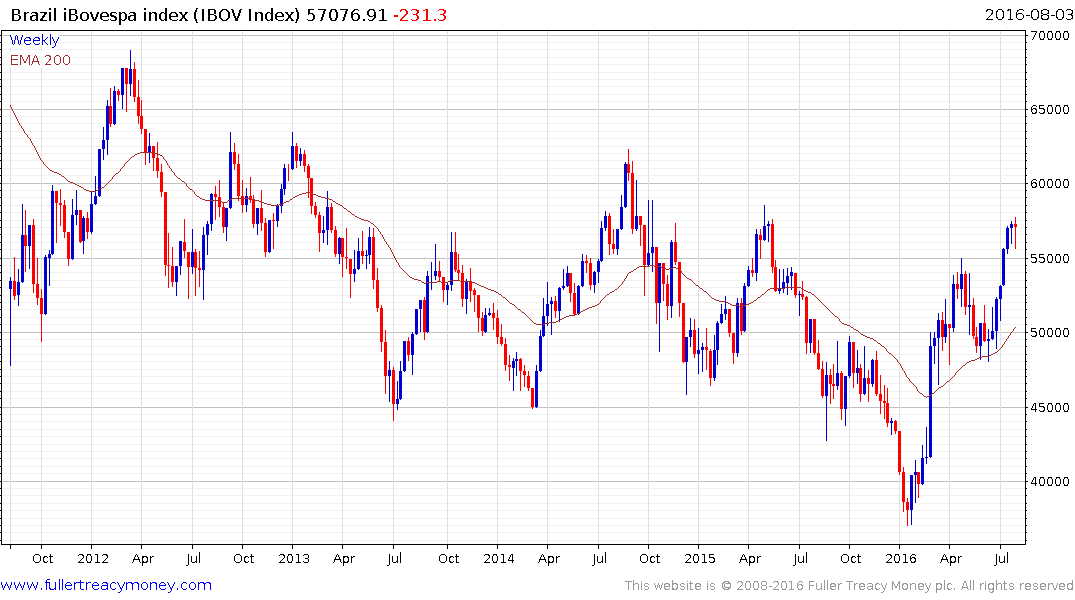

The fact iron-ore prices have broken a five-year downtrend and the Continuous Commodity Index is on a recovery trajectory suggests Brazil’s new government may have more room to stimulate the economy than they expected. The influx of foreign currency from the Olympics is also likely to represent a short-term bonus.

The iBovespa Index found support in the region of the trend mean from June and is now testing the six-year progression of lower rally highs. A sustained move below the psychological 50,000 would be required to question medium-term scope for continued higher to lateral ranging.

The iShares MSCI Brazil ETF has doubled since January and remains on a recovery trajectory.