Why Hollywood As We Know It Is Already Over

This article from Vanity Fair may be of interest to subscribers. Here is a section:

When Netflix started creating its own content, in 2013, it shook the industry. The scariest part for entertainment executives wasn’t simply that Netflix was shooting and bankrolling TV and film projects, essentially rendering irrelevant the line between the two. (Indeed, what’s a movie without a theater? Or a show that comes available in a set of a dozen episodes?) The real threat was that Netflix was doing it all with the power of computing. Soon after House of Cards’ remarkable debut, the late David Carr presciently noted in the Times, “The spooky part . . . ? Executives at the company knew it would be a hit before anyone shouted ‘action.’ Big bets are now being informed by Big Data.”

Carr’s point underscores a larger, more significant trend. Netflix is competing not so much with the established Hollywood infrastructure as with its real nemeses: Facebook, Apple, Google (the parent company of YouTube), and others. There was a time not long ago when technology companies appeared to stay in their lanes, so to speak: Apple made computers; Google engineered search; Microsoft focused on office software. It was all genial enough that the C.E.O. of one tech giant could sit on the board of another, as Google’s Eric Schmidt did at Apple.

These days, however, all the major tech companies are competing viciously for the same thing: your attention. Four years after the debut of House of Cards, Netflix, which earned an astounding 54 Emmy nominations in 2016, is spending $6 billion a year on original content. Amazon isn’t far behind. Apple, Facebook, Twitter, and Snapchat are all experimenting with original content of their own. Microsoft owns one of the most profitable products in your living room, the Xbox, a gaming platform that is also a hub for TV, film, and social media. As The Hollywood Reporter noted this year, traditional TV executives are petrified that Netflix and its ilk will continue to pour money into original shows and films and continue to lap up the small puddle of creative talent in the industry. In July, at a meeting of the Television Critics Association in Beverly Hills, FX Networks’ president, John Landgraf, said, “I think it would be bad for storytellers in general if one company was able to seize a 40, 50, 60 percent share in storytelling.”

The march of technology enabled content creation is undeniable and irreversible. The simple reason from a business perspective is that relying on human beings to be individually creative is fraught with uncertainty, ambiguity and time management issues. Computers on the other hand excel at getting the job done on time and within budget. The challenge has always been to try and teach computers how to be creative.

A joke while I was in college was “to copy from one is plagiarism but to copy from two is research”. That would appear to be how computers will be taught how to develop content. They will first analyse what worked in past successful scripts, then write a new script incorporating details from the research. They are unlikely to come up with anything new but what they will eventually do is create serviceable content. It won’t be art in the classic sense, at least initially, but it will be capable of generating income which in many respects is the greater challenge. With Silicon Valley investing so heavily in content, ensuring they keep users within their respective ecosystem while also generating income from them would appear to be the primary business model.

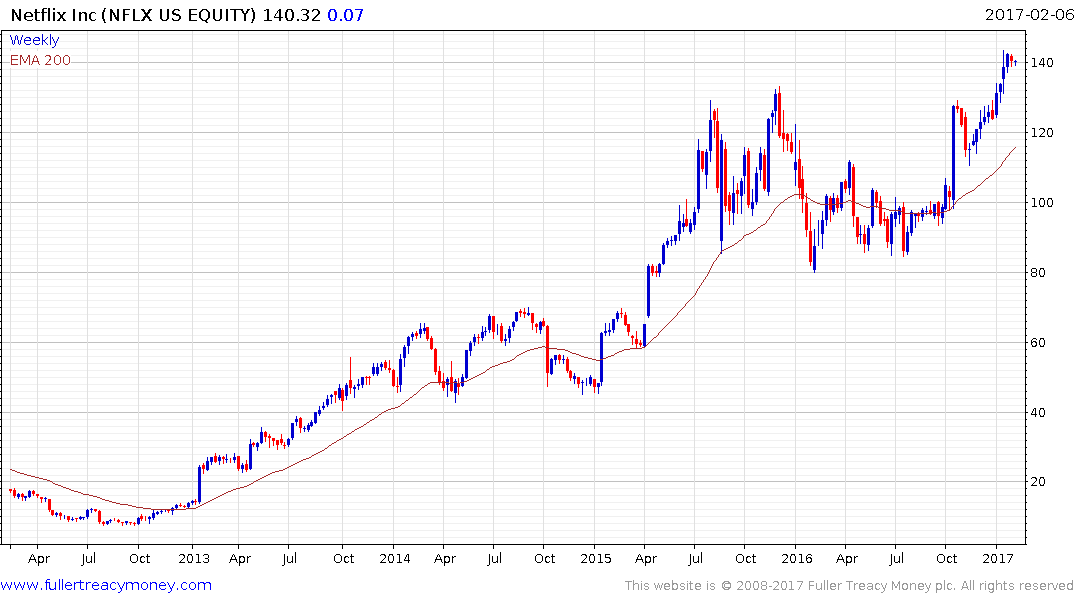

Netflix was among the best performing shares for most of 2015 before pulling back sharply and spending a year ranging. It surged higher in October on renewed earnings optimism and broke out to fresh all-time highs in January. A sustained move back below the trend mean would now be required to question medium-term scope for additional upside.

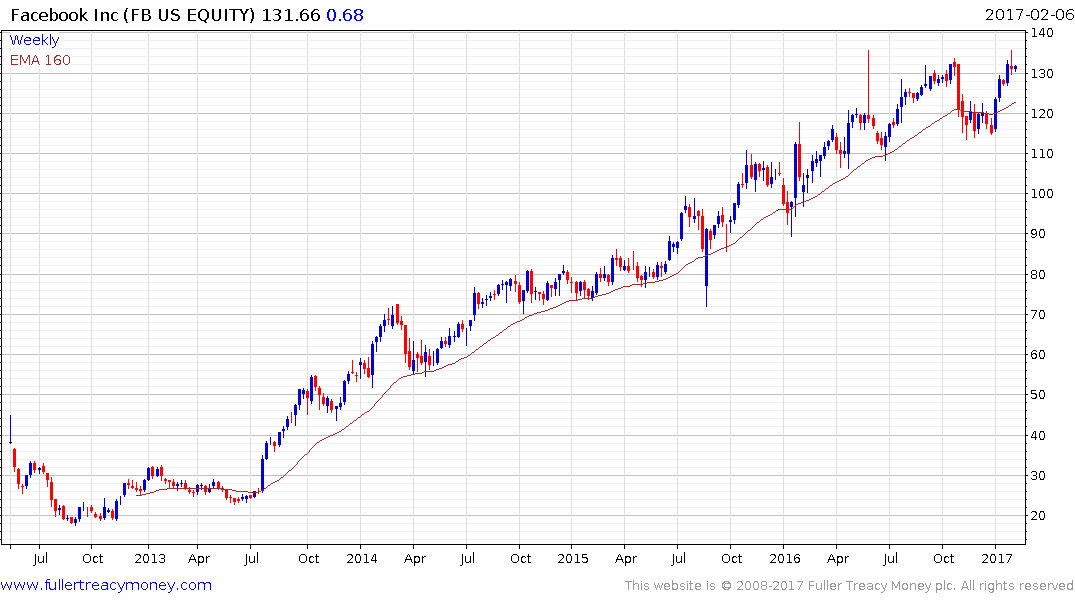

Facebook remains in a reasonably consistent medium-term uptrend defined by a progression of higher reaction lows where it has found support in the region of the trend mean on successive occasions.

.png)

Alphabet posted a well-defined downside key day reversal on January 27th and followed through on the downside the day after. The decline has been relatively modest and a sustained move below the trend mean would be required to question the consistency of the broad uptrend.

Apple surged last week on improving iPhone sales. While it is still looking for a new breakout product the share has spent almost two years consolidating and a sustained move below the trend mean would be required to question medium-term scope for continued upside.

Disney has also firmed following a lengthy consolidation and while somewhat overbought in the very short-term a sustained move below trend mean would be required to question medium-term scope for continued higher to lateral ranging.