What the China bears are missing

Thanks to a subscriber for this article from China Spectator which may be of interest. Here is a section:

First, let's address the issue of overstating the GDP. Critics point to the country's weak industrial production, export and investment figures as proof that the country is fudging its number. Lardy, a senior fellow at the Peterson Institute of International Economics, points to a salient fact that many people choose to ignore: the biggest contributor to the country's GDP is now the services industry.

"the skeptics have taken insufficient notice of China's progress in transitioning to its new model of economic growth, one less dependent on expanding industrial output, investment, and exports and more dependent on expanding private consumption expenditure?¡À, he says.

Between 2011 and 2014, the size of the service sector as a share of GDP rose by about 4 percentage points to 48 per cent and, at the same time, the share of the industrial sector dropped to 43 per cent of GDP. This is a marked change from a decade ago, when the industrial sector accounted for 47 per cent of the GDP while the service sector only accounted for 41 per cent of the economy.

Considering the size of China's economy -- it's a $US10 trillion behemoth -- the transition is even more impressive. Many services are booming in China, the e-commerce sector grew by 31.4 per cent in 2014. The entertainment sector has been growing at an average of 17 per cent a year between 2010 and 2015. In health care, McKinsey predicts the growth in spending will grow from $US357 billion in 2011 to about $US1 trillion in 2020.

Unfortunately the services sector now accounts for more than 50% of GDP because the industrial and construction sectors have declined so much. The services, consumer discretionary, information technology and healthcare sectors are most likely to lead the Chinese economy in a recovery not least because they are receiving a great deal of government support.

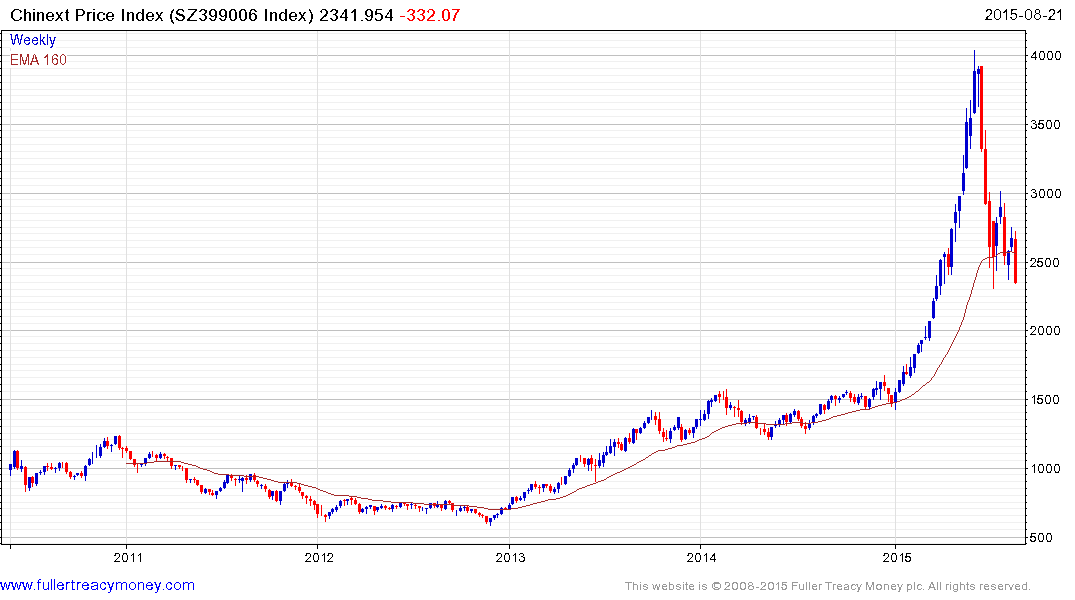

However this was priced in by the impressive outperformance of the Chinext Index and Shenzhen B shares earlier this year.

The wider Chinese market now remains in convalescence mode and the introduction of fresh uncertainty relating to the currency is a headwind. Today's declines challenge the market support initiatives introduced following June's crash. If the Chinese administration remains committed to supporting the market, and there is no reason to question that assumption, it is at this area one would expect support to come back in.

The Chinext Index of small caps tripled in 2013 to little acclaim, spent most of 2014 ranging and jumped 166% between January and its June peak. It has paused in the region of the 200-day MA over the last two months but needs to hold the lower side of that range if a further test of underlying trading is to be avoided.

The Shenzhen B-Shares surged out of a six-year range in November and accelerated to its June peak. It is now testing the lower side of its 2-month range and will need to rally soon to question potential for a further test of underlying trading.