The next move after a weak March could be a useful rally

Thanks to a subscriber for this report by Warwick Grigor for Far East Capital Limited focusing on Australia. Here is a section on the property market:

Have you noticed how much debate there is over so many issues that we confront? It is usually a face-off between those who can see an issue clearly in one corner, and those with vested interests in the other. As an example, the global warming debate is one that has been ongoing for a long time largely due to the inability to achieve consensus amongst scientists and the complications of obtaining meaningful measurements. But something that should be less controversial is the state of the property market in Australia. Do we have a bubble or don't we?

We do have an extraordinarily strong market that cannot go on forever. The bigger the cycle upturn the harder the fall on the other end. The collapse of the mining and resources boom was proof of that. After every party there is a hangover. We are seeing many initiatives being proposed, and some undertaken, that are designed to take the heat out of the market. Yet there will still be pain in due course especially for the inexperienced property investors who have been dragged into euphoria of booming property prices.

In the meantime we see arguments for and against a bubble and an impending collapse. Perhaps we should be focusing on sensible measures rather than trying to do a King Canute. You don't have to wait for direction from the government or the regulators in order to think ahead. Start getting your finances in order now so you can weather the storm.

Here is a link to the full report.

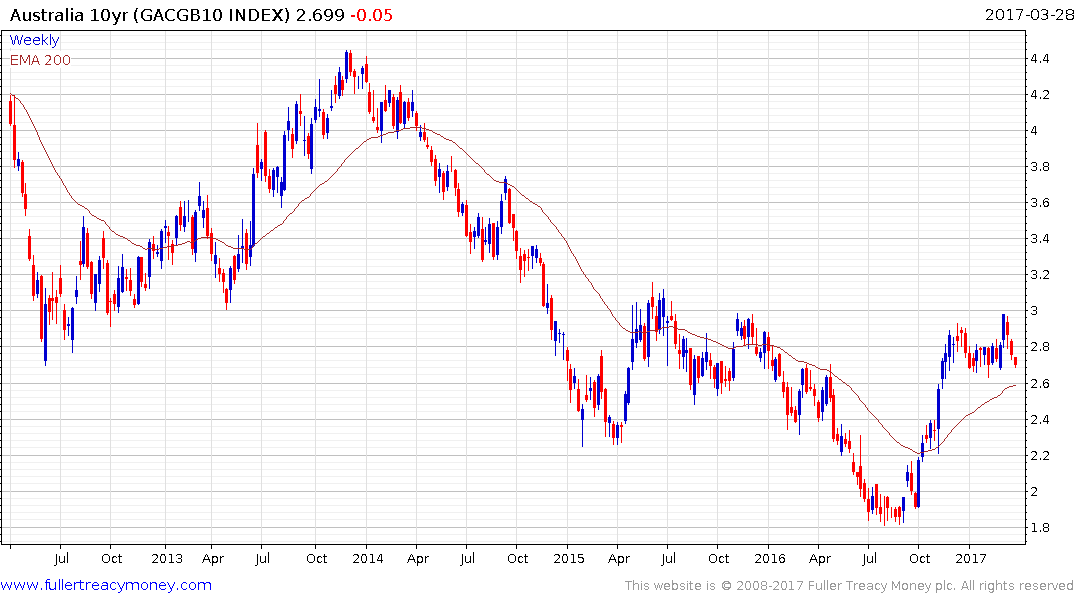

Australian government bond yields might not be as low as those in Europe, Japan or the USA but they have been trending lower for just as long. Relative seclusion from the credit crisis in the USA and sovereign debt and banking crisis in Europe as well as proximity to the commodity demand growth markets of Asia has allowed Australia to go a long time without a recession. That suggests what happens in China is likely to have much greater influence on Australia than anything that goes on in North America or Europe.

This is not the first time the 10-year yield has sustained a move above the trend mean in the last five years and it will need to hold the 2.6% level if supply dominance is to be given the benefit of the doubt. The potential issue for housing in Australia is that is dominated by floating rate or short fix mortgages which expose borrowers to a lot of interest rate risk. That’s a potential problem if yields do finally break their downtrend.

The S&P/ASX 200 Index’s trend has become more consistent over the last few months with shallower reactions and a clearer progression of higher reaction lows. It is now testing its recovery highs and sustained move below 5680 would be required to question potential for additional higher to lateral ranging.

The S&P/ASX 300 Banks Index rallied to break an 18-month downtrend in October and continues to extend its rebound.

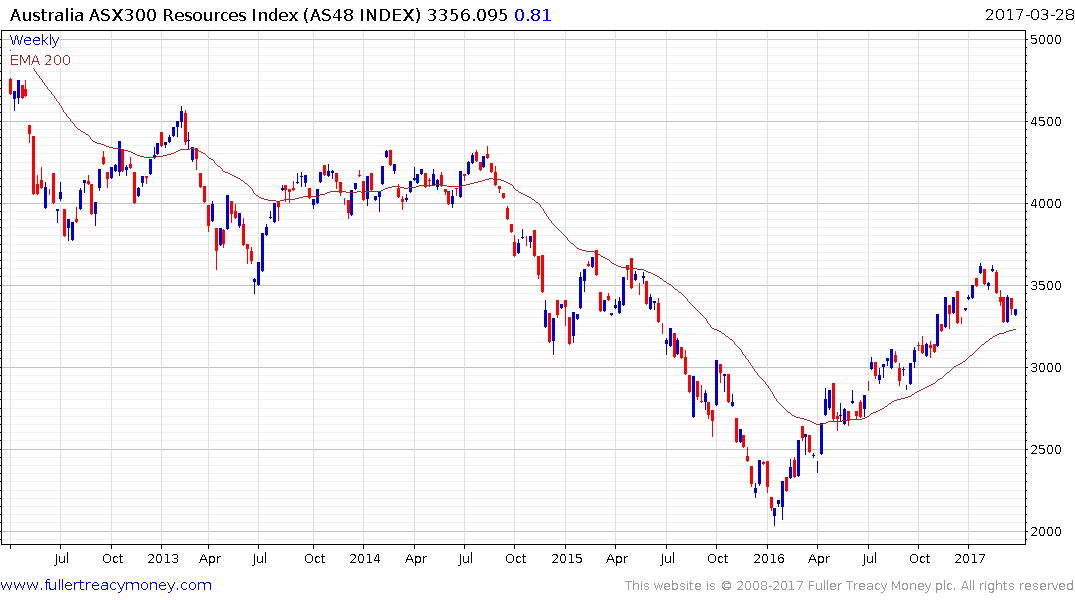

The S&P/ASX 300 Resources Index has now unwound its overextended condition relative to the trend mean and a sustained move below it would be required to question the medium-term upward bias.

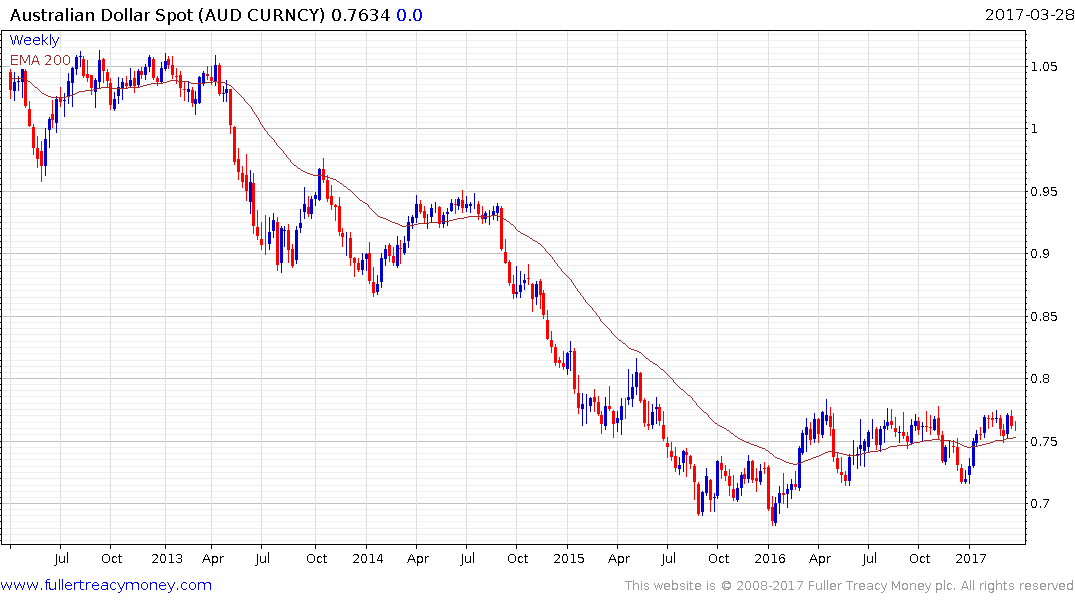

The Australian Dollar continues to trade in the region of the upper side of a yearlong range but a sustained move above 77¢ would be required to signal a return to demand dominance.