The New Bond Market: Bigger, Riskier and More Fragile Than Ever

This article by Colin Barr for the Wall Street Journal may be of interest to subscribers. Here is a section:

In the U.S., household, corporate and government debt amounted to 239% of gross domestic product in 2014, the Bank for International Settlements estimates, compared with 218% in 2007.

The U.S. isn’t alone. Dollar credit to nonbank borrowers outside the U.S. hit $9.6 trillion this spring, the BIS said, up 50% from 2009. Repaying those loans and bonds will become costlier in local-currency terms should the dollar rise, as it often does, when the Fed goes ahead with tightening, potentially stressing large borrowers such as emerging-market companies.

Domestically, the rise of large bond funds has created new risks. As the funds have grown, so has cross-ownership of the same bonds, increasing the likelihood of contagion if one manager starts selling, the International Monetary Fund says. Regulators worry that many investors may not know what is in their funds. A market downswing could lead to rising redemptions of fund shares, prompting funds to sell assets to raise cash and amplifying selling pressure across the market.

Since 2007, $1.5 trillion has gone into U.S. bond mutual and exchange-traded funds holding assets from government bonds to corporates and municipal debt, according to the Investment Company Institute. That compares with $829 billion into comparable stock funds.

Bond mutual and exchange-traded funds now own 17% of all corporate bonds, up from 9% in 2008, according to the ICI. In periods of market stress, more-concentrated mutual-fund ownership tends to mean larger price drops, the IMF said last year.

Individual bonds do not trade on an exchange but bond ETFs do. As the size of the exchange traded bond fund market has grown so has the risk that they are subject to the same intraday or intraweek volatility as stocks.

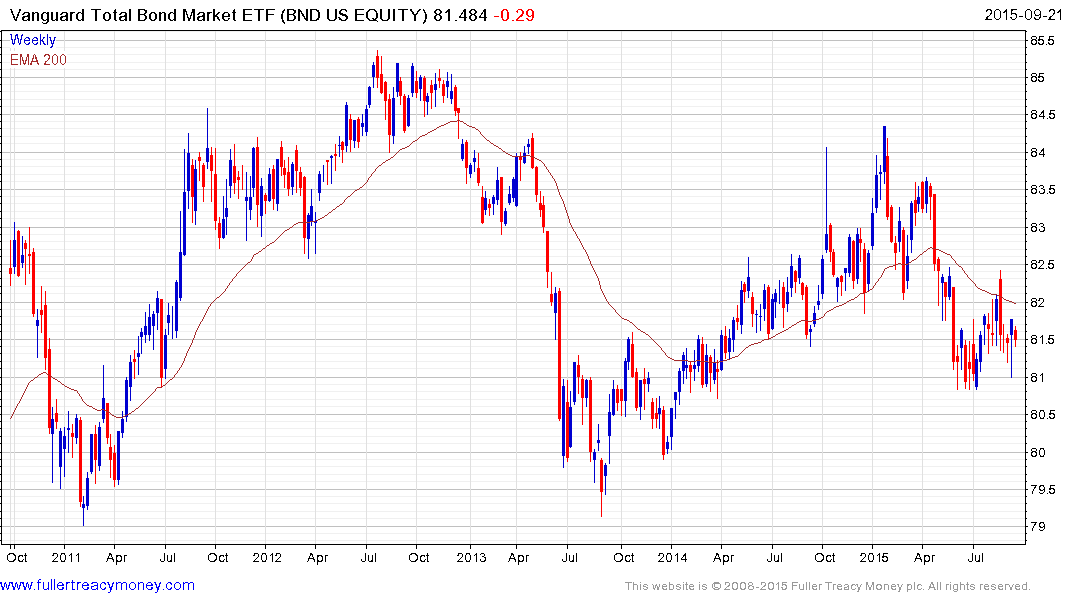

The Vanguard Total Bond Market ETF has $26.67 billion in assets. It encountered resistance in late August in the region of the 200-day MA and a sustained move above $82 will be required to question medium-term supply dominance.

The iShares iBoxx $ Investment Grade Corporate Bond ETF has $22 billion in assets. It experienced a deep decline earlier this year but has so far failed to rally meaningfully. A sustained move above the trend mean, near $118, would be required to signal a return to demand dominance.

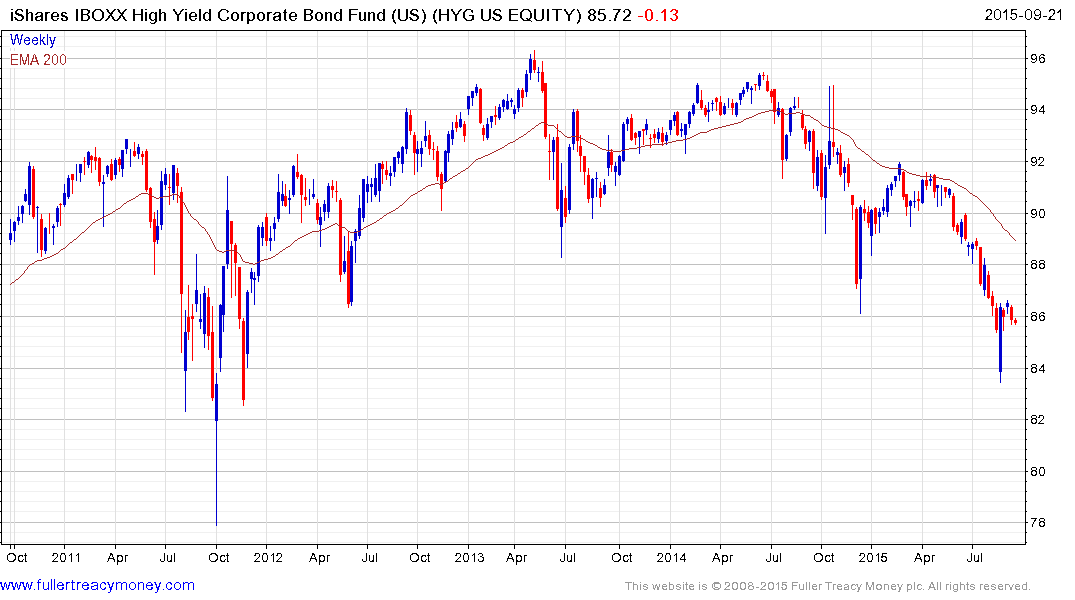

The iShares iBoxx $ High Yield Corporate Bond ETF has $13 billion in assets. It bounced from a deep oversold condition in late August but will need to sustain a move above the trend mean to signal a return to demand dominance beyond short term steadying.