Thought of the Day: Politicalization of the Fed

Thanks to a subscriber for this edition of Sydney Williams’ thoughtful note. Here is a section:

“Permit me to issue a nation’s money and I care not who writes the laws,” so, allegedly, once said Mayer Amschel Rothschild (1744-1812). Last week, Fed Chairwoman Janet Yellen took advantage of falling commodity prices, turmoil in markets, an anemic recovery in the U.S. and weakening economies overseas – especially China – to leave the rate on Fed Funds at the zero to twenty-five basis points where it has been since December 17, 2008. She also cited a lack of inflation and concern that a stronger dollar would further inhibit economic recovery at home.

What she did not mention was the effect of higher interest rates on debt owed by the federal government and, thus, its fattening impact on the deficit. Federal debt is about $18.2 trillion. That number excludes debt owed by state and local governments, as well as funds owed by agencies. And, of course, it does not include future obligations of social welfare programs like Social Security, Medicare and Medicaid. Deficits in fiscal 2015 will add about $400 billion to existing debt. A one percent increase in interest rates would up the deficit by about 40 percent. Should rates revert to normal levels, the deficit would rise to a trillion dollars. Ms. Yellen is surely mindful of the salutary effect low interest rates have had on annual federal deficits.

Here is a link to the full report.

The impact rising interest rates will eventually have on the cost of financing for governments is a very relevant issue which has not been discussed in any lengthy by other financial commentators. The danger in raising rates too soon is that economic growth is not strong enough to carry the burden for both the government and consumer sector and the Fed would then be led back to an embarrassing situation where they may have to cut rates again.

.png)

The ECB did just that in 2011 when it raised rates twice but had to quickly reverse course. Ultimately rates fell well below the level that prevailed before the premature hikes.

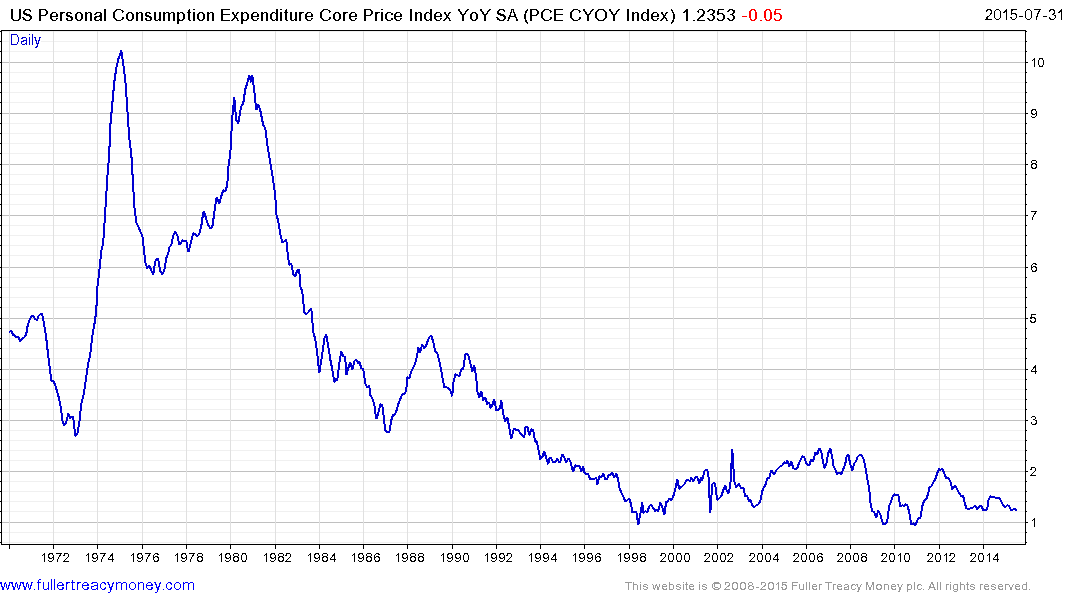

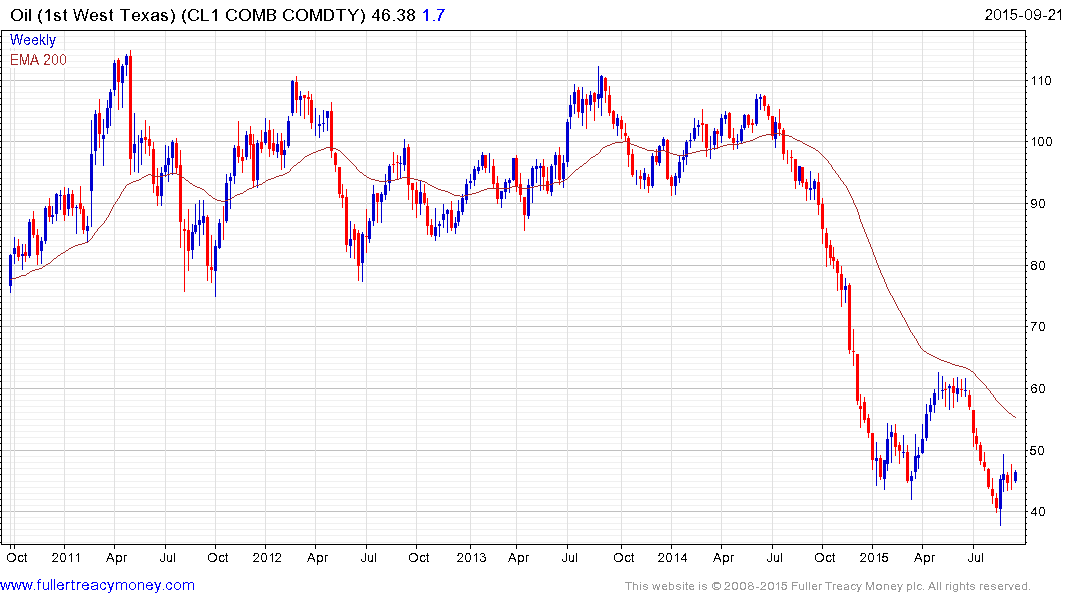

The YoY PCE Deflator was last updated in late July and the August reading is due out next week. A year ago oil prices were approximately double what they are today. The accelerated portion of its decline bottomed in January and prices today are pretty close to what they were then.

That would suggest the impact of the collapse in oil prices will not wash out of the statistics until at least February 2016.

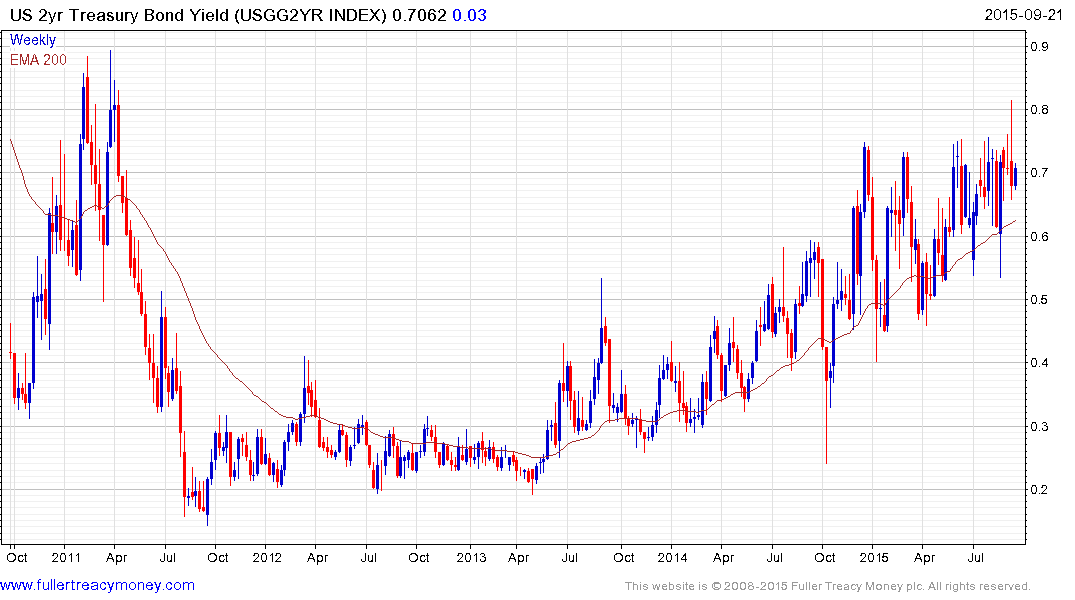

Five months is a long time in markets and some pricing in of an uptick in reported inflation may already be evident. 2-year yields pulled back very sharply on Friday but the medium-term progression of higher reaction lows remains in evidence. As long as that sequence holds we can conclude investors are betting rates will rise at some point over the next year.