On the Couch

Thanks to a subscriber for this memo by Howard Marks for Oaktree Clients which I highly recommend reading both for its behavioural insights and level headed perspective on the markets as they stand today. Here is a section:

There is no immediate connection (other than for companies doing business there) between the slowdown and the price decline in the oil patch, on one hand, and the general creditworthiness and desirability of high-risk debt on the others. And yet, over the last few months, pronounced changes occurred in the market for distressed debt:

After a period of very stable prices – ever for “iffy” debt 0 some securities have “gaped down” in the last few months (i.e. fallen several points at a time rather than correcting gradually). In particular, investors have become highly intolerant of bad corporate news.

For the first time since 2008-09, the debt of some companies outside of energy and mining has fallen from 80 to 60 and others from 50 to 20.

There is a general sense among my colleagues that investors have gone from evaluating securities based on the attractiveness of their yield (with companies fundamentals viewed optimistically (to judging them on the basis of the likely recovery in a restructuring (with fundamentals viewed pessimistically).

The capital markets have begun the swing from generous toward tight, as is their habit. Thus, whereas they used to find it easy to refinance debt I order to extend maturities or secure “rescue financing” now it’s hard for companies – especially those experiencing any degrees of difficulty – to obtain capital.

On December 7, Oaktree held a dinner in New York for equity analysts who follow out publicly traded units. Bob O’Leary, a co-portfolio manager of our distressed debt funds, planned to be among the hosts. But he called me on December 3 with a question I hadn’t heard in a long time from my distressed colleagues. “Would you mind if I don’t come? There’s too much going on for me to leave the office“. The change in investor attitudes had created investment opportunities where they hadn’t existed just a few months before – in some cases out of proportion to the change in fundamentals.

Developments like these are indicative of rising pessimism, skepticism and fear. They’re largely what Oaktree hopes for, since – everything else being equal – they make for vastly improved buying opportunities. But note that we may be just in the early stages of a downward spiral in corporate performance and credit market behaviour. Thus, while this may be “a time” to buy, I’m far from suggesting it’s “the time”.

This is balanced piece and it’s really worth taking time over the weekend to read it in full.

In August I described the price action following the volatility across ETFs as a massive reaction against the prevailing trend and therefore confirmation of Type-2 topping characteristics. Following such an event investors invariably ask if anything has really changed and whether the widespread experience of being stopped out of positions will have a lasting effect. At the time I drew parallels with the flash crash in 2011 because that was the last time investors had experienced a similar event albeit now from a higher level.

I’d like to return to that comparison today because following the flash crash in 2011 people sold the rally that followed the decline much as they have done on this occasion although with a somewhat delayed reaction. There were also similar alerts emanating from major brokerages to sell everything. RBS’s much publicised call to do that this week was one such example and I was chatting with a US based subscriber yesterday who said he had heard similar advance from a number of banks. That only heightens the emotional response of investors because sharp declines compound the fear that they may be selling too late.

.png)

In 2011 the retest of the low did not hold and volatility persisted for an additional three months before an emphatic failed break, higher reaction low and eventual higher high by September. On this occasion the August low has been retested twice and the S&P make a new intraday low today while the VIX closed at its highest level in four years. A slowdown in the pace of the decline and evidence that demand is returning beyond very short-term steadying will be required to begin to rebuild confidence.

This long-term chart of the S&P 500 highlights just how different current prices action is from anything posted over last six years. As a trend evolves we expect it to become more consistent as people make money and adhere to the bullish hypothesis. That happened between 2012 and 2014. Since then the trend has lost momentum which tells us the demand that drove the consistency of the trend from 2012 has lost impetus. As a result the bears are emboldened. A short-term oversold condition is evident so there is room for a bounce but it would need to persist in impressive style to begin to rebuild confidence.

There is a lot of lose talk flying concerning the risk of a 2008 drawdown. There are issues in the debt markets because just about anyone has been able to borrow money in an environment where spreads have been close to historic lows and central banks have been flooding the globe with liquidity. It’s a common sense point that there will be problems for companies that were overleveraged and this is particularly true of the energy complex where a great deal of debt has been sold. It is almost inevitable that a number of major bankruptcies among highly leveraged developers will occur this year. It’s even possible a sovereign such as Venezuela could default and Petrobras remains a high risk prospect not least because it has so much debt outstanding. It’s an altogether different question whether this is capable of having the disruptive effect that the US subprime crash did and I share Howard Marks view that the two are not analogous.

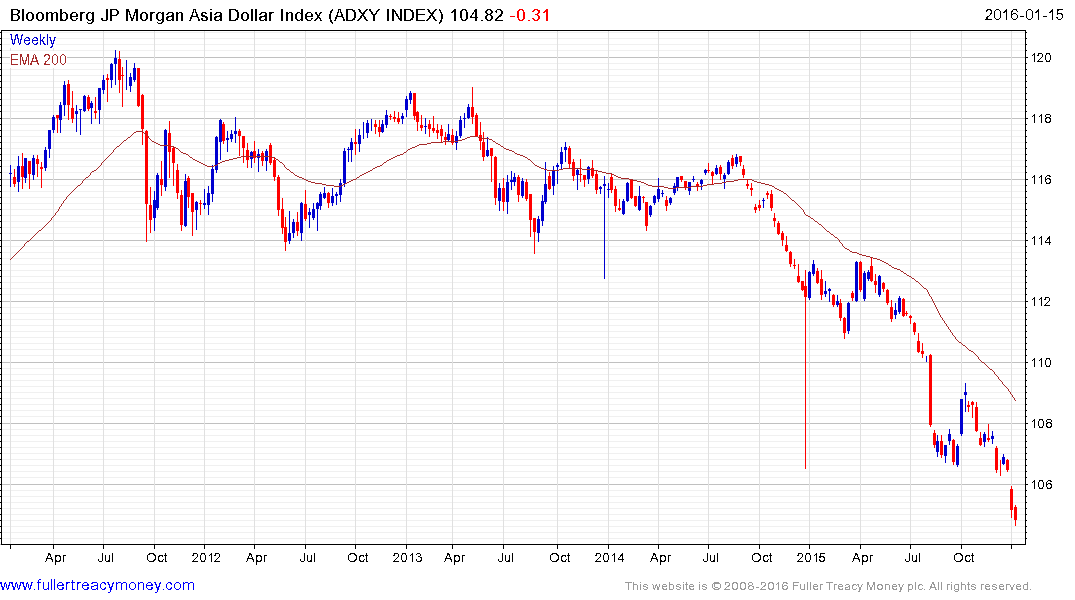

I found his comments on China’s influence of particular note not least his points on the relative dependence of the USA on China’s economy. These are important points but I believe it is also worth considering the counter argument for a sense of balance. China is not a major destination for US exports on aggregate but it is a major destination for exports from commodity producers and other countries in the rest of Asia. Many of the companies concerned have taken out Dollar denominated debt and the fall in commodity prices coupled with reduced Chinese demand is an issue that has not yet been fully explored because it is as yet unclear who holds the debt and which banks are on the hook for it. This uncertainty is perhaps the greatest outstanding risk because we simply don’t know how intertwined Dollar borrowers are with the USA’s financial system.

The Asia Dollar Index is accelerating lower but there is no evidence yet support has been found.

Back to top