MVIS Announces A Significant Methodology Change for the MVGDXJ

Thanks a subscriber for this report from Scotiabank which arrived while was in Asia. Here is a section:

We think accounts should take notice of this list because there could be as much as USD 3.2B to trade in these names at the June 2017 quarterly review (assuming our forecast holds). We estimate accounts could buy USD 1.3B in the new Canadian additions and sell USD -1.8B for funding.

What to expect from the Benchmark Change? This is not the first benchmark change for the GDXJ. Market Vector Index Solutions (previously known as Market Vector Indices) expanded the universe for the Junior Gold Miners Index after the ETF provider ran into similar problems in 2014. Specifically, Market Vector Indices allowed larger companies to qualify for the index by changing the requirements from needing 90%-98% (of the full market capitalization of the eligible universe) to needing 80%-98%. According to our analysis, the market capitalization range for new constituents effectively doubled to USD 95M – USD 995M (from USD 95M – USD 448M under the previous methodology). The buffer zones (for existing constituents) also expanded to include constituents that ranked between 75% and 80% (of the eligible universe) versus 80% and 90% under the previous methodology. The previous methodology change was announced on October 13, 2014 and took effect at the December 2014 quarterly review.

Overall, the 2014 index additions outperformed the GDXJ by 9.8% between the date the methodology changes were announced and the determination date for the index review. The additions outperformed the GDXJ by an additional 14.0% between the determination date and the effective date of the index review, bringing total outperformance to 23.8% from the announcement date of the methodology changes. Note, the 2014 additions had a 3.6% post-announcement pop, so accounts that cautiously waited for a methodology change could still wade into the trade post-announcement and benefit from the index flows.

Here is a link to the full report.

The fact that the junior gold miners ETF is being reconstituted to allow more large companies entry begs the question why have a juniors ETF in the first place? The answer of course is that the fund has grown to $4.2 billion under management which is a lot of money to invest in small companies and needs the room to buy larger cap companies. The result is that there will be little difference between GDX and GDXJ.

The fund has been underperforming the gold price and moved to a new reaction low this week before steadying today. A short-term oversold condition is evident so there is scope for a relief rally. However a sustained move above $40 would be required to signal a return to demand dominance beyond the short term.

Gold continues to hold the upward bias evident since December and has steadied above $1250. A break in the progression of higher reaction lows, currently near $1240 would be required to question potential for additional higher to lateral ranging.

Silver has fallen for nine of the last ten trading sessions and a short-term oversold condition is evident as its tests the $17 area. This area offered resistance between November and January and support in March so it is potential area where demand for at least a relief rally could be reasserted. A clear upward dynamic would confirm that hypothesis.

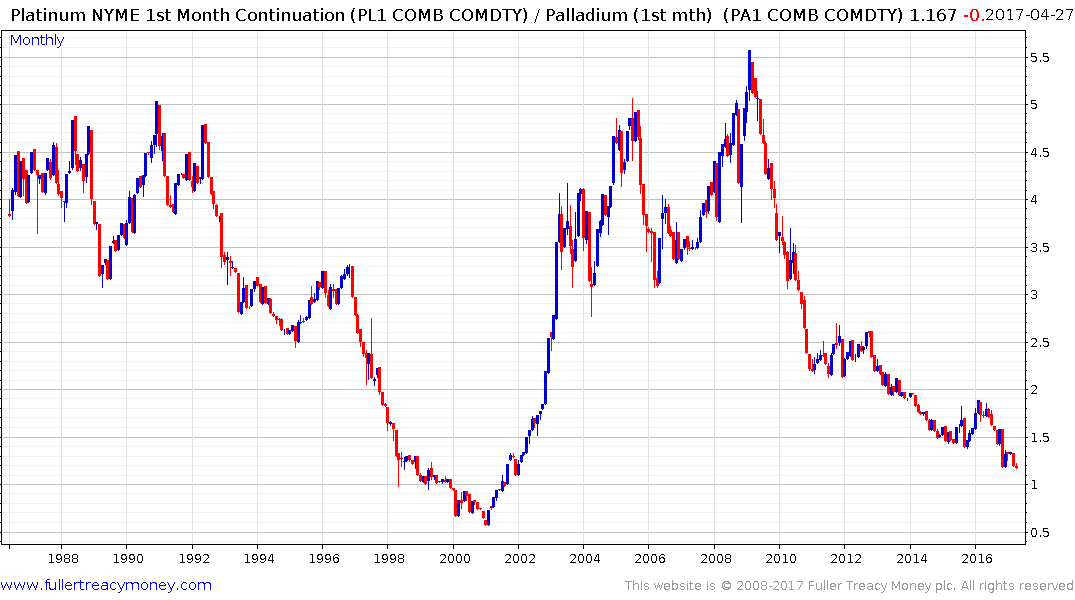

This platinum/palladium ratio is one of the most interesting in the precious metals sector at present. The last time palladium was this close to trading above parity with platinum was in 2000. That suggests the potential for retooling at catalytic converter manufacturing assemblies to favour platinum are becoming increasingly compelling. A break in the ratio’s progression of lower highs would potentially signal a switch is underway.