Email of the day on China's deleveraging

Good morning Eoin. I attempted to send this message from my mobile which I fear I bungled. I expect you must have a mountain of email daily, not least the amount which must be caught up after your travels. I hope you had a great trip. You may recall, I asked a month ago for your thoughts on liquidity in China. The Regulators have continued to rein in, essentially squeezing out smaller banks. I found it interesting that the Govt took a survey of banks regarding their recent policies, or is that positive. In any event, I will re-produce the article, I refer below:

Thank you for your warm regards and the attached article from Market News. We had a wonderful trip to Asia. Thanks to Mrs. Treacy’s guangxi, I had the pleasure of having lunch with a senior Citic Securities dealer while in Beijing in 2014 who explained that the only game in town at the time was lending to private investment clubs which he referred to as “Chinese hedge funds”.

The Chinese government’s response to the credit crisis was an unprecedented stimulus program. However by 2012 the funds had been exhausted and the banks had to come up with new way to source cash for lending to companies, infrastructure and real estate projects. The answer was to tap into the nation’s massive pool of savings mostly held in deposit. By offering fixed returns in the order of 10% they encouraged cash off the side lines and most particularly from Communist party apparatchiks. With so many government-connected people investing the structures might not have had explicit government guarantees but they were certainly implicit. That created the conditions for the private lending sector to explode in size over the last three years.

As with any other bull market in financial products there have been excesses and a great deal of cross investing in these products. Coupled with the fact that the Chinese market has gone through a massive reorientation in the last 18 months with the launch of options, futures and credit default swaps the risk of an unruly unwind has increased. That is why the government has stepped in to try and limit the leverage in the financial system.

They got a taste of what a liquidity event might look like in December when 3-month Shibor (Shanghai Interbank rates) surged 120 basis points in a month. The decade long chart highlights just how volatile the rate is which is a reflection of the fact that despite massive development China is still very much an emerging market. However it is also worth remembering that the banks are essentially arms of the government which means they have substantial leeway in maintaining open credit lines.

The Renminbi has been reasonably steady since the turn of the year but it is still in a medium-term downtrend when we take a longer-term perspective. Considering the challenges the Chinese economy faces in attempting to effect a smooth financial sector deleveraging they need a weaker currency.

The recent underperformance of Chinese banks is also a reflection of the tightening the administration’s efforts to curb leverage has resulted in. Meanwhile the Shanghai A-Share Index has at least steadied in the region of the trend mean.

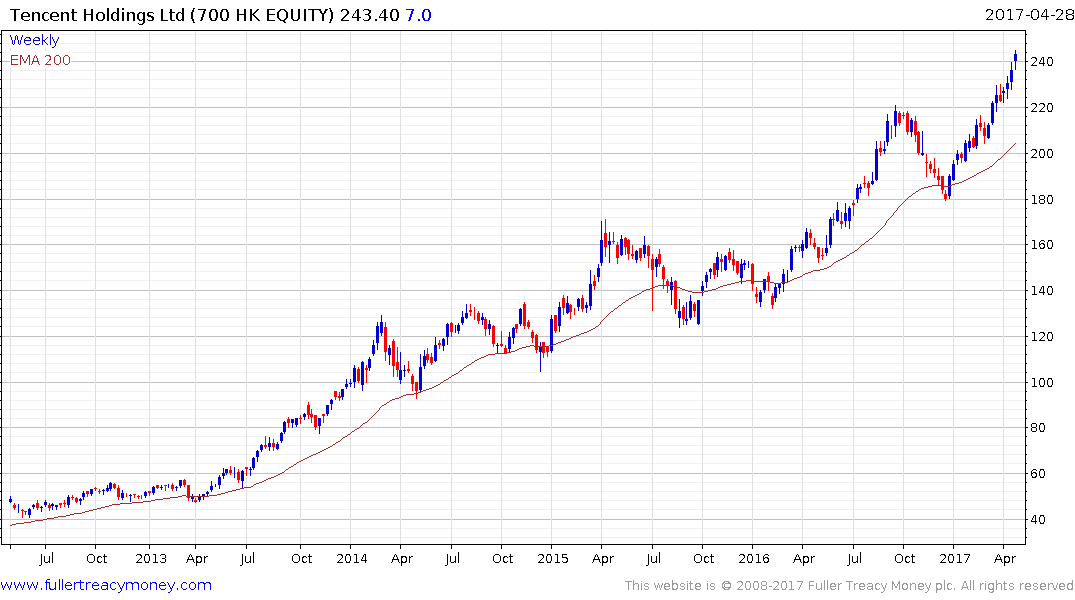

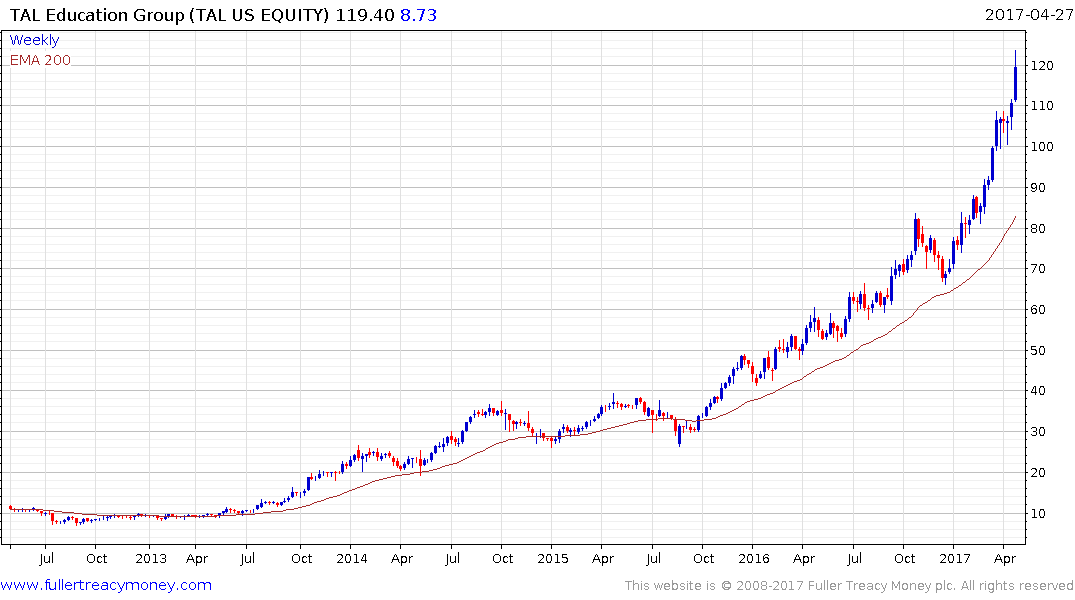

The technology sector, with many of the biggest companies listed overseas, has been a clear outperformer. Tencent Holdings which is listed in Hong Kong and TAL Education Group which is US listed are both rather overextended relative to their trend means at present and susceptible to pullbacks.