Musings From the Oil Patch December 2nd 2014

Thanks to a subscriber for this edition of Allen Brooks ever informative report. Here is a section:

Given the monetary policies recently adopted the central banks in the European Union, Japan and now China, one has to assume that the U.S. dollar’s value will continue to strengthen putting increased downward pressure on global oil prices. A strong dollar is additive to the downward demand pressures from weak economic activity, demographic challenges, changes in attitudes toward the use of oil and inroads from renewables. The combination of these forces is likely to keep annual oil consumption growth to one million barrels a day or less for the next few years. It is quite possible that we could be living in a world where more than a million barrels a day growth in consumption represents a boom rather than the norm.

?In that environment, the question becomes what will substantially lower prices – as a result of the OPEC meeting decision of last week – mean for global economic growth in the short-term? In our view, the Saudi Arabia and OPEC game plans are less about targeting Russian, Iranian and U.S. shale production, although those are beneficial outcomes, but more about restarting European and Chinese economic activity. Demand growth is what OPEC needs for its long-term future. Low oil prices will also help Saudi and OPEC limit the growth of new long-term oil supplies such as Canadian oil sands and deepwater output that should also help improve the relative attractiveness of Middle Eastern oil. Unfortunately, restarting demand may take longer to accomplish than many anticipate. Therefore, the pain petroleum companies are just beginning to experience will need to be endured for some period before the industry fundamentals change sufficiently to restore the good times we have recently enjoyed.

Here is a link to the full report.

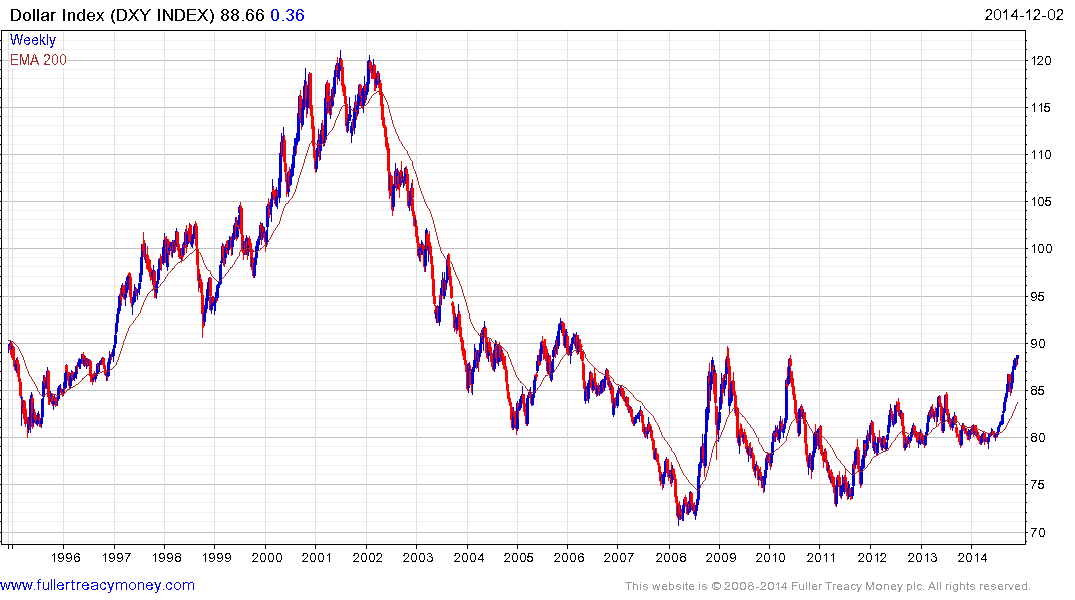

Technological innovation across a whole range of sectors and the productivity growth that is being achieved as a result, the USA’s lower cost of energy particularly natural gas which is attracting industry, the demographic dividend of the millennials and immigrants as well as the effect on asset prices of loose monetary policy have all helped stabilise the US economy. Its relative strength at the present time when other major economies are still easing has helped the Dollar appreciate meaningfully.

The Dollar Index is now testing the upper side of its six-year base formation and while there is potential for some consolidation in the current area, a sustained move below the 200-day MA would be required to question medium-term potential for additional upside.

The Asia Dollar Index is testing the lower side of a three-year range and a clear upward dynamic will be required to question potential for additional downside.

While it would be a mistake to think of the Dollar’s influence on commodities in terms of a one to one relationship, there is no doubting that a stronger Dollar is a headwind for nominal commodity prices.

Back to top