Japan Adopts Negative-Rate Strategy to Aid Weakening Economy

This article by Toru Fujioka and Masahiro Hidaka for Bloomberg may be of interest to subscribers. Here is a section:

Bank of Japan Governor Haruhiko Kuroda sprung another surprise on investors Friday, adopting a negative interest-rate strategy to spur banks to lend in the face of a weakening economy.

The move to penalize a portion of banks’ reserves complements the BOJ’s record asset-purchase program, including 80 trillion yen ($666 billion) a year in government-bond purchases, which was kept unchanged at the board meeting. By a 5-4 vote, Kuroda led his colleagues to introduce a rate of minus 0.1 percent on certain excess holdings of cash.

Long a pioneer in adopting unorthodox policies to tackle deflation and revive economic growth, the BOJ is now taking a page out of European policy makers’ playbooks in the goal of stoking inflation. The yen tumbled after the announcement, which came after Kuroda just last week rejected the idea of negative rates.

“This clearly shows the BOJ wanted to weaken the yen and raise the price of import goods and boost inflation,” said Daisuke Karakama, an economist at Mizuho Bank in Tokyo. “We don’t know this negative rate policy will be good for the economy in the end,” he said, adding that success in Europe doesn’t guarantee the same for Japan.

JGB yields plunged on today’s news since a yield of 0.1% is still better than receiving negative 0.1% from deposit. In addition to continued BoJ purchases, in line with its quantitative easing program, this has sent yields to record lows with little prospect for significantly higher levels while the policy persists.

I had illustrated previously that Yen strength was a symptom of deleveraging and indicative of the risk-off environment that has prevailed in global stock markets over the last couple of months. Today’s upward dynamic confirms a return to Dollar dominance at the lower side of the more than yearlong range and is a potent signal we may now be entering a fresh risk-on phase.

In many respects this takes us back to 2011 when the Fed’s 2nd quantitative easing program ended and the market was trying to adjust to the end of persistent central bank largesse. At the time the Fed was by far the largest supplier of liquidity to the global market but now that position is filled by the BoJ, PBoC and ECB. Today’s BoJ action suggests short-term oversold conditions are likely to be unwound over the coming weeks.

Perhaps the greatest uncertainty right now is how many times the Fed will raise rates this year. They say as many as four while the bond market suggests it may be one or none. There is no measurable inflation, not least because commodity prices have been trending lower for four years. With unemployment at close to optimal levels, the uptick in wage growth late last year was probably the catalyst for the Fed hiking rates.

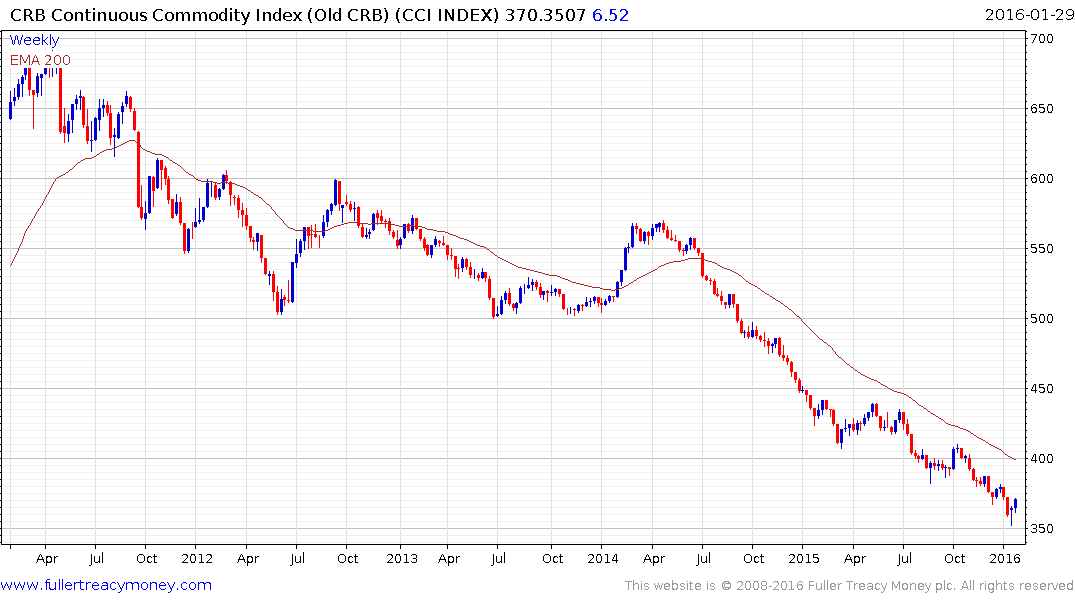

This question centres on to what extent external factors will compete with domestic considerations to frame any further decisions. Oil prices have found at least a near-term low and are already 27% off their nadir. The Continuous Commodity Index is deeply oversold relative to the trend mean so potential for a reversionary rally is gaining impetus. If commodity prices both rally and hold their gains that will negate many of the deflation arguments that have prevailed over the last six months. If wage growth continues to improve then the Fed will have justification for raising rates. Of course those are big ifs and the impact on emerging markets of Dollar strength is still a major risk factor.

The Dollar Index has been ranging below the psychological 100 level since early 2015 and continues to find support in the region of the 200-day MA. A clear move below the trend mean would be required to question medium-term scope for a successful upward break.

Back to top