Inflating inflation fears

Thanks to a subscriber for this article from Saxo Bank which may be of interest. Here is a section:

Wage pressures are a key concern

Despite widespread news of tech layoffs, the January jobs growth of +517k sent a shockwave to the markets. Unemployment rate touched a 53-year low as service providers expanded their activities. Likewise, jobless claims data and surveys on unemployment all continue to point at hiring and wages would remain on an upward path.With the demand and supply imbalance in the labor markets continuing, companies are feeling wage pressures eat into their margins. As the US consumer is still holding up well even in the wake of high inflation and interest rates, companies with pricing power will pass on these wage costs to the consumers, thereby creating more upside pressures to inflation and a potential wage-price spiral.

Re-acceleration of cyclical growth

Transition from a recession to a goldilocks/soft-landing narrative to the current no-landing/acceleration narrative isn’t all positive for the markets. The Atlanta Fed GDPNow model estimate for real GDP growth in Q1 is now at 2.7% from 0.7%, which is hardly a sign of recession or stagnation.Overall, recent economic data suggests that the US economy is reheating, and the market is moving to price that in by bringing the terminal rate forecast higher and driving out the rate cuts priced in for this year to 2024. This also brings back the risk of higher inflation. The reopening of the Chinese economy also brings fears of an inflationary impulse through commodity and raw material prices.

Cleveland Fed economists Randal Verbrugge and Saeed Zaman have said that it will likely take US inflation many more years than central bankers and financial markets expect to close in on 2% without a deep recession.

Upward repricing of the Fed path

Beyond cyclical risks, inflation continues to face upside threat from structural factors such as shortage of labor, deglobalization as well as the energy supply crunch. US breakevens are signalling renewed concern that inflation will stay elevated in the shorter term, with the 2-year rate above 3% for the first time since August 2022 and the 10-year rate holding at around 2.5%.As such, market expectations of the Fed path have seen a dramatic shift from expecting a pause/pivot to now pricing in a terminal rate of 5.4% from sub-5% a month back. Calls for 6-7% terminal rates have also picked up. But the Fed has already transitioned to a 25bps rate hike pace, and it would potentially be a credibility issue if they were to move back to 50bps rate hike increments. So, a longer tightening cycle looks like the most likely outcome.

Retail sales are still strong despite a tighter interest rate environment. That is supporting the employment outlook and giving the impression of a strong economic expansion. The only way I can think of to describe that succinctly is as an inflationary boom. There is clear evidence of a more inflationary bias to consumer sentiment with people accelerating purchasing decisions.

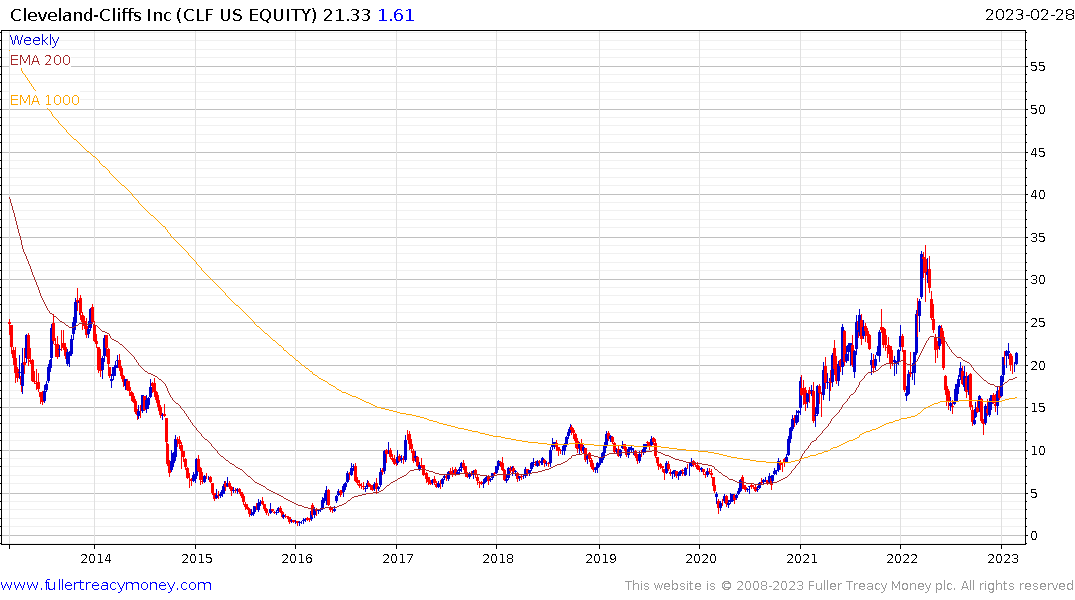

Cleveland Cliffs raised prices again yesterday because “we can”. The automotive sector is building more cars and the company believes they can easily pass on the higher cost of steel.

Meanwhile Nestle continues to expect to raise prices but the share broke below the 1000-day MA today. It needs to rebound in a dynamic manner to check the slide and signal a return to demand dominance.

In the early stages of an inflationary move companies regain pricing power. That allows the stock market to offer a clear hedge against inflation. However, as inflation persists, the ability of companies to continue to raise prices hits some consumer resistance. That is what we are potentially seeing now. The breakdowns in Nestle, Pfizer, Johnson & Johnson and other quality stocks suggests both uncompetitive dividend yields and resistance to higher pricing.

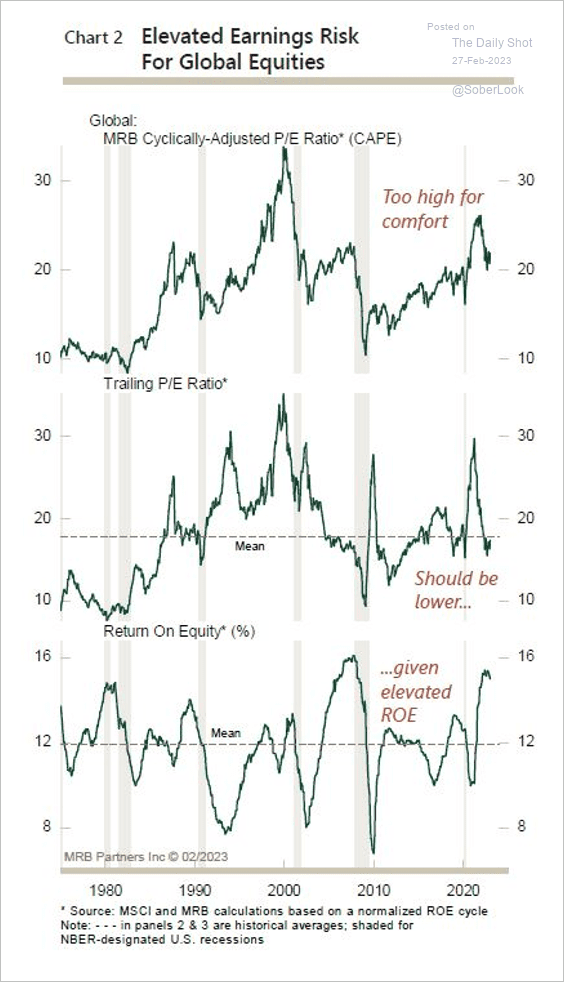

This graphic from MRB highlights how return on equity is probably peaking. That suggests lower valuations are inevitable. There is every reason to expect that tighter monetary conditions will catch up with prices in due course. The worst case scenario would be an inflationary bust because that would inhibit central banks from adjusting policy as required.