Half-Trillion-Dollar Exodus Magnifying U.S. Bill Shortage

This article by Liz Capo McCormick and Daniel Kruger for Bloomberg may be of interest to subscribers. Here is a section:

During the past five years, America has enjoyed some of the lowest financing costs in its history as the Fed held its benchmark rate close to zero and bought trillions of dollars in bonds to restore demand after the credit crisis.

Based on prevailing Treasury bill rates, it costs the U.S. just 0.02 percent to borrow for three months as of 8:49 a.m. today in New York. In the five decades prior to 2008, the average was more than 5 percent.

Now, with traders pricing in a 58 percent chance the Fed will raise its overnight rate by July, speculation is building that borrowing costs are bound to increase. That’s made finding buyers for the nation’s debt securities even more important.

The sweeping rule changes in the money-market fund industry may help provide that demand. Since 1983, money-market funds have been permitted to keep share prices at $1, meaning a dollar invested can always be redeemed for a dollar.

Unnecessary Risk

Institutional prime money funds, which invest in short-term IOUs issued by companies known as commercial paper, are among the funds that will now have to report daily prices which may fluctuate based on their underlying holdings, according to rules adopted July 23 by the Securities and Exchange Commission.The SEC the will also give the funds the ability to impose fees on redemptions and lock up investors’ money for as long as 10 days when a fund faces an inability to meet redemptions.

The changes are intended to prevent a repeat of 2008, when the collapse of the 37-year-old, $62.5 billion Reserve Primary Fund triggered a run on other money funds and deepened the worst financial crisis since the Great Depression.

Still, investors using prime funds to manage their idle cash may find floating prices an unnecessary risk when differences in fund rates are so minimal, said Brian Smedley, an interest-rate strategist at Bank of America in New York.

He estimates about half the $964 billion held in institutional prime funds will flow into those that only invest in government debt and yield about 0.013 percentage point less, before the new rules become fully effective in 2016.

Governments have a knack for creating demand for their paper through manipulation of regulations. Exactly the same types of move have been introduced in the UK and Europe with regard to the insurance sector and the quality of paper they can hold to compensate for risk. Some commentators have wondered at the fact that the short end of the curve has not risen more as the prospects of Fed tightening increase. However the reality is that demand remains robust not least because of regulatory changes that necessitate funds hold short-term paper.

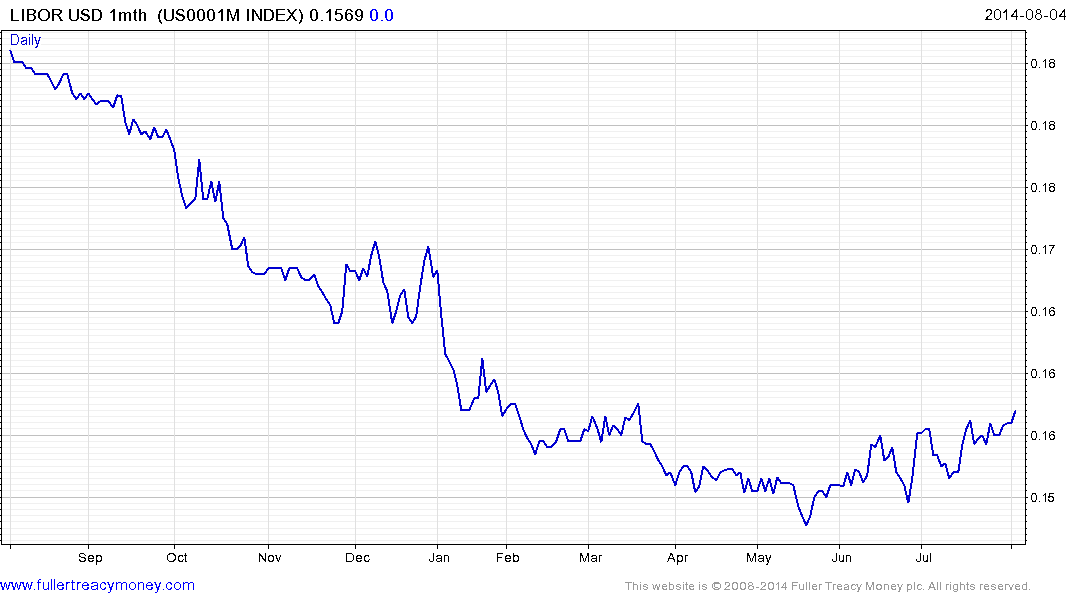

Nevertheless, 1-month LIBOR has been trending higher since May and a break in the progression of higher reaction lows would be required to question medium-term scope for additional upside.

This graphic from Bloomberg compares the US Treasury curve to itself over the last month, quarter and year. It is evident that any yield curve flattening that has occurred has been because long-dated yields have fallen rather than any meaningful move at the short end.

The spread between the 10-year and the 2-year has contracted from 260 to 200 basis points this year and a break in the progression of lower rally highs would be required to question potential for additional flattening. More than any other measure, this spread highlights the fact that credit conditions are slowly but surely tightening.

Back to top