Greek Borrowing Costs at Most Since 2012 Amid Political Turmoil

This article by David Goodman for Bloomberg may be of interest to subscribers. Here is a section:

As he attempts to expand the ECB’s balance sheet, President Mario Draghi said last week officials would act should current stimulus be seen as insufficient, and were considering other measures, including purchases of sovereign debt known as quantitative easing.

Loan RepaymentThe 130 billion-euro value of today’s allocation of targeted loans won’t cover the repayments lenders owe from a previous loan program. The amount euro area banks will borrow is less than the 148 billion-euro median estimate in a survey of 24 analysts. Predictions ranged from 90 billion euros to as much as 250 billion euros.

Between now and February, banks must repay 270 billion euros of outstanding loans issued at the end of 2011 to alleviate the effects of the euro area’s sovereign debt crisis.

The initial round of targeted loans in September raised 82.6 billion euros.“If there’s no major surprise to the upside this will be taken as another argument that QE needs to be implemented, so core and periphery bonds could benefit,” Daniel Lenz, lead market strategist for the euro area at DZ Bank AG in Frankfurt, said before the announcement. “The money will be used for repayment, so the net effect on the ECB’s balance sheet will be limited.”

European governments are often prone to using EU politics to influence decisions domestically, whether this is blaming the EU for overregulation when it meets resistance or for increasing taxes. Greece is currently engaged in a dangerous game of internal struggle which could have serious consequences if the prime minister fails to achieve his goals and an EU exit party comes to power.

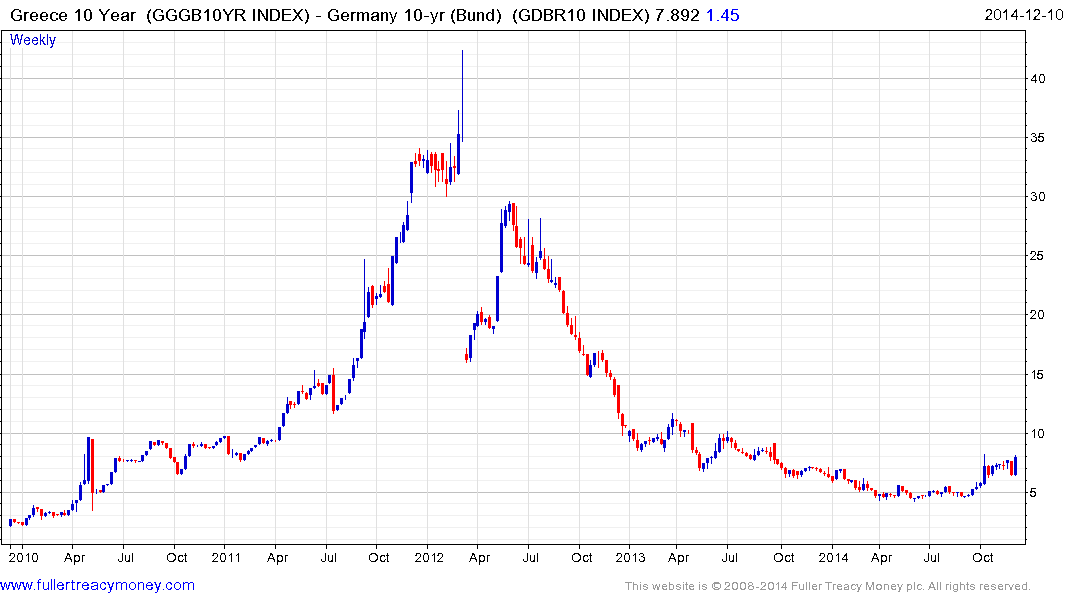

Greek 10-year yields have been ranging above the 200-day MA since early October and appear to be in the process of resolving to the upside. The spread over Bunds has an almost identical pattern since German yields are so low.

This action suggests that if Mario Draghi is looking for a reason to justify purchases of sovereign bonds, in order to keep the bond yields of other countries low, he will not have to look far.

Since the majority of Euro ABS have already been posted as collateral with the ECB and the pace of issuance is still low, the ECB will need to begin to purchase sovereign bonds if it is to achieve its goal of increasing the size of its balance sheet by 50%.

Back to top