Global watchdog tackles 'vulnerabilities' in leveraged loans

This article from Reuters may be of interest. Here is a section

Another issue is overly-aggressive adjustments to earnings before interest, taxes, depreciation and amortisation (EBITDA) of a company borrowing money, IOSCO said.

"Alongside looser covenants, there is evidence that headline debt-to-EBITDA may be understated," it said.

Investors have long worried that the EBITDA used, boosted by "add backs", may not be achievable, and that it masks the true amount of leverage.

"EBITDA adjustments based on future synergies, earnings and asset disposals should be made on a reasonable basis and borrowers are encouraged to provide clear justifications of these adjustments to investors," the proposed guidance says.

There is also a lack of transparency in the private finance market, which has experienced rapid growth, with private market assets under management reaching $12.8 trillion in June 2022, IOSCO said in a separate report.

U.S. companies have raised more money in private markets than in public markets in each year since 2009, it added.

"While the inherent opacity in private finance provides investors with some insulation from the transparency costs faced in public markets, it could also jeopardize availability of information that regulators and investors require to effectively assess risks," IOSCO said.

The size and lack of transparency within the leveraged loan market is daunting, and there are clear risks associated with the sector. However, it is also the one portion of the bond market that has been immune to interest rates despite investment grade selling off aggressively over the last 18 months.

The pace of “amend and extend” negotiations has accelerated over the last year. Those deals often stretch maturities in return for a sweeter coupon.

The pace of “amend and extend” negotiations has accelerated over the last year. Those deals often stretch maturities in return for a sweeter coupon.

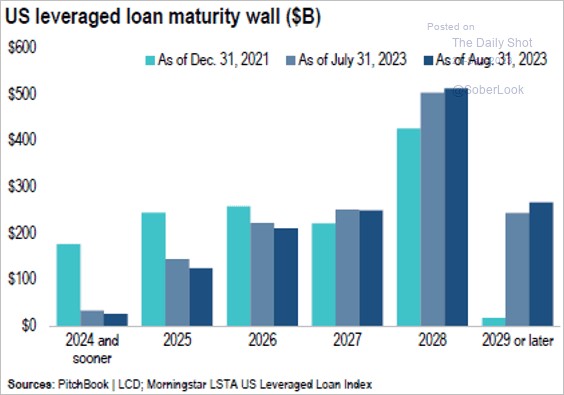

The net result is the total number of loans expected to mature in 2024 has contracted from around $180 billion to around $10 billion. 2025 maturities have similarly halved. Those loans have mostly been pushed out to 2028 and 2029 maturities.

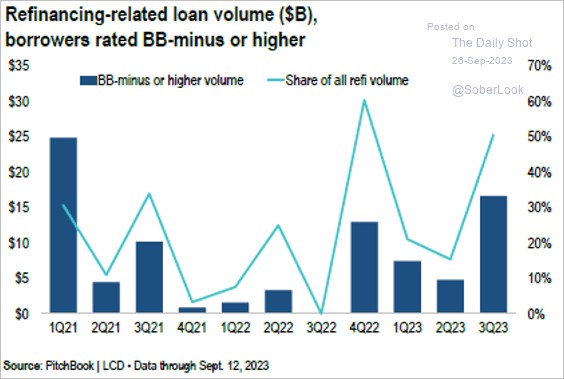

At the same time new leveraged loan issuance is running at an average of close to $25 billion a month.

At the same time new leveraged loan issuance is running at an average of close to $25 billion a month.

Netting off maturity stretching versus new issuance we have a sector worth $12 trillion which is still growing and providing the BB- sector of the bond market with all the capital it requires. This is the basis for the belief a soft landing can be achieved.

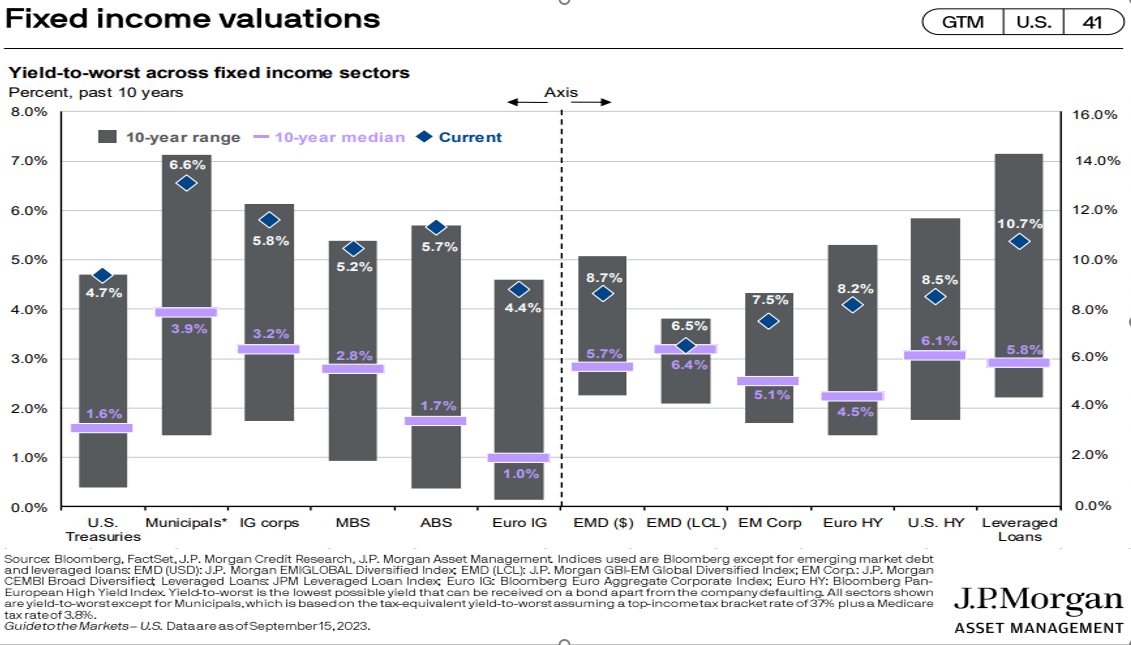

However, it is worth remembering that current yields are almost double the 10-year median. The majority of commentary has been on the dominance of the FANGMANT companies in the Nasdaq. The role of leveraged loans in the private lending sector is at least as important and possibly more so.

The same “amend and extend” has been evident in office space negotiations. Several landlords have been prepared to offer better terms to ensure their tenants stay put.

Private equity has been a boom industry for the last couple of decades but not all funds are created equal. As valuations trended higher over the last year bidding wars were common and funds overpaid for assets. Demand for debt to supplement businesses is running at a feverous pace. Larger, better capitalised funds appear eager to cannibalise their smaller more leveraged brethren.

Brookfield has failed to hold its attempted breakout. The share is now returning to the lows.

Brookfield has failed to hold its attempted breakout. The share is now returning to the lows.

The fact there is no ETF for leveraged loans and virtually no news on the sector suggests it is doubly important to attempt to keep abreast of.

Back to top