ESG in practice: assessing Food and Beverage companies' externalities

This report from the Candriam Academy may be of interest. Here is a section:

The market of protein foods is witnessing two key developments. The first is the efficiency drive, through new technology, among existing producers of animal protein food, such as milk, meat, fish or eggs. Better efficiency comes with smaller carbon footprint; indeed, the top 10% best performing farming businesses reduce theirs by double digits by adopting new innovative solutions.

Even more good news for companies: because most of the innovations work alongside existing production systems, their implementation will not require additional capital expenditure. There are also some products that target specific issues, such as cows belching methane – a greenhouse gas more potent in causing global warming than carbon dioxide. We now have a remarkable innovative food supplement that can suppress the production of methane by 30% in dairy cattle, and up to 90% in beef.The second type of innovations is about finding new sources of non-animal proteins. Everything from using canola to single cell proteins. Recent study reported that “considerable progress has been made towards the development and production of meat alternatives, including cultured meat, plant-based meat alternatives, microbial protein, edible fungi, microalgae, and insect protein.”

We expect a combination of advanced scientific expertise and investment will be required in the years to come not only to develop new sources of proteins but also test how safe they are for human health and well-being. In the meantime, the diet is not the only factor that impacts our climate and other sustainability factors, it is also the operation of the supply chains themselves.

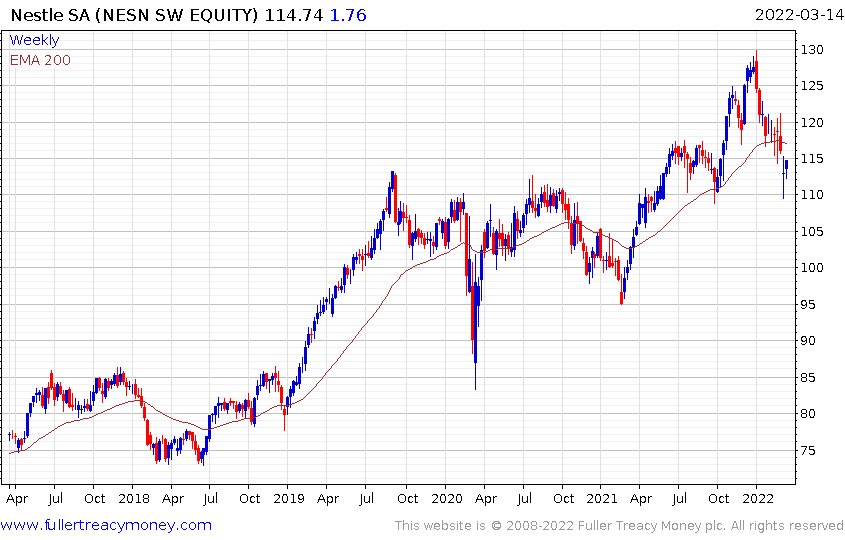

Arguably, the ESG movement found its first target in Nestle. For years activists lobbied the public to stop consuming Nestle products because of labour and business practices they found distasteful and often with good reason. Today the carbon footprint of the food sector is under scrutiny and the ESG model is part of every corporate communication.

Nestle is an S&P Europe 350 Dividend Aristocrat. The breadth and reliability of cashflows make it a defensive play and it is currently testing the upper side of its underlying range.

Nestle is an S&P Europe 350 Dividend Aristocrat. The breadth and reliability of cashflows make it a defensive play and it is currently testing the upper side of its underlying range.

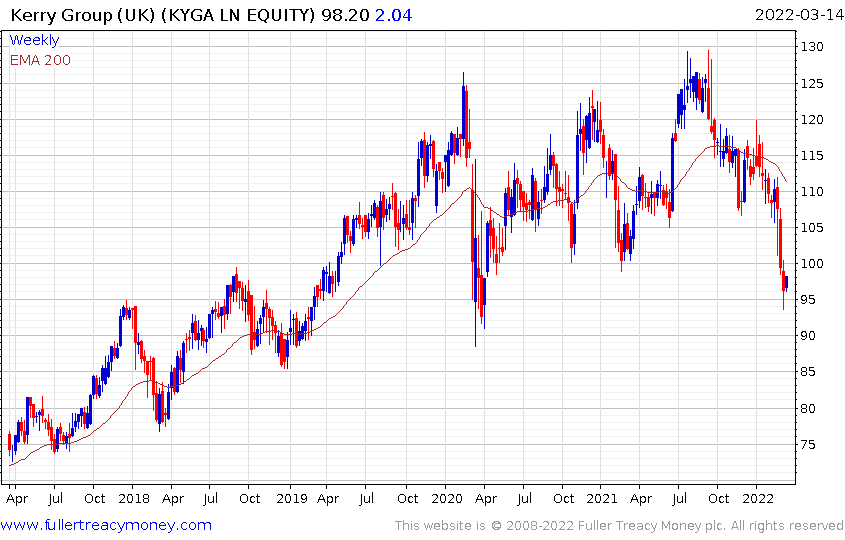

Kerry Group has not traded below the 1000-day MA since 2009. It is also a dividend aristocrat and is short-term oversold.

Kerry Group has not traded below the 1000-day MA since 2009. It is also a dividend aristocrat and is short-term oversold.