Email of the day on volatility measures

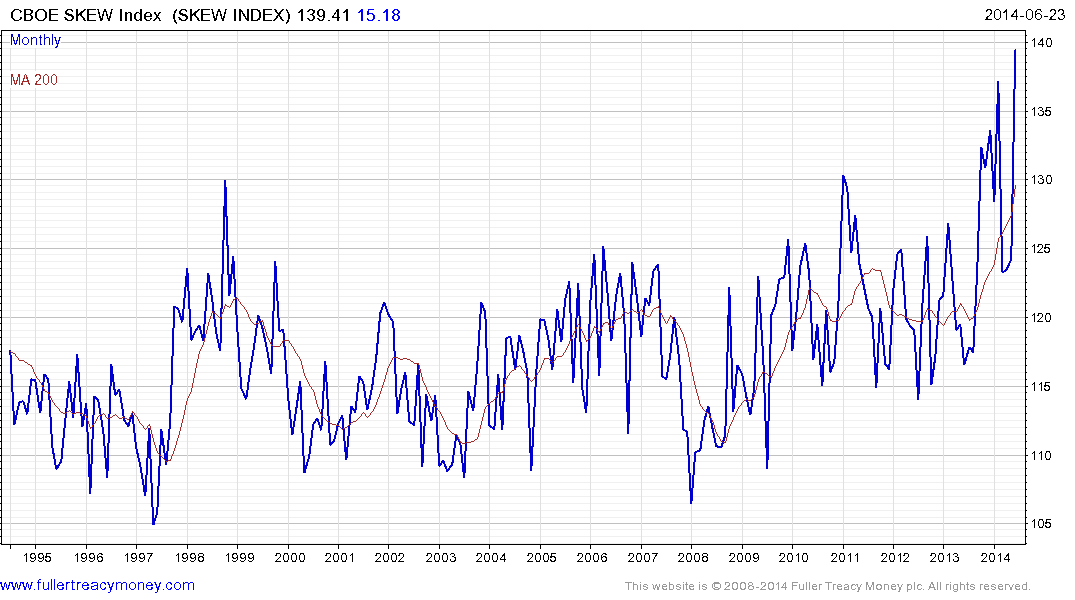

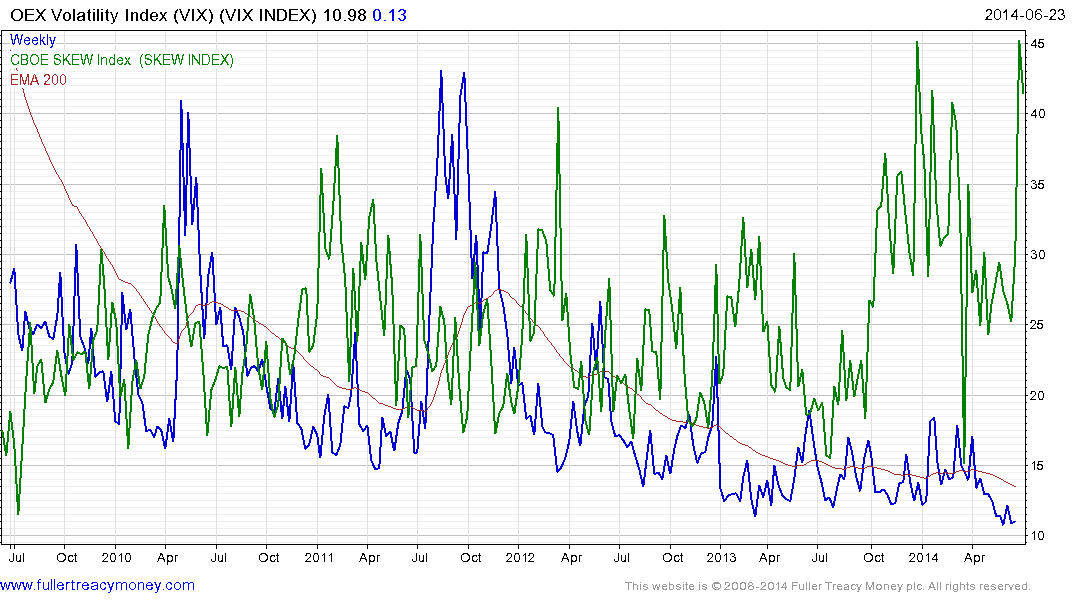

“Have you noticed how the CBOE SKEW index is exploding while the VIX stays low? This market is a bit messed up I’m afraid”

Thank you for pointing out this divergence which is worthy of consideration. You are correct that both are measures of volatility. However, the VIX measures the relationship between at-the-money options while the SKEW looks at the relationships between out-of–the-money options. In other words the VIX looks at realised volatility and the SKEW looks at expectations of volatility.

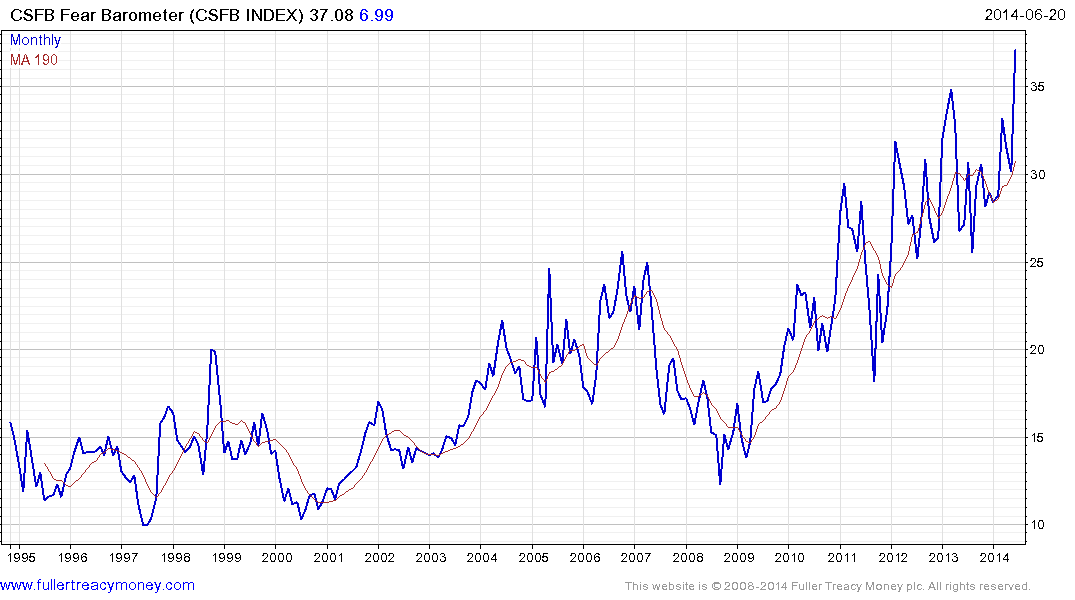

What is interesting at present is that the VIX is close to record lows following an unusually quiescent period while the SKEW is close to all-time highs. This suggests investors are betting the low volatility environment will not persist. The CSFB Fear Index is similar to the SKEW and is also at an all-time high.

These indicators are not timing tools but they confirm that institutional investors are becoming increasingly cautious as the S&P500 approaches the psychological 2000 level.

Back to top