Email of the day on Treasuries, Wall Street and Australia

I am a retired Debt Capital Markets banker. I think US Treasuries are still an attractive investment. Well at least US Treasuries pay a coupon and the USD is an attractive currency to many global investors. You are right these ridiculous low yields are not sustainable long term. However before reality reappears in global bond markets we need to see the end of the many excessively accommodative global monetary policies. You are rather bullish on equity markets. Looking at the S&P500 I think I can see why you hold that point of view. As you say the S&P 500 seems to be forming a base or consolidation. Regrettably the chart for the local ASX200 to my observation looks awful. Thank you for all your good work.

Thank you for these comments and I agree US Treasuries represent a safe haven for bond investors, when so many other sovereigns have negative yields. The big question we will likely get an answer to over the coming six months is how willing the Fed is to go-it-alone in raising rates.

With the rest of the world moving towards further monetary accommodation the upward pressure on the US Dollar from additional Fed hikes would represent a significant headwind. Meanwhile the US economy is 70% domestic consumer and wage growth has become a focus for those looking at signs for what the Fed will do next. Last week’s decline in wage demands suggest the Fed has time to monitor the situation.

Right now Treasury yields are rallying from the lower side of a developing base formation in a reversion back up towards the mean. 2% is an obvious first area of resistance and a sustained move back above that level would be required to signal more than steadying. Since bonds are priced on a relative value basis, the potential for increased investor interest as yields rise, when compared to the negative yields elsewhere, is likely to act as a brake on significant near-term additional supply dominance.

Last week’s upside weekly key on Australian 10-year yields suggests a low of at least near term significance and a reversionary rally is underway. Nevertheless, the RBA has significantly more scope to ease should it need to and a break in the medium-term progression of lower rally highs would be required to signal more than temporary supply dominance.

I think we need to have some clarity on exactly what we expect from the S&P 500. It has been considerably less volatile than many international stock markets and has returned to test the region of the psychological 2,000 level. A short-term overbought condition is evident so we can expect some consolidation before long. Over the medium-term there is a completed top formation overhead and that represents a significant source of additional supply. We can expect continued volatility. Longer-term this looks like the first big consolidation following an impressive breakout from a long-term range. How well the recent lows near 1800 hold during the next pullback will give us greater clarity on how credible the medium-term consolidation thesis is and the very least will give us a touchstone in terms of the overall trend.

In my book Crowd Money published in 2013 I laid out the case for a secular bull market on Wall Street but highlighted that normalising monetary policy represented the first challenge to its evolution. It’s been a more gradual process than I expected and it is still a long way from over, but the USA is now embarking on that journey Significant economic deterioration would be required for the Fed to embark on additional monetary easing at this stage.

The S&P/ASX has held a progression of lower rally highs for more than a year and is now testing the region of the 200-day MA following its latest reversionary rally. A sustained move above 5200 is required to signal a return to demand dominance beyond short-term steadying. Longer-term the Index does not have a consistent chart pattern which has made it very difficult to deal with. That suggests there is significant disagreement among market participants about the likely direction for the Index.

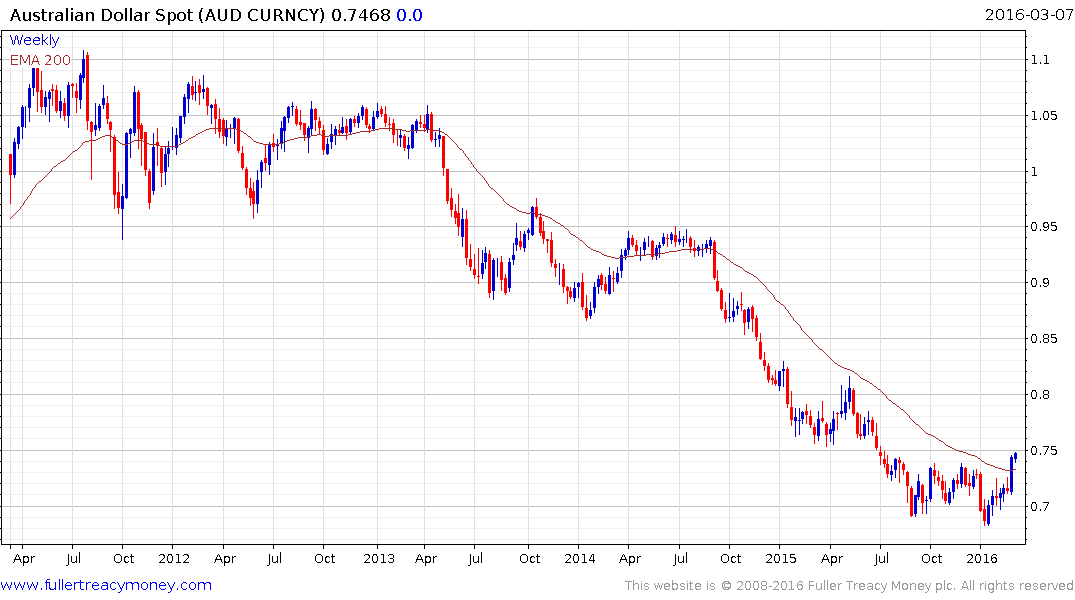

One bonus for Australia in attracting foreign investors is that the Australian Dollar rallied last week to push back above the 200-day MA for the first time since September 2014. The recent rebound in industrial and energy commodities should be good news for Australia’s embattled resources sector and a clear downward dynamic would be required to question current scope for additional Aussie Dollar strength; in line with the Continuous Commodity Index.