Email of the day on the digital economy:

Another dynamite audio last weekend - much appreciated, and thank you.

I came across this report from Huawei and Oxford Economics the other day. I'm still reading but it really ups the argument about the effect of digital technology using what it calls the spill-over effect within and across industries.

Some of the report’s key findings are:

The true size of the 2016 digital economy is US $11.5 trillion globally, or 15.5% of global GDP. This is roughly 3 times larger than traditional measurements. The base digital assets comprise 1/3 or $3.8 trillion, while digital spillover effects account for the remaining 2/3 or $7.5 trillion

The digital economy is 18.4% of GDP in advanced economies, ranging in size from 35% to 10%. The US has the largest digital economy at 35% of GDP.

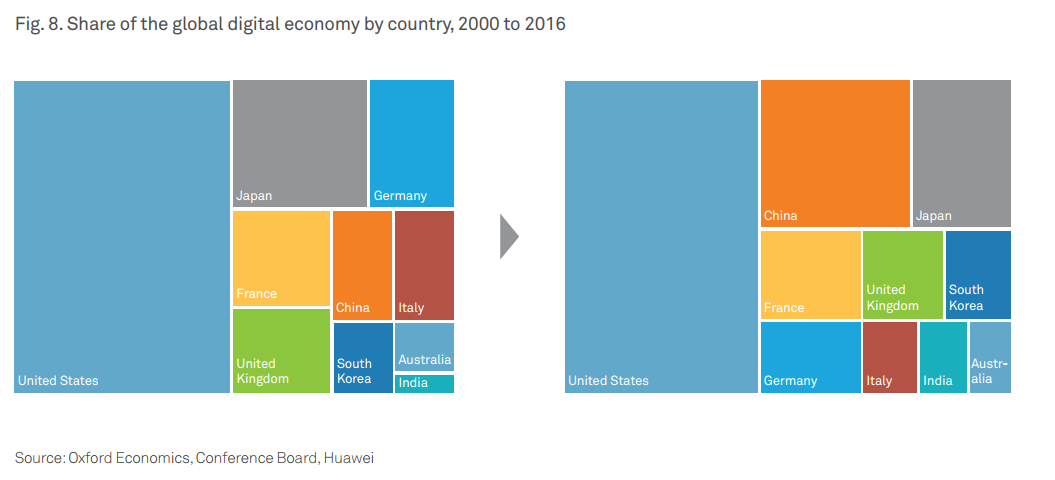

The global digital economy has almost doubled between 2000 and 2016, growing 2.5 times faster than global GDP over this period. China’s share has tripled from 4% of GDP in 2000 to 13% in 2016.

Over the past three decades, every dollar invested in digital technologies added $20 to GDP on average, 6.7 times higher than non-digital investments which added $3 for every dollar invested.

Assuming current growth rates of digital investments over the next 10 years, the report estimates that by 2025 the digital economy will be US $23 trillion globally, or 24.3% of global GDP, up from 15.5% in 2016.

If you download, I found the graph on 9.17, Fig 3 particularly interesting and unexpected.

Thank you for your kind words and I’m delighted you are enjoying the big picture long-term videos. If the viewer numbers on Vimeo are anything to go by they are the most popular feature on the site apart from the Chart Library.

This is a very welcome contribution to the debate on how much the digital economy contributes to productivity growth. Some are still arguing that the productivity gains from the internet peaked more than a decade ago and use that to explain why growth has been less than impressive since. However, as the complementary evolution of artificial intelligence, automation, cloud computing, social media, 5G connectivity and Internet of Things advance they all contribute to productivity gains when viewed from a wider digitisation theme.

These conclusions raise important questions about how GDP is measured and what is considered as contributing to growth. The Velocity of M2 has been declining steadily since 1997. Some would point out this is a reflection of excess savings resulting at least in part from the surge in monetary accommodation from central banks. However, an alternative explanation I favour is that it is a correlation with the disintermediation of the internet and the digitisation of the economy.

Here is a section from the report:

The digital spillover happens when technology accelerates knowledge transfer, business innovation, and performance improvement within a company, across supply chains and amongst industries, to achieve a sustainable development economic impact. The digital spillover is crucial to the growth of the digital economy. In partnership with Oxford Economics, we modelled the impact that technology investments have had on GDP, across a sample of around 100 countries over three decades. We found that their full impact on the economy was much greater than what might be inferred from the direct gains flowing to the investor. This extra impact is driven by the digital spillover, and it makes a considerable difference. Our analysis shows that every US $1 invested in digital technologies over the past three decades has added US $20 to GDP, on average. This is an enormous return compared to non-digital investments, which delivered an average return of around US $3 to US $1 invested.3 This result shows that for every US $1 investment the average return to GDP is 6.7 times higher for digital investments than for non-digital investments.

The indirect impact of digital investments can often outweigh the direct returns to the investor. Every investment businesses make in digital assets — such as upgrading their computer hardware, building new software solutions, strengthening their network infrastructure — is designed to boost productivity. But zooming out from these case-by-case investment decisions, the true economic impact of digitalization is much broader, more complex and far-reaching than this. Over and above the private gains to the investor, a more profound chain of indirect benefits also rolls out when businesses invest in digital technologies. There are three key channels through which it can materialize, namely internal, horizontal and vertical channels.

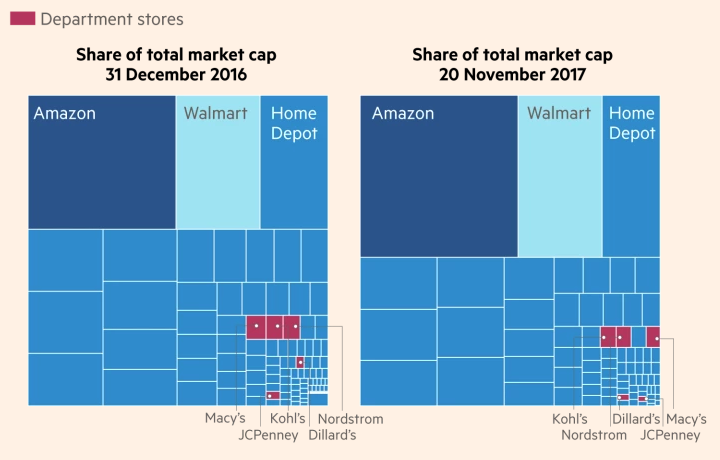

Two points that immediately grabbed my attention is that there are obviously some clear winners from the digitisation trend such as Amazon, Facebook etc. However, this article from the Wall Street Journal today highlights the fact that many retailers still have a long way to go before they are up to speed on how to manage the traffic data they collect from visitors to their sites.

The second was a remark one of the delegates at the recent London Chart Seminar made about the suspicion many German consumers still have about using credit cards and online payments. This graph of the growth of the online sector globally illustrates how quickly Germany is falling behind the rest of the world; going from #3 in 2000 to #7 in 2016.

These points both highlight how digitalisation of the global economy is contributing to an even more competitive environment where there is likely to be continued polarisation between the winners and losers. This chart from the Financial Times illustrates the jump in dominance of the three largest retailers versus everything else this year.