Email of the day on secular bull markets

I was just listening to your big picture round-up from last Friday.

You mentioned a point that I have heard a number of variations on over the last year, from Fuller Money ..... and that is that we (I think you are taking of US shares) are near the beginning of a major secular bull market (in US shares).

I think the argument you made in last Friday's big picture round-up went something along the lines of:

That US shares have had a long period (16 years) of ranging after the peak in 2000 ....... and that this is roughly the length of time that US shares ranged sideways in the period from the late 1960s until 1982 ....... when US share commenced it last major secular bull market.

Like you, I am very happy to acknowledge that I do not know the future.

BUT this is what makes me wary of your view that US share might be near the beginning of a major secular bull market:-

The Shiller cyclically adjusted P/E for US shares is above 25 .... which is an extremely high valuation. I am not aware of any example in history, where there have been good real returns for shares over the following 20 years. Shiller's research would suggest the next 20 year share returns would be more like something closer to 0%pa real.

The historically large debt bubbles in the West (but USA in particular) also warns of bad times ahead for investors. Most debt bubbles are followed by economic depression. I am aware of only 1 debt bubble where this has not occurred, namely Japan post 1989 ...... but the 19 years following 1989, delivered horrible returns for Japanese shares and property.

So you are saying I think, "This time is different". As you know, these are some of the most dangerous words for investors. For US shares to embark on a major secular bull market, would be truly unique in history - at least from what I have found in my very long-term market research.

Your thoughts please?

Thanks for this question which in my opinion is of fundamental importance for investors. As you point out, we believe major breakouts from long-term ranges are generally a signal something has changed in how supply and demand are interacting. Provided the breakout is to the upside, this can lead to a new long-term or secular bull market. The possibility of a new secular bull market on Wall Street has been a persistent topic of conversation at this service since we observed large companies with global businesses (Autonomies) breaking out of long-term bases as early as 2011. We are already four years into a secular bull market. .

As you point out debt levels are high and valuations, at least on a cyclically adjusted basis, are elevated so it is hard to argue stocks are cheap. For the trend to persist beyond the medium-term there has to be real fundamental change to support it. Technological innovation, the energy revolution, the global availability of these products and methodologies and the rise of the global middle class all combine to provide the fundamental reasoning for why a new secular bull market might be in evidence.

The big question is to what extent the breakout from long-term ranges was the result of a liquidity fuelled surge initiated by central bank monetary policy and how much of its was fundamentally driven. Opinions on this matter differ widely. We know that quantitative easing and extraordinary monetary accommodation has helped inflate asset prices so liquidity has definitely played a role in supporting stock prices.

We cannot simply ignore the fact that governments and corporations have been gorging on debt because it has been so cheap. However it is unlikely to be a problem until it needs to be refinanced. With much of it issued at five-year maturities the 2018-2021 timeframe will be a challenging period for debt roll overs if interest rates do in fact move higher from current rock bottom levels.

We should remember that the breakout from the last big range in 1981 resulted in an impressive rally but that valuations didn’t bottom until 1982 following a reversion back to the upper side of the underlying range. In this instance the S&P500 has been ranging for a year already.

The Fed is the only major central bank even considering tightening policy and even that is still an open question. Nothing has happened to question the practice of issuing debt to fund buybacks and dividend increases although the quantity of such purchases is not increasing fast enough to have the same effect.

We might have identified the makings of a new secular bull market from late 2011 and early 2012 but the market has been rallying since 2009. It’s reasonable to assume a lot of good news has already been priced and that is evident in valuations. Those measures of value are either going to moderate from here or they are going to get to bubble levels. A breakdown from the current range on the S&P500 would signal the former is more likely while a breakout would signal we are potentially entering the mania phase of what has been an already impressive seven-year advance.

Manias are not based on fundamentals. They exist because the crowd believes whole heartedly in a contradiction but has no reason to question it. We might agonise over the practice of surging debt levels, central bank money printing, the inevitable requirement to refinance. However if you are managing money and need to generate a return in a zero interest rate environment you have no choice but to move out the risk curve, get long and/or get leveraged. The longer the practice remains profitable, the larger the positions are likely to be. It’s is not until a bubble is well and truly underway that central banks feel compelled to choke off liquidity.

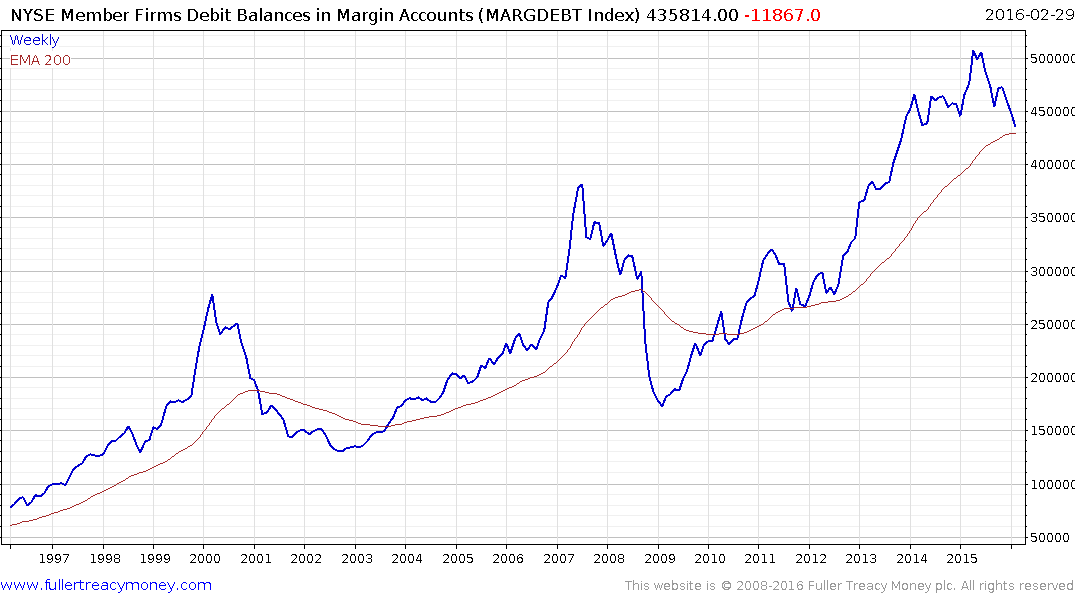

NYSE Member Firms Debit Balance in Margin Accounts is updated with a significant lag but the historically high level it is at bears out the above point.

Part of the reason there is so much focus on what the Fed is likely to do is because the decisions made over the coming months are likely to have an outsized impact on financial markets and stocks in particular. This article from Bloomberg includes some relevant points that may also be of interest.

Meanwhile today’s rally on the S&P500 represents a change with the stock market rallying on positive news about the economy and housing.

The Banks index has held a progression of higher reaction lows since January and pushed back above the 200-day MA again today.

Oil prices also continue to exert a positive influence on large cap energy companies.