Email of the day on potential for a revival of the Eurozone debt crisis

I wonder what you make of this article in today’s Financial Times.

It concludes: “With growth weakening once more it is time to dust off the old euro crisis playbook: short the euro, short the periphery, long Germany.”

Well I have been long a few German shares and short Euro (via Spread Bet) for some weeks and have made good profits, which is fine in a personal sense though sad if Europe really is heading back into serious problems. What is your view on what the key charts are telling us, the financials, the banks, sovereign bond yields, country stock market indices etc.

Thank you for this question which appears to be the topic of the moment in various financial blogs. For example another subscriber sent through a link to this post making a somewhat different argument but reaching a similar conclusion.

The prospect of relations with Russia being strained for the foreseeable future represents a headwind for the Eurozone which already faces a well-known series of challenges to growth. Winnowing companies that are exposed to Russia from the wider market was swift and resulted in stock markets, not least Germany, pulling back sharply and bonds, particularly Bunds, rallying to records.

To my eye at least, this situation is different to the Eurozone’s sovereign and banking crisis because we have clear communication from the ECB that they will do whatever is necessary to preserve the currency union. Nevertheless, the Eurozone needs a weak currency more than the US right now. The Euro’s uptrend since 2012 has been broken and while potential for a short-term bounce has increased, a sustained move above $1.35 would be required to question scope for a further test of underlying trading.

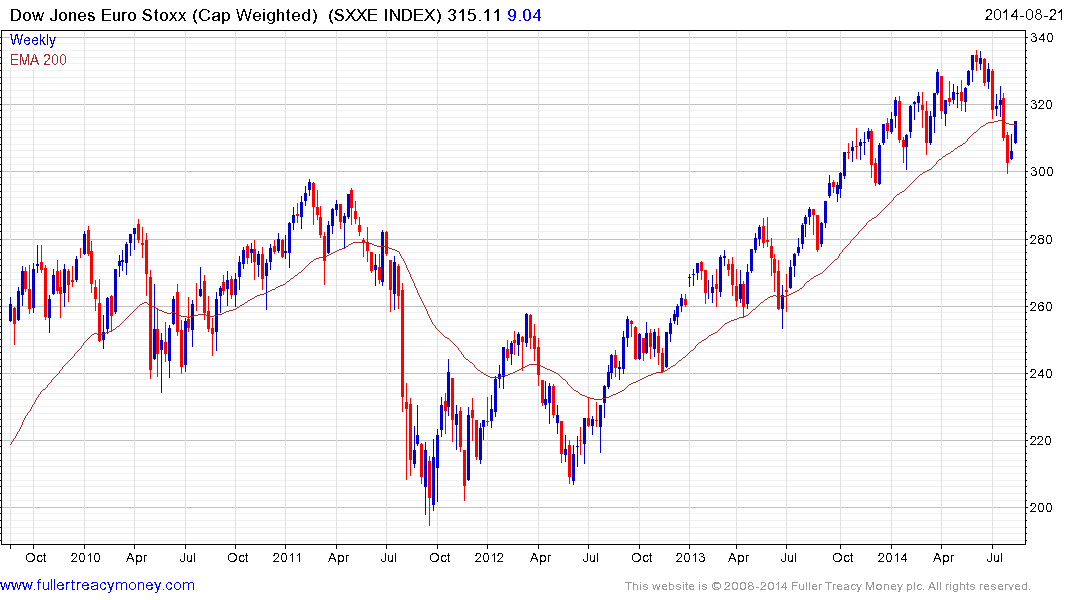

The Euro STOXX Index experienced its largest reaction since 2012 and has bounced over the last two weeks to test the lower side of the overhead range and the region of the 200-day MA. At this stage it is worth watching because it will either find support above the August lows, lending the Index a greater chance of resuming the overall uptrend, or it will fail at this level and extend the decline, which would increase the potential that the Eurozone economy is headed for a significant contraction. In the absence of evidence to the contrary I’d be inclined to the give the bulls the benefit of the doubt, not least because sentiment is so negative.

The Euro STOXX Banks Index fell less than the wider market and has subsequently rallied more.

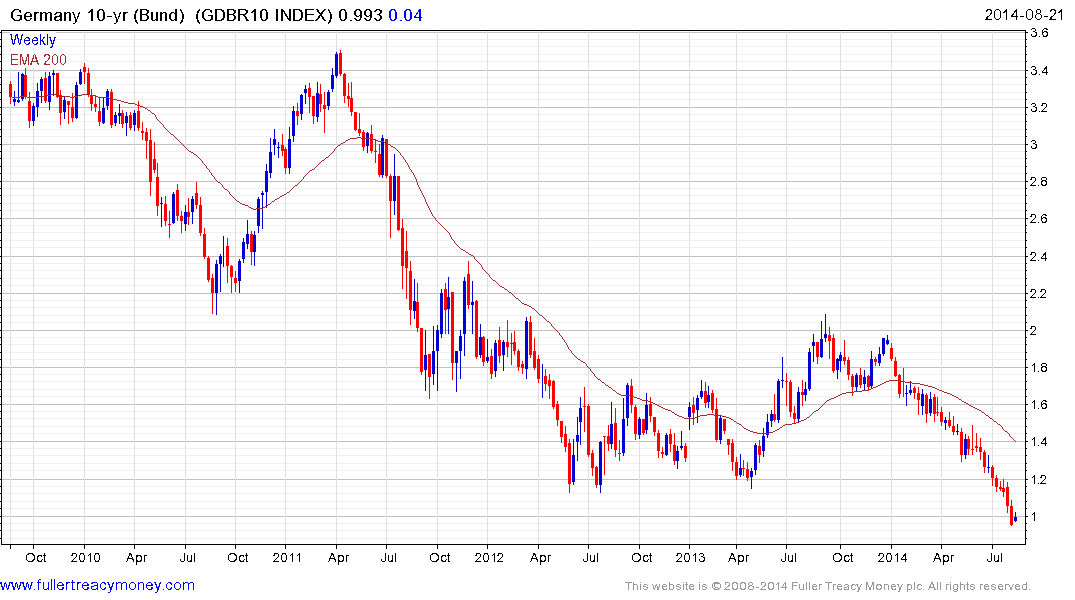

German Bund yields have been trending lower all year and hit a new all-time low last week. One conclusion is that this reflects rising deflationary pressures. Another interpretation is that the ECB’s backstop of the bond markets makes speculation risk free. There are certainly deflationary fears but the contraction of sovereign spreads, particularly along the periphery, is more a sign of faith in the ECB’s pledge to support the market than deflationary fears. If the stock markets continue to rally, there will be less need to hold an overweight in sovereign bonds.

The imposition of sanctions on Russia exposed the challenges facing the Eurozone as it struggles to reignite growth without a concerted strategy and introduced a risk premium in the form of geopolitics that had not previously existed. An escalation of the Ukraine/Russia crisis, which has been easing of late, would represent an additional source of uncertainty so the outlook for the region remains far from clear. Nevertheless, easy monetary policy suggests that traders will support the continued rally until they have a reason to reverse positions. The Fed’s monetary policy is likely to remain the single biggest factor in the absence of an additional deterioration in the geopolitical situation.

Back to top