Email of the day on bonds versus equities

Having read John Authers FT.com column today, I confess to a bit of confusion. Listening to your outstanding audios over past weeks and months (for which, many, many thanks), I had formed the impression that when the bond markets turns, it would be good for equities on the basis that money has to go somewhere, and it would flow in a large part to equities. Authers seems to be saying the opposite - see his last 3 paras today:

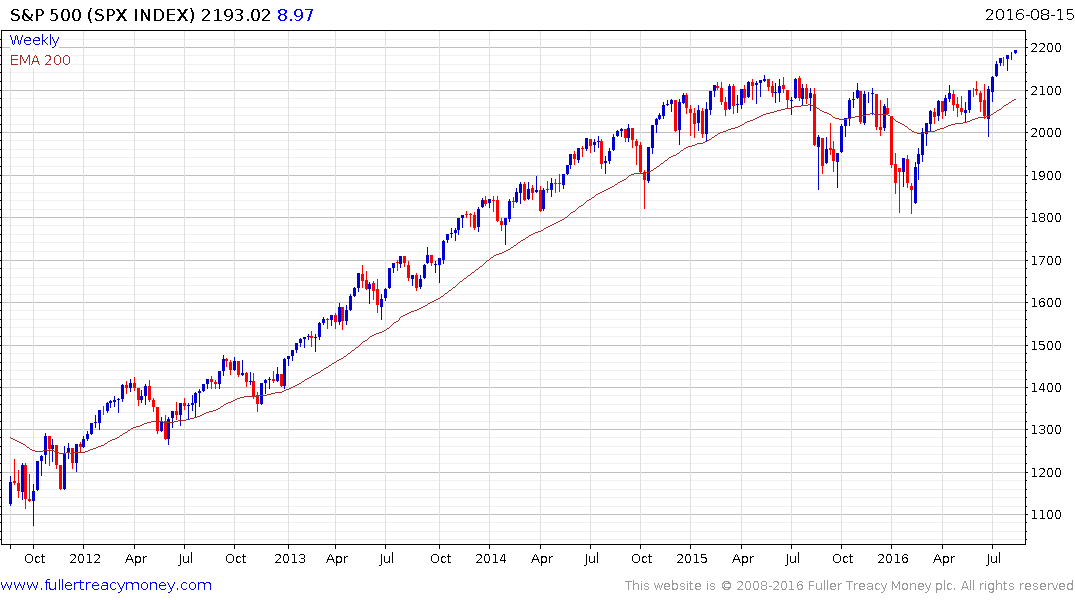

"Look at the chart of the S&P and this looks like a peak, and a bad time to buy. Look at the chart of how stocks have performed relative to bonds, and it looks like stocks should be ready to shine. This illustrates the paradox that has also lasted for years that stocks look expensive by almost any sensible historical measure — except when compared to bonds, when they look cheap.

But there is a nasty problem with this. If bonds finally go into reverse, rates will rise, the support for stocks will be removed and the risk is more that stocks will start to fall. The bond market rally is extraordinary, it has gone on for a long time, defeating predictions by many (myself included) that yields had become unsustainable. US Treasury yields have been falling steadily for more than three decades.

If bonds can somehow continue this, then stocks will probably continue to prosper (although they may fail to outstrip bonds). If bonds go into reverse, it would be bad news for both stocks and bonds. And either way, the record in the S&P 500, which has created genuine wealth for those who hold it, is a sideshow besides what is happening in bond markets."

Can you comment please and perhaps remove my confusion?

Thanks as always

Thank you for this topical email and snippet from John Authers’ article. Here is a pdf of the full article.

If you had asked me a couple of years ago, before just about every central bank in the world was engaged in quantitative easing, I would have said that a peak in the bond market would have helped act as fuel for an additional rally in equities. However I’m not so sure now.

We have long described the rally since 2009 as liquidity fuelled and I have made the same point as Authers in recent audios that the primary rationale for justifying buying stocks at today’s valuations is because of the potential for yield compression due to the fact so many bonds have negative yields.

If we are indeed entering the third psychological perception stage of the bull market evident since 2009, as I contend, then we would expect to see increasing acceptance of the rationale for owning shares regardless of the objective fact they are expensive on an increasing number of fundamental metrics. If the rally is being driven by contracting spreads then a hike in bond yields would disrupt the momentum and result in a pullback in stocks.

A jump in bond yields could also have the additional effect of hindering the ability of companies to roll over and source new debt at attractive rates. That could have a knock-on effect for buybacks which have been a significant influence on the bull market to date.

The flip side to these arguments is that it will, in large part, depend on what the catalyst for higher bond yields eventually is. If it is because inflation is spiking higher, potentially in response to helicopter money, that should be good for equities as a potent hedge. If on the other hand bond yields are spiking because of a widespread lack of faith in the currency they are denominated in, that is likely to affect equities in absolute but not nominal terms. Alternatively if a benign scenario results in bond yields recovering because economic growth picks up, after what has already been a long hiatus, then the leverage question means equities could have a mixed performance as higher debt servicing costs are counterbalanced by better medium-term growth prospects.

In the meantime, leverage and liquidity remain the hallmarks of this bull market and the potential for fiscal stimulus is an additional bullish characteristic. Manias are characterised by irrationality and it is more important than ever to monitor trends not least because momentum moves are most dangerous when they lose consistency.

Back to top