Email of the day

“Saturday's audio was masterful and a wake-up call for those short of equities. Few are calling it (though I attach Odey's piece on Europe). 10-12 year bases are important technical underpinnings for a new bull market in equities and has allowed a PER de-rating to be compensated by earnings increases. I show a few autonomies (or global high yielders) that you can buy at more or less the same price as 2000 (taking a holiday from probity in some cases). These are mostly stocks we hold for clients, but not all, and I could have added a plethora of telecoms and oil companies. Technicians might be tempted to sell the Making-New-High autonomies like Nestlé, Diageo, Unilever and Pepsi to buy laggards. I am not so sure it is so simple as our low growth, develeraging world will value consistency of growth. The 1960s Nifty Fifty lasted well over a decade.

“I wonder if Heineken (2% yield, 12x PER'12, forced to pay up for Asia Pac Brew, one of our GTI stocks) is not now a strong buy as it focuses more on emerging markets, somewhat belatedly….we are checking this out and if the family holding co is the better way in. (UBS IB say “Heineken is the third largest global brewer behind ABInbev and SABMiller. Heineken has a large exposure to Western Europe (36% EBIT) and Eastern Europe (12%). Post the FEMSA acquisition in January 2010, Mexico accounts for 12% of group EBIT. Its second largest emerging market is Nigeria. Overall Heineken has 40% EM exposure directly or through its JVs (CCU/APB). The Heineken brand accounts for 20% of group volumes. Heineken's major shareholder is the quoted entity, Heineken Holding, which owns 50.05%. This, in turn, is 51.083% controlled by the Heineken family. FEMSA has 20% economic interest in Heineken”.)

Eoin Treacy's view Thank you for your generous comments and educational email. The majority of stock market activity is short-term oriented and is becoming even more focused on the minutiae as high frequency traders become ever more influential. However this “noise” masks the long-term profit potential of a thematic approach to investing.

A considerable number of globally oriented shares have been in a process of valuation contraction over the last decade which has been characterised by mostly ranging markets and rising earnings. Those with solid records of increasing their dividends are now being rewarded by investors. While money flow data continues to suggest that interest in the sovereign bond markets remains robust, the long-term potential for that market is easily outstripped by the upside potential for shares with solid balance sheets and leverage to the growth of the global consumer.

As one clicks through the constituents of the Autonomies sector, a considerable number of consumer shares have moved into a process of mean reversion. Industrial shares have for the most part rallied strongly from their June lows and moved to positions of outperformance. Rotation from one sector to another is to be expected from time to time but the broader picture is of a group of companies that continue to benefit from the increasing demands of a new disposable income class. While there is scope for some occasional trimming around the edges, the broad scope of this theme means it is likely to provide a recipe for success for upwards of a decade.

Following your example I have chosen to post 20-year weekly charts below.

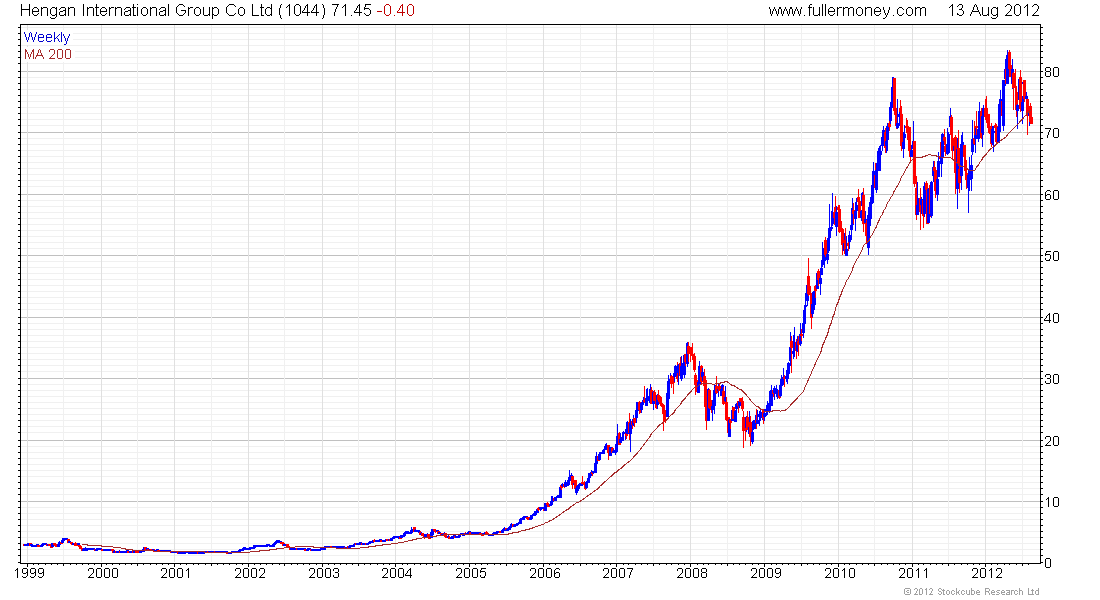

Apple, Microsoft, IBM, Qualcomm, Samsung Electronics, Intel, Yum Brands, Kraft, Hengan International, Linde AG, Mastercard and Praxair all found support in the region of their respective 200-day MAs over the last few weeks and sustained moves below these lows would be required to question medium-term scope for additional upside.

Google, Johnson & Johnson, Eli Lilly, GlaxoSmithKline, PepsiCo, Heinz, Procter & Gamble, Uni-Charm, Reckitt Benckiser, Heineken, General Electric, Emerson Electric, ExxonMobil and Royal Dutch Shell are currently testing the upper side of their respective ranges and clear downward dynamics would be required to check potential for additional upside.

LVMH, Compagnie Financiere Richemont, Christian Dior, Air Liquide and Praxair have all posted new highs in the last week to reassert their medium-term uptrends. Clear downward dynamics would be required to question potential for additional upside.

Novo Nordisk, Fresenius Medical, Sanofi, Biogen, Merck, Pfizer, Anheuser Busch InBev, Diageo, SAB Miller, Remy Cointreau, Pernod Ricard, Coca Cola, Nestle, Unilever, Colgate Palmolive, Kimberly Clark, Wal-Mart, Intertek Group and Visa have all become temporarily overextended relative to their 200-day MAs and are susceptible to mean reversion.

Cisco Systems, Lam Research, Microchip Technology, Tesco, BHP Billiton, Rio Tinto and Siemens have all found support in the region of the lower side of their respective ranges and are rebounding strongly.

Nike, McDonalds, Starbucks, Mean Johnson Nutrition, Herbalife, NuSkin Enterprises and Bristol Myer Squibb have sustained moves below their respective 200-day MAs and will need to sustain moves back above them to begin to repair technical damage and investor confidence. Estee Lauder has found support in the region of $50 and pushed back above the MA last week. A sustained move below $50 would now be required to question medium-term potential for continued higher to lateral ranging.

HTC is becoming increasingly oversold and the first clear upward dynamic is likely to signal the onset of short covering.

{kind=link}