Echoes of 1999: The Tech Bubble and the "Asian Flu"

This article by rob Arnott for Research Affiliates may be of interest to subscribers. Here is a section:

In the first quarter of 2016, each of the four trends reversed. Recent weeks have brought rebounds in inflation hedges, emerging market currencies, diversifying markets, and global value stocks relative to growth. Do these last few weeks represent “the turn”? Perhaps. The question, however, is irrelevant because the answer is simply impossible to know. But what we do know is that if we want peak exposure to these markets when the turn comes, we must begin to “average in” in the face of adversity.

We also know that these out-of-favor markets average a 3.0% yield premium versus a U.S.-centric 60/40 portfolio, which represents a powerful performance advantage to those who can patiently wait for mean reversion’s inevitable grip on the market. Once the market turns, history has shown the upswing will be fast and vigorous.

Real Potential

In the 5 and 10 years following December 1998, assets other than U.S. and developed-market equities and U.S. notes and bonds outperformed 60/40 by an annualized 8.8% and 6.2%, respectively. Developed value stocks also outperformed their growth counterparts by nearly 6% a year in the 5 years following December 1998. Are these markets poised to repeat this strong outperformance? Only time will tell, but we believe the potential is very real. Our view today is that real return–diversifying asset classes5 could improve on a traditional 60/40 allocation by approximately 3.5% a year over the next 10 years. Real return–oriented diversifiers and value strategies may not experience the same magnitude of outperformance as they did starting in 1999, but we’re confident they will outperform in the years to come. Now is the time to rotate into these markets.

The MSCI Emerging Markets Index is market cap weighted so it is heavily influenced by what happens to Chinese, South Korean, Taiwanese, Indian and South African shares. These five countries account for 67.25% of the Index. It’s an awfully big world out there and the emerging market universe is much more diverse than these five countries which raises the question of how good a barometer it is.

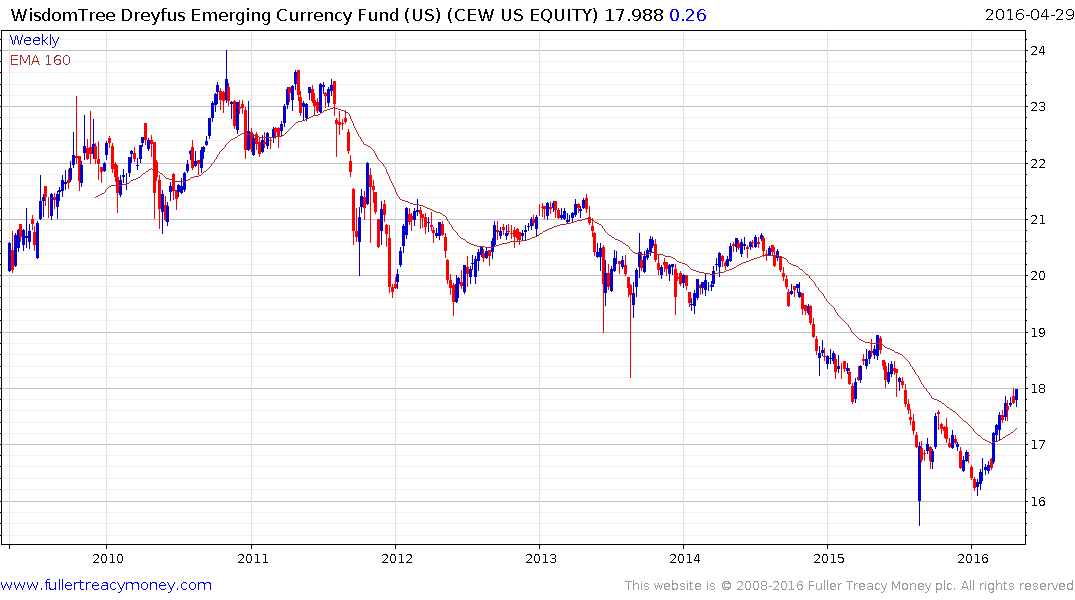

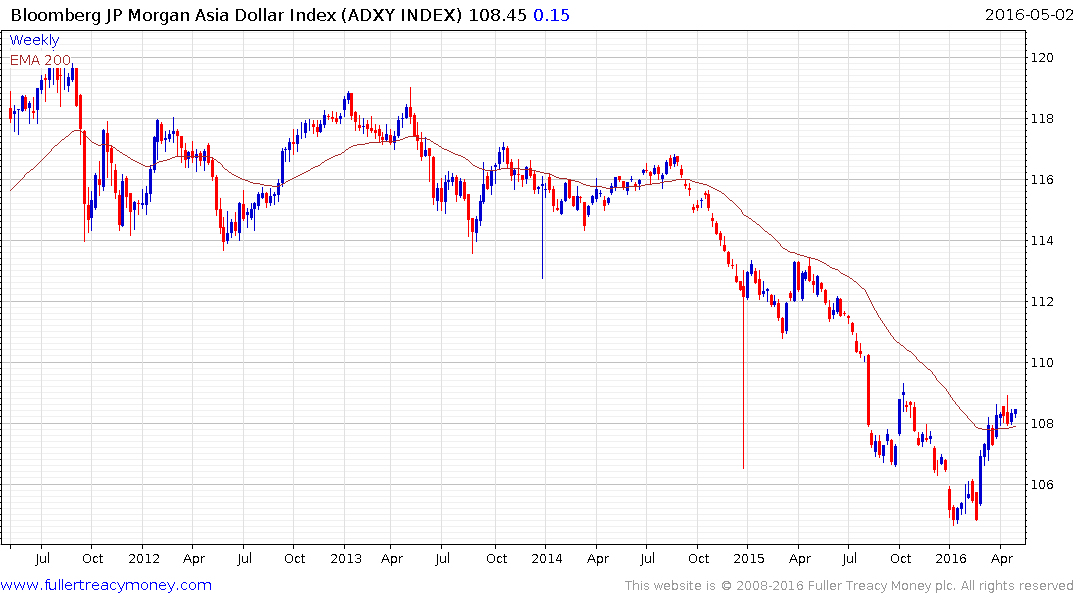

What is interesting is that if we contrast the performance of the MSCI Emerging Markets Index, the WisdomTree Emerging Market Currencies ETF and the Asia Dollar Index we observe a high degree of commonality. This is despite the fact that the currency fund is considerably more diversified. It points to the fact that selling pressure in emerging markets has been rather indiscriminate and was largely fuelled by investors taking broad spectrum decisions influenced by currency concerns rather than treating countries on their individual merits.

The MSCI Emerging Markets Index held a progression of lower rally highs from its 2011 peak and accelerated lower in the second half of 2015. It has rallied over the last couple of months to break that downtrend and a sustained move below the trend mean would now be required to question medium-term scope for additional upside.

As we can see from the above currency fund, many emerging currencies trended lower for nearly five years. That is a reflection of the difficulties many economies experienced as commodity prices declined and the effect tapering of quantitative easing had on leveraged bets the Dollar would trend lower indefinitely. However the competitiveness that many countries lost when their respective currencies were strong and domestic inflation was high has been regaining at least to an extent by the decline of their currencies since 2011. That will be a major factor in helping to revive manufacturing and exports which should translate into additional interest from foreign investors provided the various currencies hold their lows.

This article highlighting an interview with Mark Mobius on Bloomberg may also be of interest.

Back to top