Copper, lead, zinc prices to stay on the boil

This article by Frik Els for Mining.com may be of interest to subscribers. Here is a section:

Industrial metals prices are projected to jump 16% this year due to strong demand, especially from China, and supply constraints, including mine disruptions in Chile, Indonesia and Peru, the World Bank says in its commodities markets outlook published on Wednesday.

Researchers at the institution believe zinc has the brightest prospects this year and will follow up 2016's 60% price gain with a 32% jump this year.

Lead, often a byproduct of zinc mines, will also build on last year's gains and is expected to add 18% in value due to mine supply constraints brought on by permanent closures due to resource exhaustion, as well as discretionary closures and downscaling in Canada, Peru and Australia top zinc miner and trader Glencore.

[Lead] demand remains strong for the battery and industrial sectors, including increasing demand for “stop/start” vehicles, which use batteries containing 25 percent more lead than conventional units. However, lead demand faces threats from a maturing electric bike sector in China and alternate battery technologies (e.g., lithium).

The authors of the report also warn however that zinc-lead fundamentals may change longer term as higher prices "prompt greater supply in China, and Glencore’s idled capacity eventually restarts."

The industrial metals represent a clear bright spot within a commodity complex that is under pressure from excess supply, not least in the food sector. The mining sector on the other hand has been through a painful process of rationalisation where expansion has been cancelled and uneconomic supply shuttered. Generally speaking it takes time for higher prices to justify the expense of reopening mines so the potential for a further recovery remains intact.

Aluminium trended lower between 2011 and early 2016 when a recovery rally began. It continues to hold a progression of higher reaction lows and a sustained move below $1900 would be required to suggest a reversion towards the mean.

Copper has been forming first step above its Type-2 base since late last year and bounced this week from the region of the trend mean. A sustained move below $2.50 would be required question potential for additional upside.

.png)

Zinc broke successfully above the psychological $2500 level for the first time since 2008 late last year and has been forming a first step above that almost decade long base since.

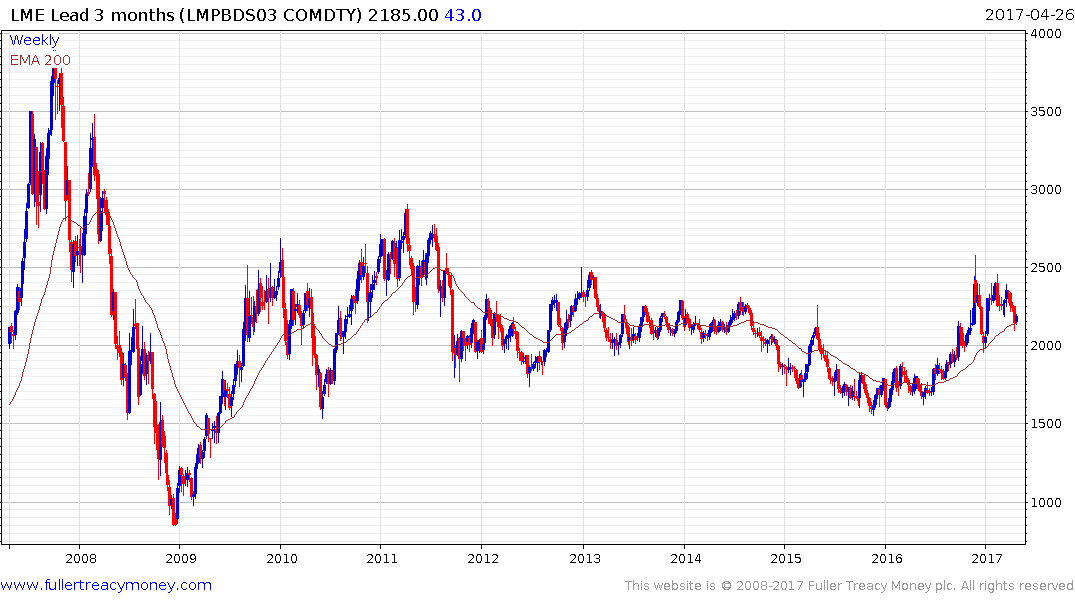

Lead has been consolidating below $2500 since late last year and has firmed from the region of the trend mean this week to hold the medium-term progression of higher reaction lows.

Tin has been ranging in the region of $20,000 since late last year and a sustained move below trend mean would be required to question potential for a successful upward break.

Nickel remains an outlier. The price has struggled to surmount the $10,000 level and broke to new reaction lows this week. A clear upward dynamic will be required to check the slide.