China's Commodities Imports Surge as Coal Hits All-Time High

This article may be of interest. Here is a section:

“With inventories relatively low, the prospects of further stimulus measures triggered restocking across commodities, which should keep demand strong in the short term,” ANZ Group Holdings Ltd. said in a note after Chinese customs released its latest trade figures on Thursday.

Still, the country’s recovery from the pandemic has fallen well short of expectations and confidence among households and businesses is fragile. Deflationary pressures in the economy and a weaker currency have added to the headwinds faced by importers, although fears that the yuan will slide further may have motivated some to front-load purchases.

A jump in Chinese demand for industrial commodities would normally be cause for celebration among miners. China’s demand growth has been one of the primary reasons investors have been willing to give credence to the view that a new secular bull market in commodities is unfolding. The problem is the narrative does not match up with the price action.

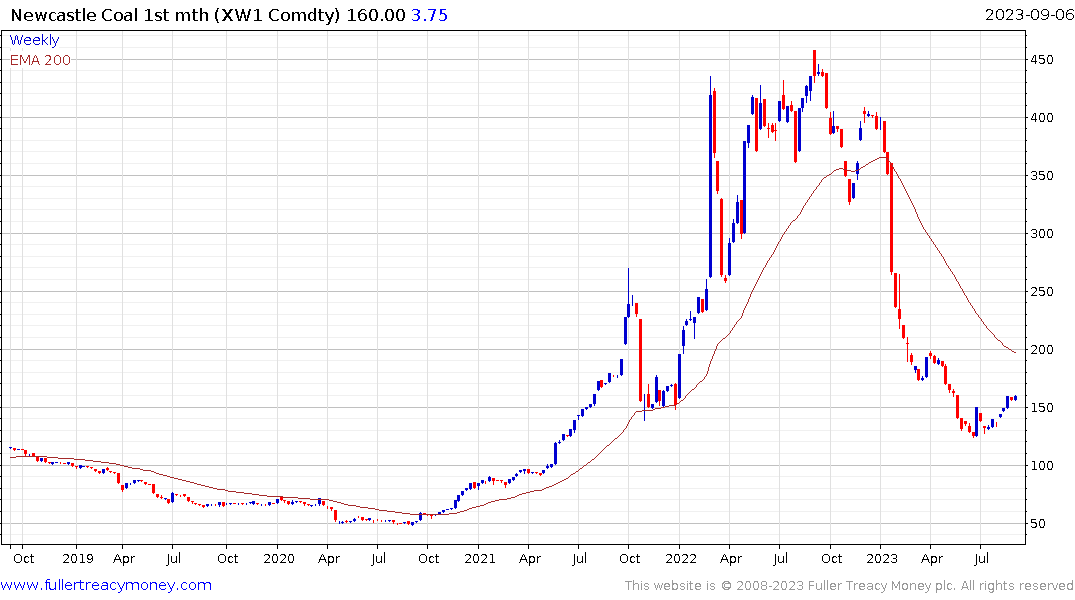

It is quite likely the recent jump in demand is a hedge against further Renminbi weakness. Coal futures surged in 2021 and 2022 and have since completely unwound the move. The price is now steadying at the upper side of the base formation but a potentially lengthy period of ranging is likely following such a large decline.

It is quite likely the recent jump in demand is a hedge against further Renminbi weakness. Coal futures surged in 2021 and 2022 and have since completely unwound the move. The price is now steadying at the upper side of the base formation but a potentially lengthy period of ranging is likely following such a large decline.

Australia’s Whitehaven coal is on the cusp of extending its downtrend as it pulls back from the region of the 200-day MA.

Australia’s Whitehaven coal is on the cusp of extending its downtrend as it pulls back from the region of the 200-day MA.

BHP Group is also pulling back from the region of the 200-day MA. If China’s demand growth were credible, it would be reasonable to expect better performance from the world’s largest miners.

BHP Group is also pulling back from the region of the 200-day MA. If China’s demand growth were credible, it would be reasonable to expect better performance from the world’s largest miners.

Copper prices are barely steady in the region of the 1000-day MA.

None of these charts suggest regional infrastructure projects are about to lift global demand. A more important question is whether China’s appetite for railways is akin to Japan’s bridges to nowhere?

In order to have a secular bull market one needs a truly impactful new demand story. To drive prices higher supply inelasticity is necessary. If demand is instead transferred from China to new energy infrastructure that is not enough to drive a major bull market. For prices to remain steady, the handover would have to be seamless. The bear case for commodities is China’s demand flatlines or declines and the green revolution does not take place.

Back to top