Australia Materials - The Big Golden Book

Thanks to a subscriber for this report from Morgan Stanley which may be of interest. Here is a section:

The 6th Edition of our Big Golden Book, covering a suite of 25 ASX listed gold producers and developers, with 7 stocks under MS coverage (AQG, EVN, MML, NCM, PRU, RRL, RSG) and broad detail on another 18 mid small cap gold miners, provides a sector snapshot in which to identify relative strengths and weaknesses amongst the ASX gold space. Our 6th Edition arrives at a time of relatively buoyant AUD gold price - a key beneficiary of the weakened Aussie dollar.

Australian gold miners are up ~15% YTD, as represented by the S&P ASX All Ords Gold Index, significantly outperforming US$ spot gold (down ~9% YTD), the ASX 300 Resources Index (-26% YTD), the ASX Small Resources Index (-20% YTD) and the ASX All Ordinaries (-2% YTD). Currency has been a key driver, pushing AUD Spot gold ~2% higher against the backdrop of a falling USD gold price (down ~9% YTD).

Here is a link to the full report.

At The Chart Seminar in Sydney in 2010 a delegate asked what all the fuss was about in the gold market because prices had not moved for more than a year when redenominated to Australian Dollars. I was reminded of that today because prices today are no different from where they were in 2010 and are about 23% of the 2011 peak which represents significant outperformance relative to the US Dollar quoted price.

As the above report highlights, Australian gold miners have benefitted from the relative weakness of the currency. This also speaks to the broader point that gold is a monetary metal and tends to hold its value better than fiat alternatives in a depreciating currency environment. As a result it outperformed spectacularly while the US Dollar was in a decade long downtrend and is likely to remain a relatively sound store of value for other countries when their respective currencies fall.

Among Australian gold miners there are a number with estimated P/Es in the low single digits and there are a number with promising chart patterns but those with have attractive valuations and chart patterns which also pay a dividend are quite rare.

For example Newcrest (Est P/E 21.98) had to cancel its dividend in 2013 and has underperformed as a result. The share bounced today from the region of this year’s lows this week.

Ramelius Resources is a small cap with a market cap in the region of A$100 million. It has an estimated P/E of 3.52 and may be in the process of completing a first step above its base.

Companies that have all three attractive characteristics include:

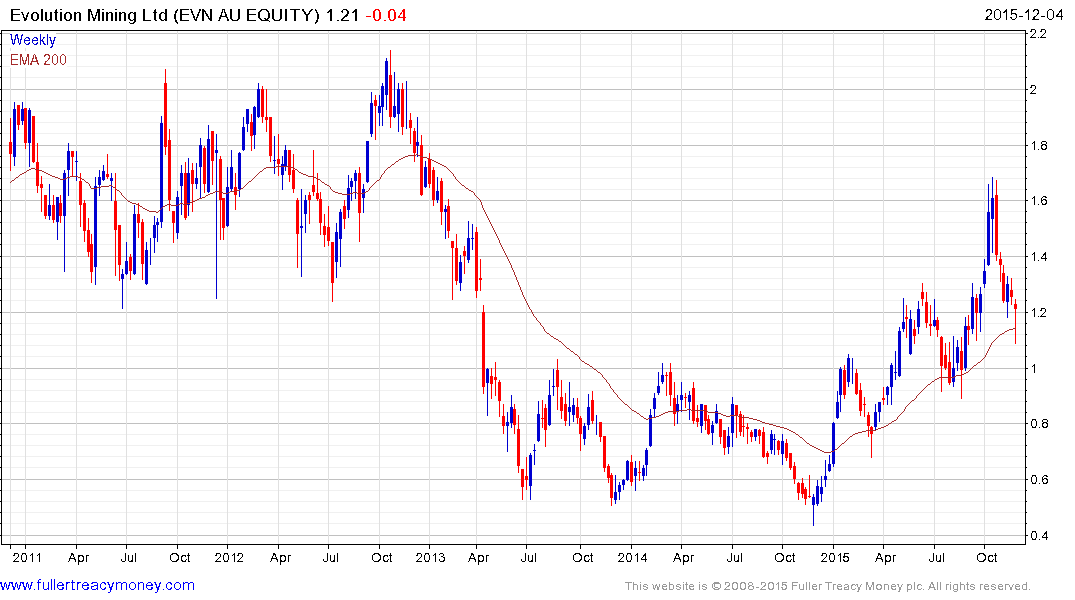

Evolution Mining (Est P/E 6.3, DY 1.60%) is bouncing from the region of the 200-day MA.

Regis Resources (Est P/E 11.67, DY 4.37%) has been testing the upper side of an 18-month base and found support this week in the region of the 200-day MA.

Back to top