Secular Bull Market Investment Candidates Review

On November 24th I posted a review of candidates I believe likely to prosper in the emerging post-pandemic market. It was well received by subscribers so I will post an update on my views on the first Friday of the month going forward. That way subscribers can have an expectation that long-term themes will be covered in a systematic manner and will have a point of reference to look back on.

Media hysteria about the 2nd or 3rd waves has not led to new highs in the number of deaths. The success of biotech companies in deploying vaccines means there is going to be a substantial recovery in the economic activity in 2021 and going forward.

The stay-at-home champions saw their sales growth surge in 2020. It will be impossible to sustain that growth rate in 2021. That’s particularly true for mega-caps. One-way bets on the sector are likely to work less well in the FAANGs going forward.

How is Apple going to double from here? If it continues higher it will be on the back of valuation expansion. That can’t be ruled out but the pace of the advance is still likely to moderate. It seems to me there will be better opportunities. Those will be likely be outside of mega-caps but also around the world.

Base formation completion is one of the most attractive of all chart patterns. When a market goes sideways for years or even decades, it is easy to forget about it. There is always a bull market in something and whatever that is tends to attract a great deal of interest. Asset classes that underperform tend to fall by the wayside as investors move on. At present a large number of international indices are breaking out of long-term ranges.

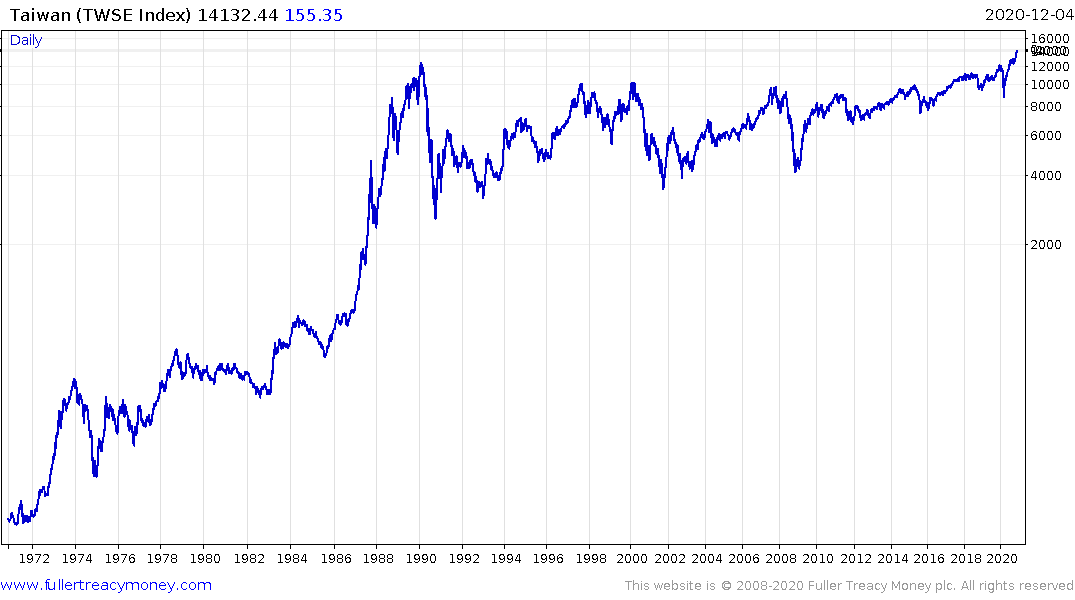

Taiwan has just broken out to new all-time highs after a thirty-year hiatus.

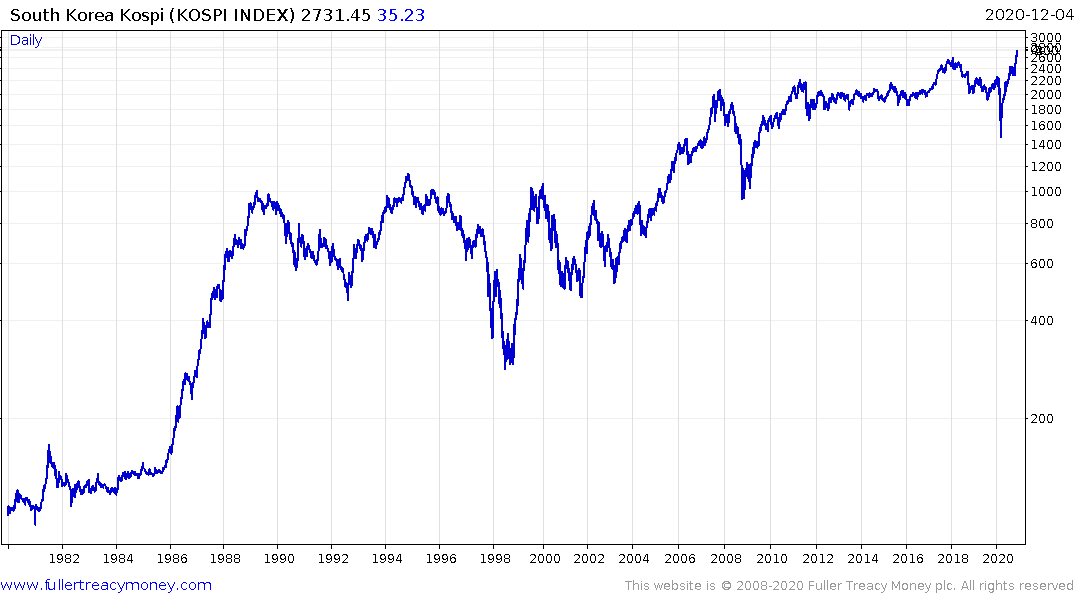

South Korea has broken out to new all-time highs after a 12-year choppy range.

The MSCI Emerging Markets Index is testing the upper side of a 12-year range.

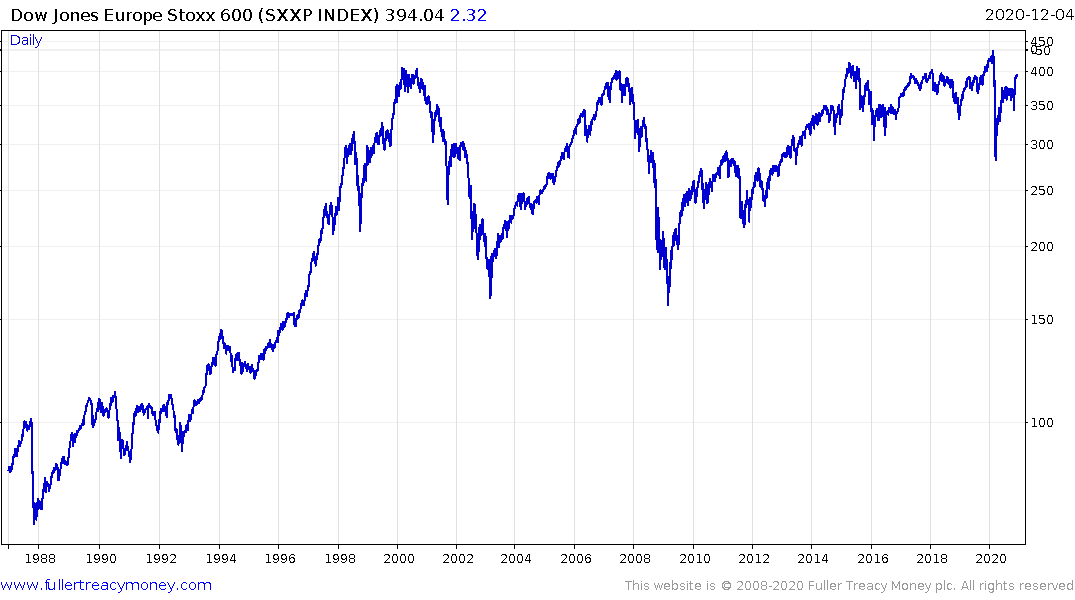

The Europe STOXX 600 is approaching the upper side of a twenty-year range.

The FTSE-100 is recovering back towards the upper side of its 20-year range.

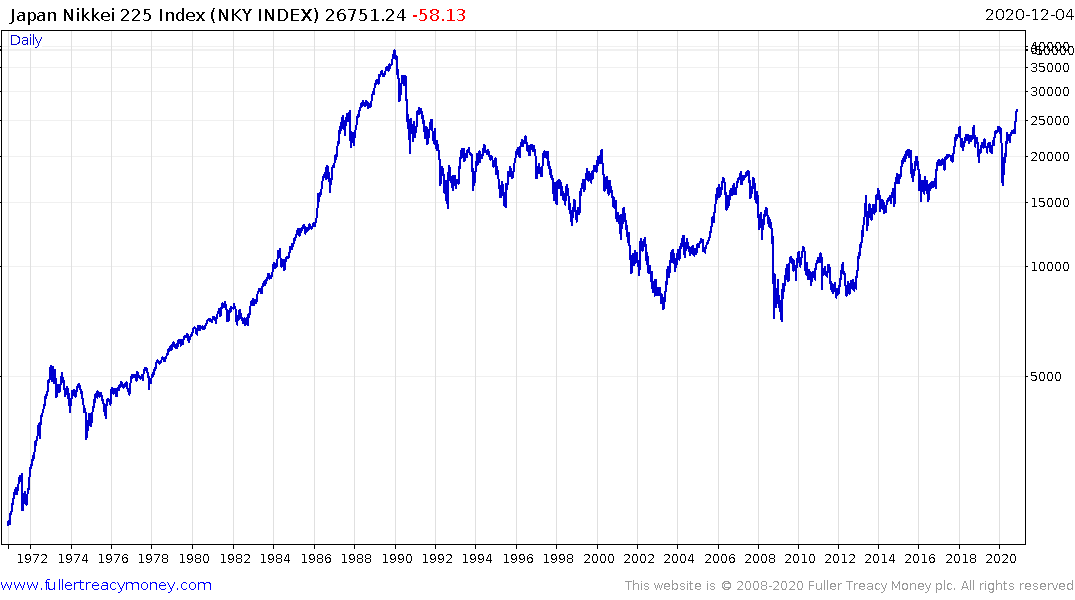

Japan’s Nikkei-225 has completed a first step above its long-term base formation.

.png)

If we rebased the Nikkei-225 to US Dollars it is on the cusp of hitting a new all-time high.

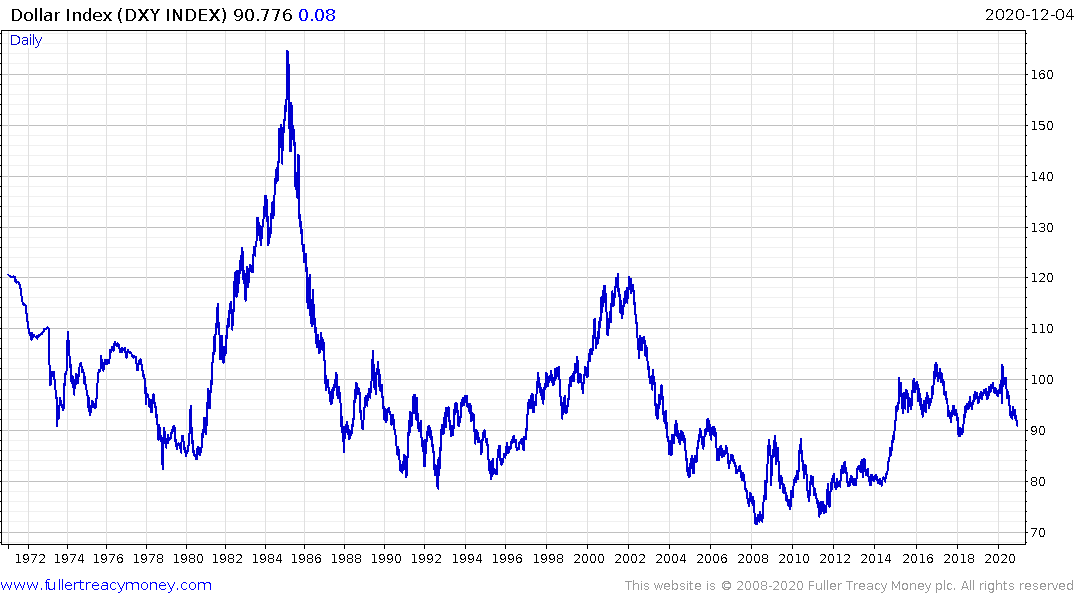

The big change, which is secular in nature, is the Dollar has broken downwards. That is a catalyst for increasing interest in non-US markets from the perspective of international institutional investors. The recent turn to outperformance of non-US markets is still only in its infancy but as long as the Dollar trends lower, the rationale for diversifying will only growth stronger.

The long-term chart of the Bloomberg Dollar Index exhibits three examples of 5/6-year uptrends. Each was followed by moves to new reaction lows. The big bull market between 1980 and 1985 was more than reversed. The uptrend from 1995 to 2001 took a while to put in a top formation but ultimately made a new low. The uptrend from 2011 to 2016 has taken four years to put in a top formation but now looks likely to break and trend lower.

If we turn our attention to what has been normal in terms of downtrends, the average peak to trough move has been seven years. 1985 to 1992 and 2001 to 2008. If that consistency is repeated, we would be looking at a new low for the Index and a terminal value sometime between 2024 and 2027 depending on how much weighting one is willing to give the Euro cross rate.

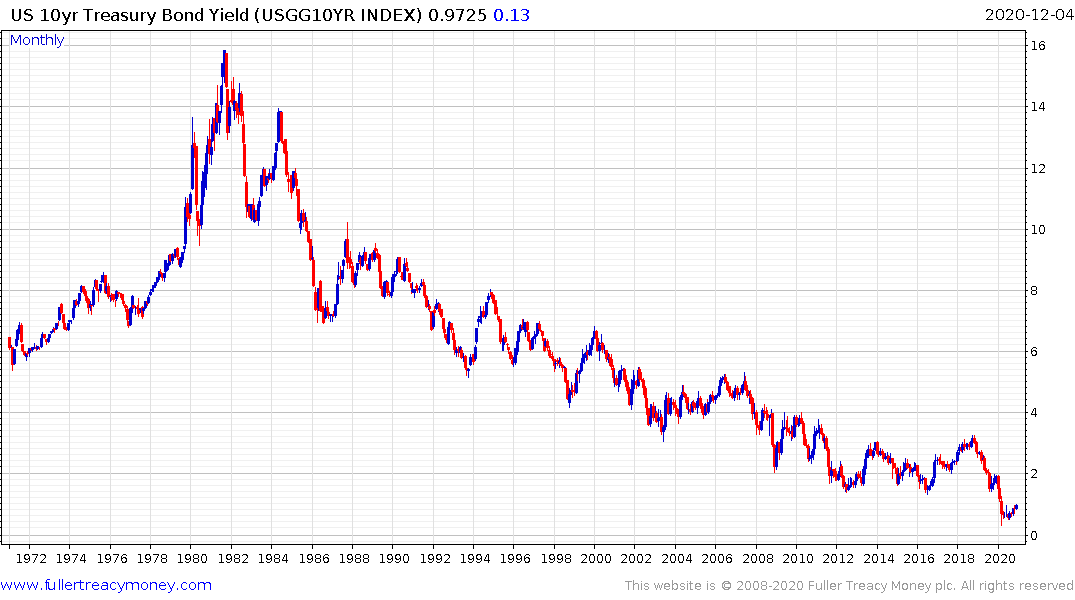

2020 and the pandemic panic ushered in helicopter money. That’s very difficult to unwind. 10-year yields are trending higher. Without clear policy changes to arrest the advance the yield curve is going to steepen further and hit a new high today. That is going to have a very deleterious effect on the ability of the US government to fund itself.

The reason the Dollar held its value for so long was because fiscal stimulus was being offset by the Fed’s quantitative tightening and interest rate policy. Today we are in the exact opposite scenario. The incoming Treasury secretary is a former Fed chairperson. That signals a level of cooperation between the monetary and fiscal arms of the government not seen since the early 1930s. The Fed will print whatever money the Treasury requires.

The long-term positive for gold. No country wants a strong currency so we can anticipate other countries will attempt to slow their currencies’ appreciation. Gold is likely to continue to attract interest as a hard asset with relatively limited supply.

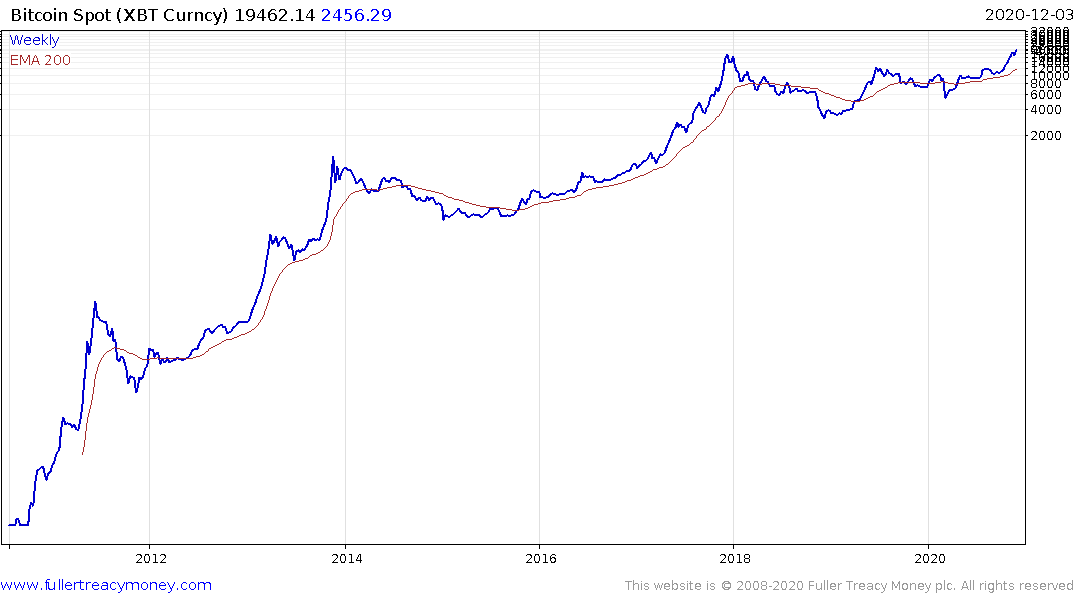

The relative attraction of cryptocurrencies and particularly bitcoin is seen in the same light and there is a generational divide between those who buy gold and those buying crypto. The range of possible access points to transact over the blockchain network is increasing, particularly with PayPal and Square’s entry into the market.

The announcement this week that Stripe is now offering Treasury services to anyone who wants to take deposits is a significant development. It might look like a digital equivalent of lay away or vendor financing but the ability of small companies to offer these services is a significant innovation. It offers a way to create a significant credit multiplier effect for the financial sector which has been absent since the financial crisis.

That has been one of the primary missing links in the route to inflationary outcomes over the last 12 years. Therefore, it is reasonable to assume that on this occasion the massive monetary stimulus and simultaneous monetary and fiscal actions will result in the inflation. This is quite similar to the inflation response to the student protests of the late 1960.

Wall Street is still in a bull market and it is still home to some of the most innovative companies in the world. In fact, with a weak Dollar, the foreign earnings of large companies will be flattered which should improve corporate profits.

However, the performance of the average stock in increasingly dependent on a weak currency. International investors have been free to invest in the USA over much of the last decade and had the benefit of capital market appreciation, the currency and yield in their favour. Today, international markets are rallying despite strong currencies. That is symptomatic of a significant change in direction of international flows.

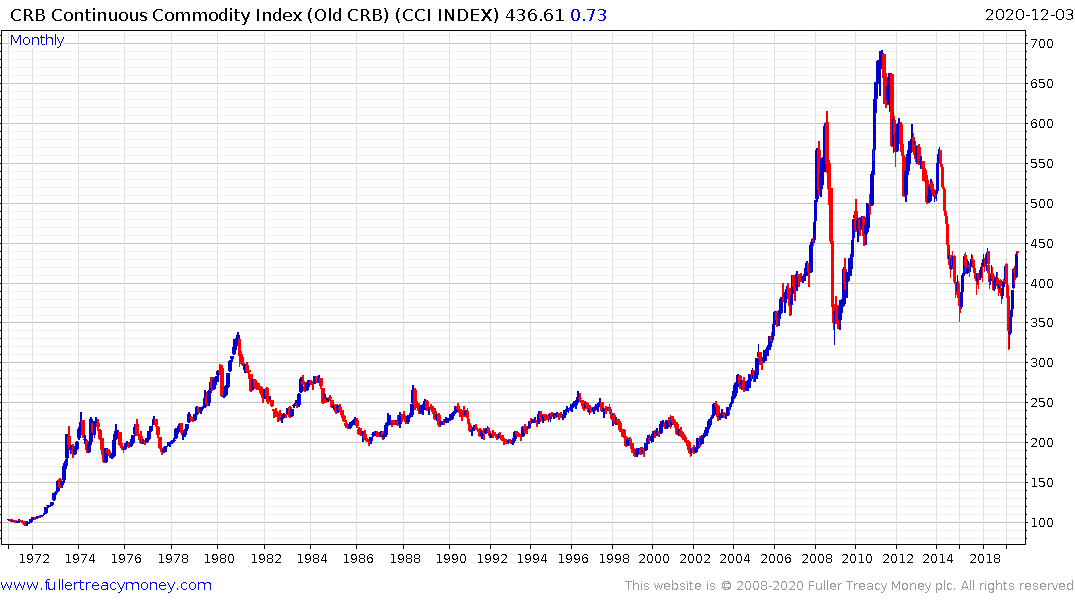

The declining Dollar is positive for both commodities and emerging markets but not so great for Treasuries. That virtually ensures the Fed will need to continue to buy bonds to support the market.

The unweighted Continuous Commodity Index in the process of completing a five-year base formation. Copper in particular is trending higher.

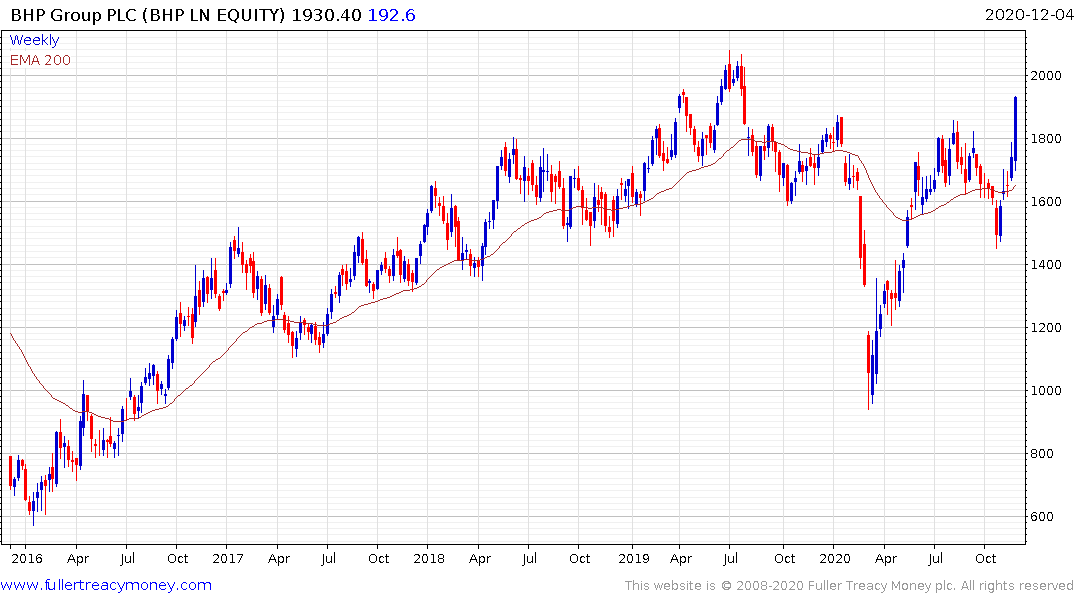

Individual shares like Rio Tinto, BHP or Glencore are all on recovery trajectories. The lengthy bear market has chastened management teams so that supply inelasticity is a factor in the commodity markets once more.

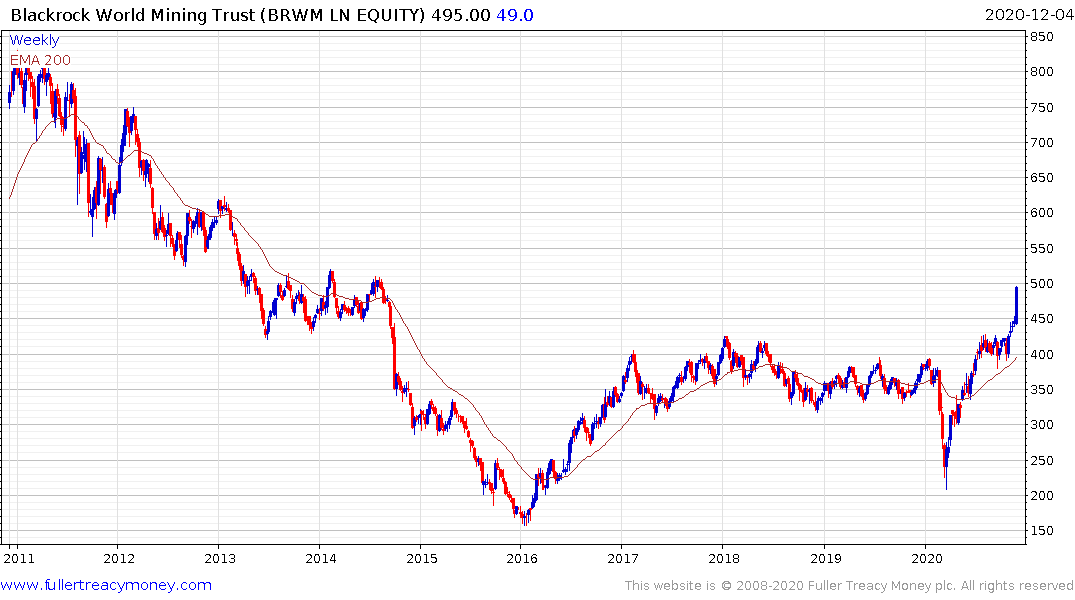

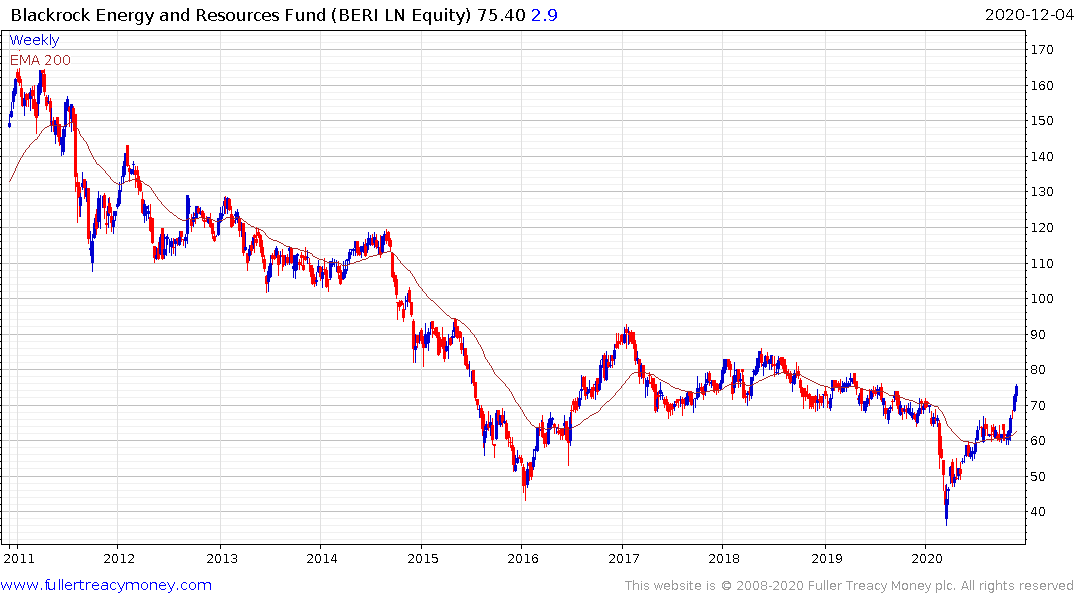

That is supporting the outlook for miners. The Blackrock World Mining Trust and the Blackrock World Energy and Resources Trust continue to extend breakouts.

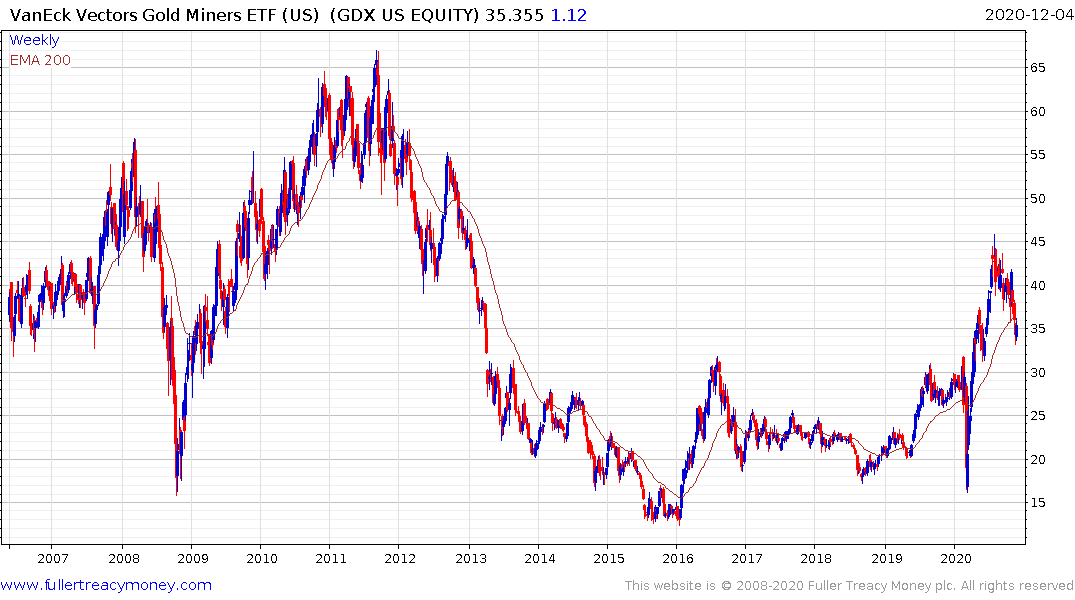

The Gold Miners ETF is currently steadying from the region of the trend mean and remains on a medium-term recovery trajectory.

The primary benefit for the mining sector is that a significant rationalization has already taken place. The survivors are now much better leveraged to rising commodity prices than they were at the peaks in 2011.

Significant rationalization is also ongoing in the energy sector. Many shale producers have been boosting production at uneconomic levels over the last decade. That trend is now over. The sector has also been chastened by the bear market so we are seeing significant write-downs. For example, $20 billion from Exxon this week. The winners are likely to be the larger companies best able to adapt to the changing regulatory environment.

The Energy SPDR ETF continues to firm from the region of the trend mean; suggesting the worst is probably behind the sector for at least the medium term.

The two regions with advanced plans for decarbonization are also those that benefit least from the petrodollar internal currency regime. Both Europe and China are heavily dependent on imported oil and chaff at the need to hold US Dollars to pay for commodities. Pioneering renewable energy solutions, batteries, green hydrogen etc. fulfill the aims of energy independence, currency independence and geopolitical independence. That’s more of a priority for China than it is for Europe.

China’s willingness to allow the renminbi to appreciate and its preference for lending to emerging markets via the Belt and Road program over the US government are some of the most acute sources of geopolitical strife globally. China’s creation of a digital currency is an additional source of potential friction. In many respects these actions can be considered as China securing its supply lines. That is in preparation for war.

Technological competition is a necessary component of that strategy.

The evolution of renewable energy solutions is not directly leading to a weaker US Dollar but the two issues are certainly connected in a broad sense.

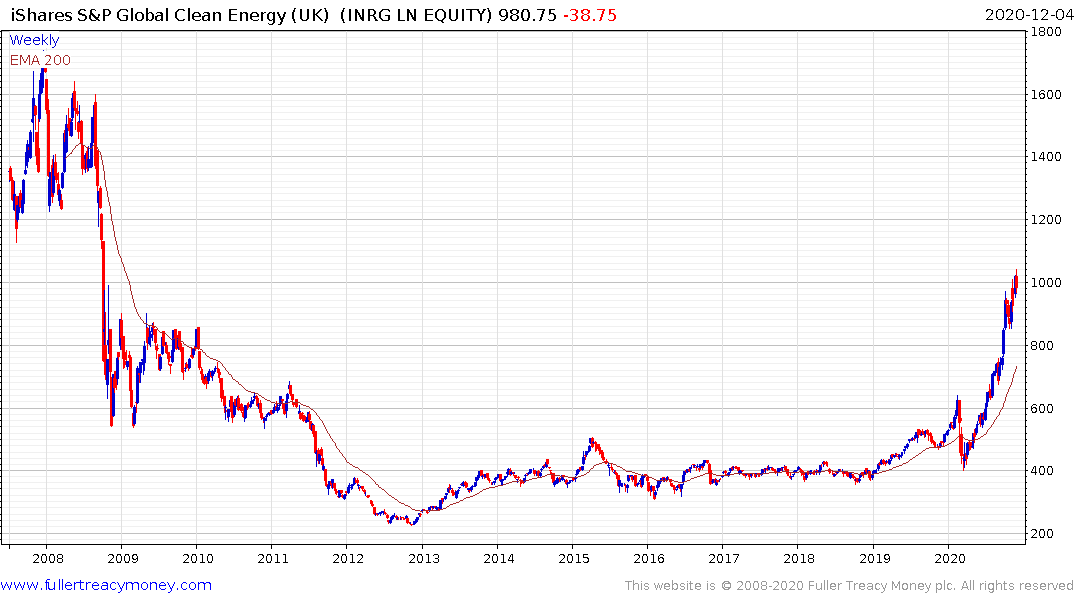

The iShares Clear Energy ETF remains on a recovery trajectory.

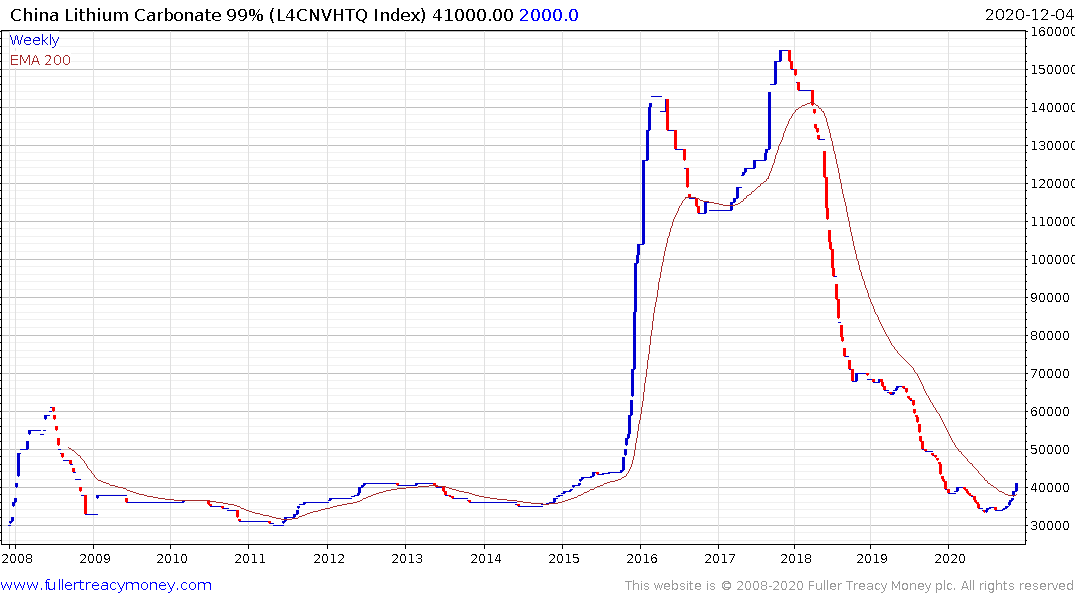

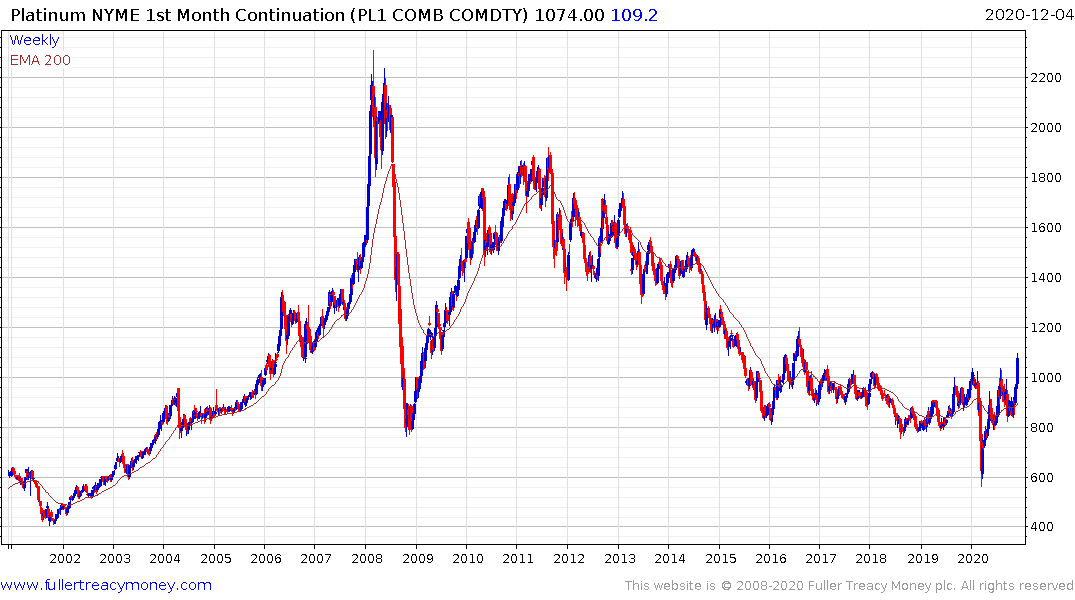

Lithium and platinum are now on recovery trajectories since they benefit from the increasing demand for batteries and hydrogen fuel cells respectively.

This report from Candriam may be of interest.

The weaker Dollar and ongoing La Nina weather pattern are also supporting a recovery in most agricultural commodities.

Many fertilizer and seed companies are now rebounding from very depressed levels.

The other agriculture sector that is coming off very depressed levels is cannabis. We live in an increasingly licentious society and demand for distractions continues to rise. There is increasing potential that a Biden-led administration will relax the Federal prohibition of cannabis and shares are beginning to respond.

The Alternative Harvest ETF is now in the process of completing a six=month base formation.

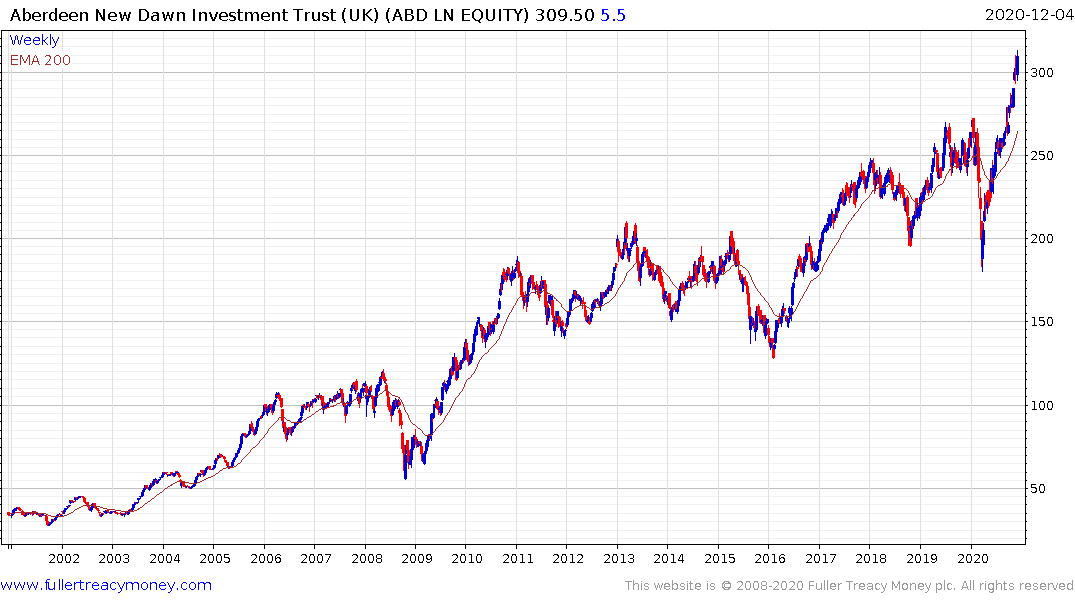

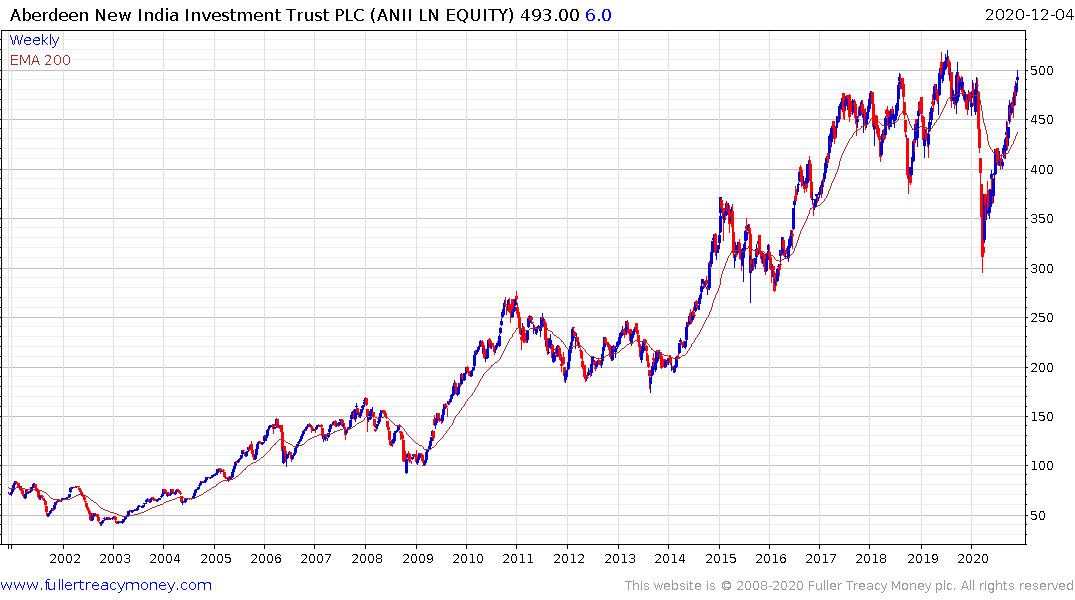

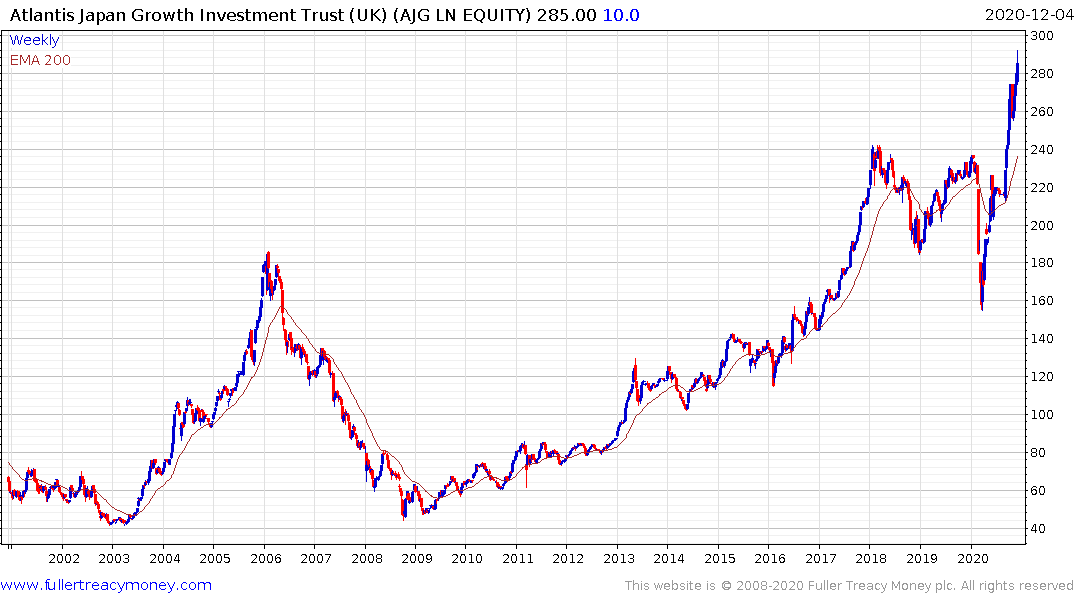

The Aberdeen New Dawn Investment Trust, The Aberdeen New India Investment Trust and the Atlantis Japan Growth Fund remain on recovery trajectories.

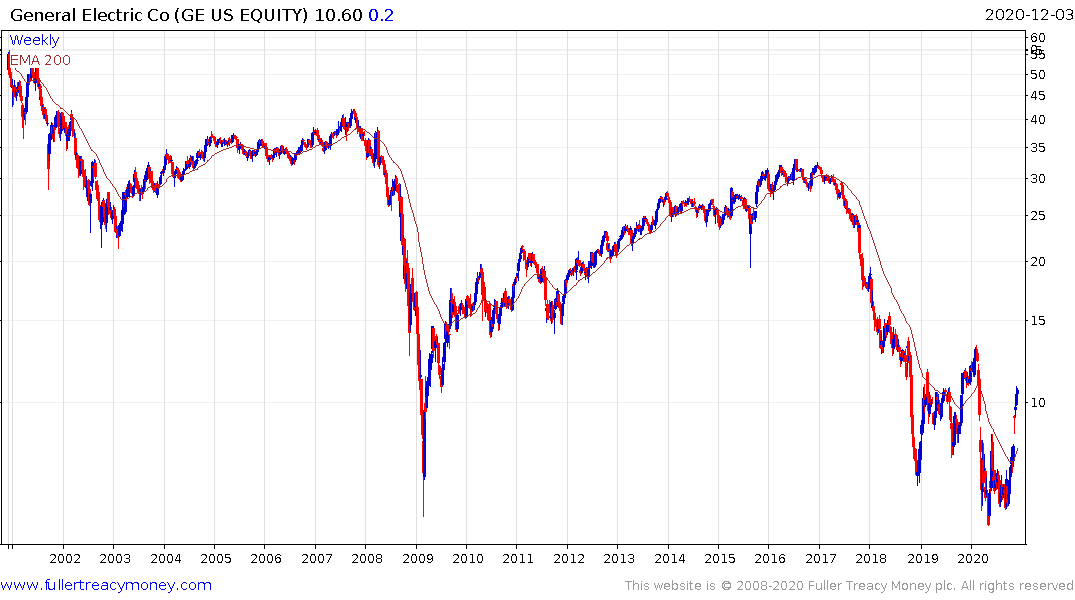

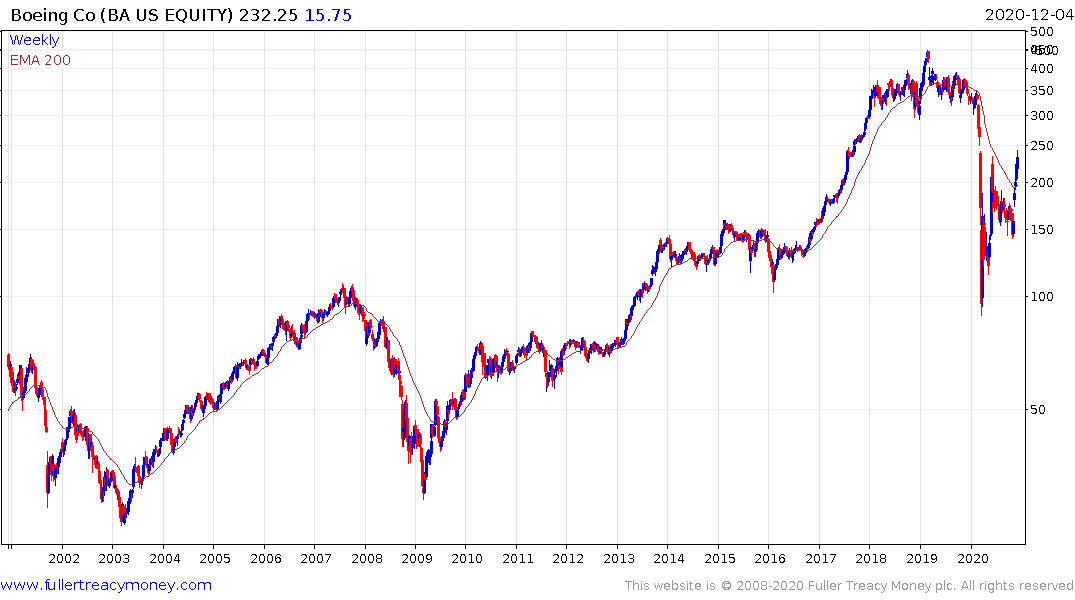

The challenge with looking at recovery candidates in the industrial sector is the percentage moves are so large close to the bottom that a less than ideal entry point can be a source of stress while a choppy recovery takes place. The only way to tackle that challenge is to adjust position sizes to allow for the possibility of volatility providing a more favour entry point.

.png)

Industrials like Rolls Royce, General Electric, Pitney Bowes and Boeing are currently rallying from very depressed levels.