Musings From the Oil Patch May 1st 2018

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. Here is a section:

The Bloomberg article highlighted the plight of Big Oil. Its weighting in global equity indices is at a 50-year low. Of the MSCI World Index’s 100 biggest stocks, only six are oil producers. Within the Standard & Poor’s 500 Index, Exxon Mobil Corp. (XOM-NYSE), which a decade ago was the largest company, has fallen to ninth place, and investors are requiring higher dividend yields to sustain the share price. So, what’s the problem for Big Oil? Simple. There is a perception that the world is awash in oil at the same time its long-term demand may be falling due to the public’s embrace of climate change policies promoting renewable energies and electric vehicles.

Institutional money manager Kevin Holt of Invesco Ltd. was quoted in the Bloomberg article saying, “Earnings have started to come through but no one believes it’s sustainable. That’s why the stocks haven’t worked even though the commodity has gone up. Everyone’s saying they don’t believe it.”

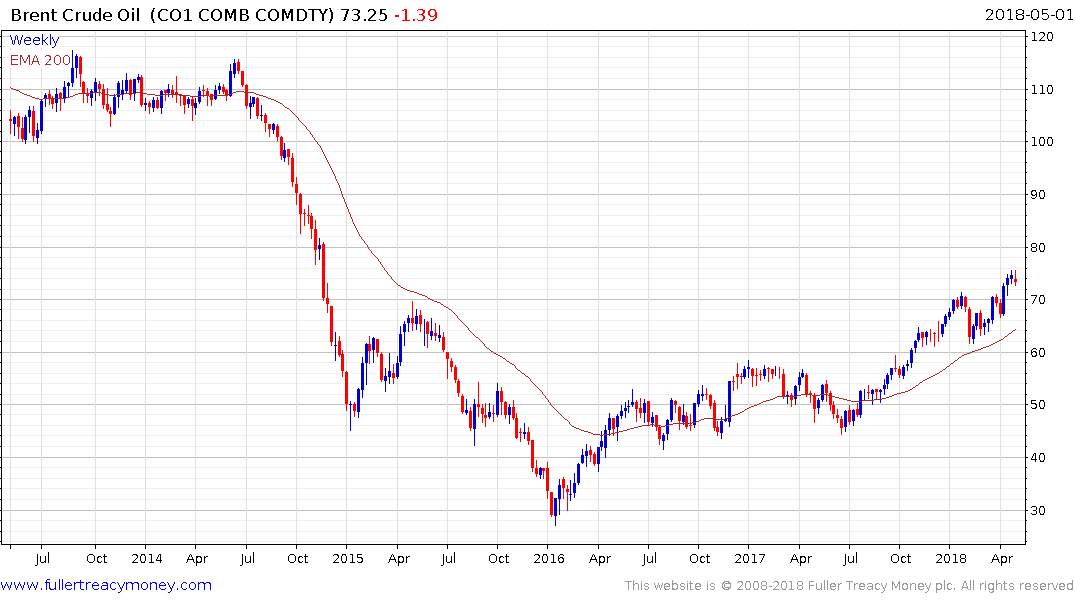

Stock market valuations are the collective view of investors as to the future earnings and dividend prospects for companies. Current low valuations are a manifestation of the industry’s negative perception. Mr. Holt is certainly correct about oil prices. Since the start of this year, Brent/WTI prices have climbed 12.2%/13.3% through April 23rd. If we go back to the oil price low of 10 months ago, prices have soared by 66.7%/61.4%. In the past, an increase in oil prices of those magnitudes would have sparked a meaningful recovery in oil company and oil-related company share prices.

A report by the oilfield service research team at Barclays delivered a similar message about their universe of stocks as cited by Bloomberg about Big Oil. The most telling chart shows a nearly complete correlation (0.96) between the movement in oil prices and the value of the Philadelphia Oilfield Service Stock Index (OSX) between January 2012 and January 2016. However, from June 2017 to April 2018, the correlation has fallen to only 0.06. And, June 2017 marked the low price for crude oil!

Here is a link to the full report.

One of the biggest consensuses in the markets at present is that the future is going to be carbon free, and not in a couple of decades but imminently. There is no doubt that electric car penetration is rising, particularly in China, but it will still be years before it reaches even 10% of the global fleet. I think there is reason for optimism about the future of carbon emissions based on technological improvements alone but perhaps enthusiasm has overtaken the reality represented by the market.

The higher oil prices rise, the greater the incentive suppliers have to bring additional product to market. That is particularly relevant for higher cost producers like Canada and Brazil. Right now, the price is pausing in the region of $75 and there is scope for some consolidation of the short-term overbought condition. The longer prices remain high the greater the possibility that spending on drilling will increase.

The Oil Service ETF (OIH) remains confined to a base formation and a sustained move above $30 will be required to confirm a return to demand dominance.

BP broke out of a 5-year base formation today and will need to hold the move above 500p if medium-term recovery potential is to be given the benefit of the doubt.

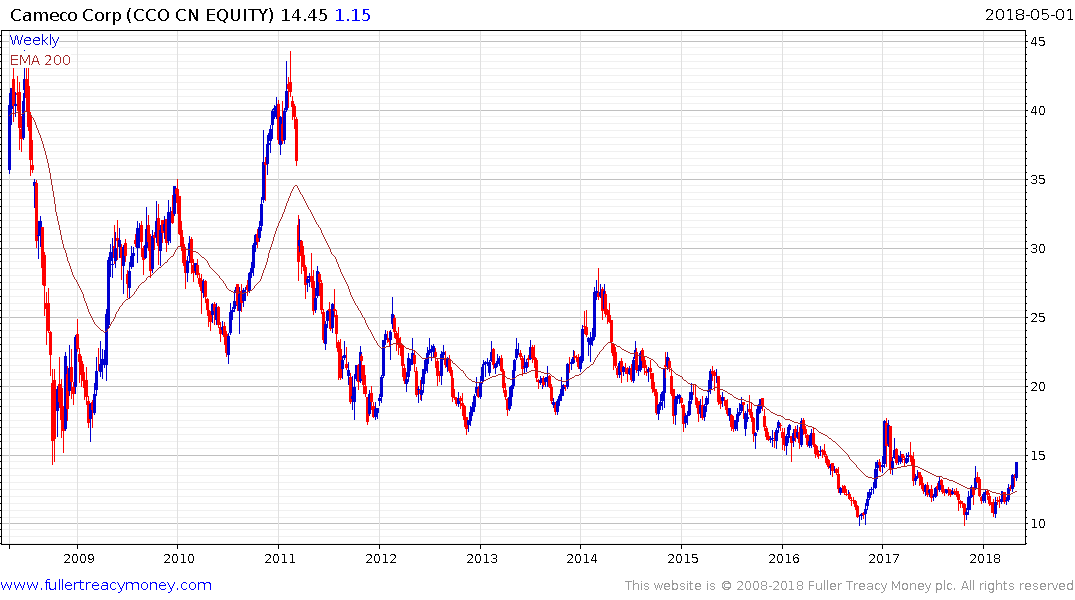

There are also very tentative signs that the uranium sector is garnering attention. Cameco is back pressuring the C$15 area and a clear downward dynamic will be required to confirm resistance in that area.