Musings from the Oil Patch July 19th 2017

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. Here is a section:

The latest topic of interest in the oil and gas business is the lack of new discoveries given the cutback in capital investment in keeping with Mr. Dudley’s “capital diet.” What does this mean for the industry’s future? The International Energy Agency (IEA) has sounded the alarm over sharply higher oil prices in the 2020-2022 time frame due to a lack of industry capital spending. With capital spending cut by 25% in 2015 and by another 26% in 2016, prospects are increasing for a growing gap in the future output trajectory for oil. Current expectations call for a modest increase in capital spending during 2017, but that increase could prove overly optimistic should oil prices fail to recover in the second half.

The IEA warned in its Oil 2017 report of a possible imbalance between demand and supply growth, leading to the smallest global spare production capacity surplus in 14 years by 2022. That conclusion is based on demand growth for 2016-2022 of 7.3 million barrels per day (mmb/d), which exceeds the projected supply growth of under 6 mmb/d. A possible relief valve might be the growth in U.S. shale output. As Dr. Fatih Birol, the IEA’s executive director put it: “We are witnessing the start of a second wave of U.S. supply growth, and its size will depend on where prices go.” He went on to say, “But this is no time for complacency. We don’t see a peak in oil demand any time soon. And unless investments globally rebound sharply, a new period of price volatility looms on the horizon.”

The supply shortage view seems to be gaining traction among oil and gas industry professionals. Halliburton Company’s (HAL-NYSE) Mark Richard, senior vice president of global business development and marketing, told the World Petroleum Congress that “You’ll see some kind of spike in the price of oil, maybe somewhere around 2020, 2021." This fits with Bernstein Research’s latest oil price downgrade. The firm now sees oil prices exhibiting a U-shape cyclical pattern: after having declined from over $80 a barrel in 2014, they traded in the $40s for 2015-2016, and will now be flat at $50 for 2017-2018 before slowly climbing back to $70 by 2021.

Here is a link to the full report.

Synchronised global economic expansion is generally positive for energy consumption and most particularly in emerging markets where the bulk of energy demand growth is expected to originate. How quickly battery technology advances to quell range and charging time questions is likely to represent a significant a key arbiter for whether bullish forecasts come to fruition over the next five years.

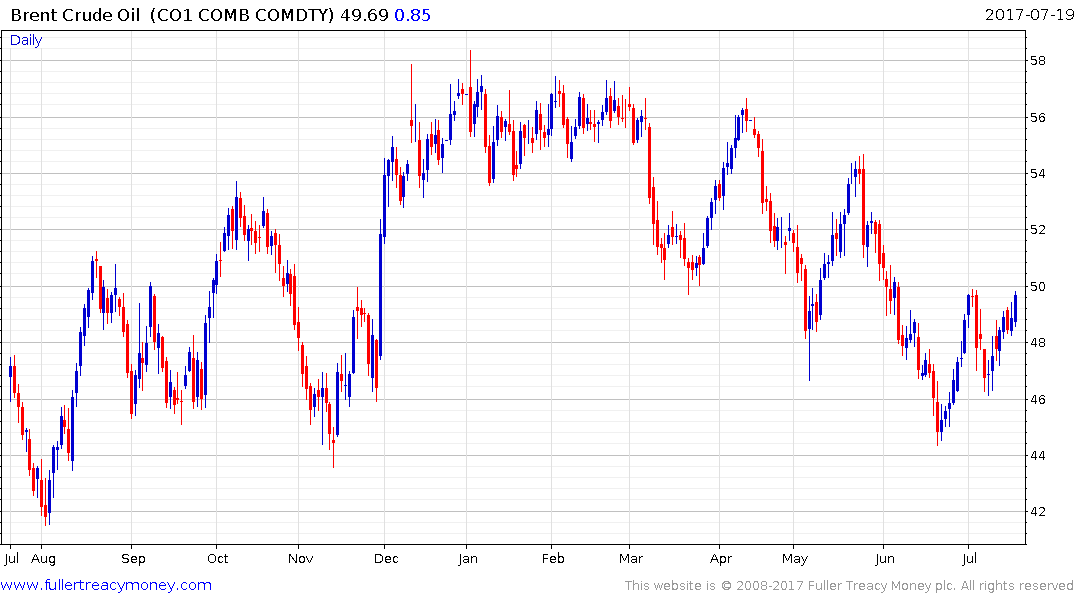

I find it interesting that bullish forecasts are at least medium-term in nature while the challenging environment we have been presented with this year is not questioned. No doubt trading oil has been difficult this week considering the volatility but it now is an interesting time to address the charts.

Brent crude hit a low near $45 in June and posted the first higher reaction low since February on July 10th. It is now testing the most recent lower high near $50 and a sustained move above that level would begin to signal a return to demand dominance beyond short-term steadying.

I’ve been of the view for what feels like a long time that oil prices are more likely to range than trend and that we can expect volatility. However, that works both ways and there is the potential that oil prices could rally back towards the upper side of the evolving congestion area. A great deal of supply becomes economic near $60 so that is an important future hurdle for oil prices.