Musings from the Oil Patch April 4th 2017

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB which may be of interest. Here is a section:

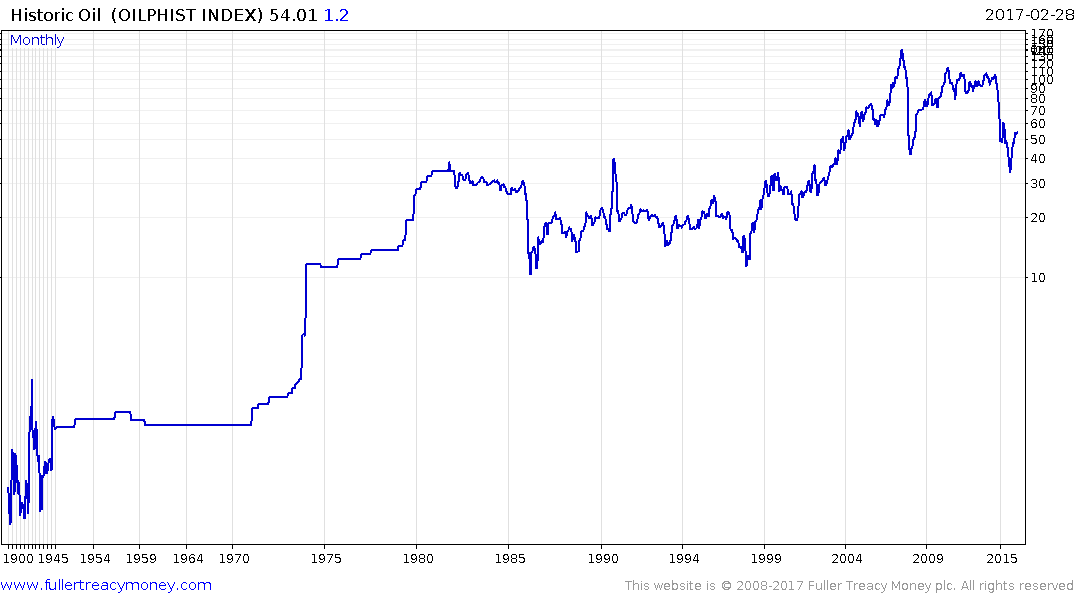

As we contemplate the next cycle, we cast our view back on the industry’s history. The last great cycle came out of the explosion in oil prices in the latter half of the 1970s due to geopolitical events, but realistically it resulted from the peaking of U.S. oil output and the transferring of pricing power to the OPEC cartel. What broke the back of that price explosion was new, large sources of oil – offshore basins in the North Sea and West Africa, in particular, along with Alaska. Those were the resources that drove the industry over the subsequent 30 years. Shale is what is driving the industry now, and likely will drive it for the foreseeable future. What could that mean for oil prices? Look at Exhibit 1 where we show the inflation-adjusted oil prices from the late 1960s to 2016. After the bust of the early 1980s, the oil price traded for 18 years without ever going above $45 a barrel in current dollar prices except in response to one-off geopolitical events.

The recent oil price bust followed a much longer period of super-high oil prices than in the 1970s. To our way of thinking, we are likely to experience another extended period of lower, but stable, oil prices. Will it be 18 years? We don’t know. Will oil prices stabilize around $45 a barrel? We don’t know. Might the price range be $55-$60 a barrel? It could be. Will it be $70 a barrel or more? We doubt it, except for brief periods. This isn’t because we think history always repeats itself, but rather because the oil industry is fighting maturing economies around the world, meaning slower demand growth. Developing economies are where oil demand is growing the fastest, but those countries have the benefit of employing the most recent equipment designs and technologies, suggesting their economies will be much more energy-efficient than earlier developing economies at the same point in time. Think about how no country now would consider string telephone wires to allow communication – cell towers are the answer. The oil industry is also fighting a global push to de-carbonize economies in order to fight the damage of climate change, which has the potential to significantly lower global oil consumption growth.

Here is a link to the full report.

This piece rhymes very strongly with our long-held view that shale oil and gas represent game changers for the energy complex. This has resulted in US onshore shale now representing an important swing producer for the global market.

This very long-term chart of oil prices highlights three long-term ranges interspersed with multi-year bull markets. We have just lived through a decade of high energy prices and if the 125-year pattern is to remain intact it is reasonable to expect prices will be largely rangebound for at least another decade. That is not particularly beneficial for a buy and hold strategy but it will represent a fertile ground for volatility traders where trough to peak swings could be in the order of more than 100%.

EOG Resources is one of the larger shale oil producers and bounced this week from the region of its trend mean.