Lithium 101

Thanks to a subscriber for this comprehensive heavyweight 170-page report on lithium. If you have questions on the lithium sector the chances are they will be answered by this report. Here is a section:

Global lithium S&D analysis highlights opportunity for high-quality assets

The emergence of the Electric Vehicle and Energy Storage markets is being driven by a global desire to reduce carbon emissions and break away from traditional infrastructure networks. This shift in energy use is supported by the improving economics of lithium-ion batteries. Global battery consumption is set to increase 5x over the next 10 years, placing pressure on the battery supply chain & lithium market. We expect global lithium demand will increase from 181kt Lithium Carbonate Equivalent (LCE) in 2015 to 535kt LCE by 2025. In this Lithium 101 report, we analyse key demand drivers and identify the lithium players best-positioned to capitalise on the emerging battery thematic.Global lithium demand to triple over the next 10 years

The dramatic fall in lithium-ion costs over the last five years from US$900/kWh to US$225/kWh has improved the economics of Electric Vehicles and Energy Storage products as well as opening up new demand markets. Global battery consumption has increased 80% in two years to 70GWh in 2015, of which EV accounted for 35%. We expect global battery demand will reach 210GWh in 2018 across Electric Vehicles, Energy Storage & traditional markets. By 2025, global battery consumption should exceed 535GWh. This has major impacts on lithium. Global demand increased to 184kt LCE in 2015 (+18%), leading to a market deficit and rapid price increases. We expect lithium demand will reach 280kt LCE by 2018 (+18% 3-year CAGR) and 535kt LCE by 2025 (+11% CAGR).Supply late to respond but wave of projects coming; prices are coming down

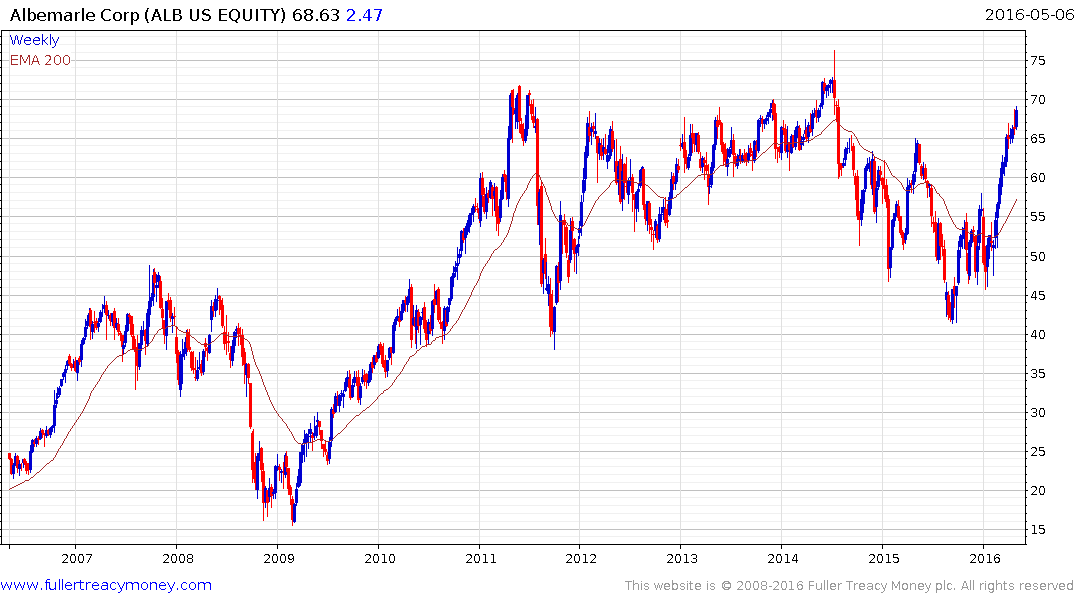

Global lithium production was 171kt LCE in 2015, with 83% of supply from four producers: Albemarle, SQM, FMC and Sichuan Tianqi. Supply has not responded fast enough to demand, and recent price hikes have incentivized new assets to enter the market. Orocobre (17.5ktpa), Mt. Marion (27ktpa), Mt. Cattlin (13ktpa), La Negra (20ktpa), Chinese restarts (17ktpa) and production creep should take supply to 280kt LCE by 2018, in line with demand. While the market will be in deficit in 2016, it should rebalance by mid-2017, which should see pricing normalize. Our lithium price forecasts are on page 9.

Here is a link to the full report.

The cost of lithium ion batteries falling rapidly and the fact this is occurring at the same time solar cells costs have been trending lower is a major incentive for installations of both technologies; increasingly in parallel. With costs coming down and technology improving growth in demand is a major consideration as factories achieve scale and miners invest in additional supply.

That suggests lithium represents a “supply inelasticity meets rising demand” bullish scenario until significant new supply reaches market, which could take upwards of three years. The growth of the lithium market represents a challenge for the fossil fuel sector because while it is small right now it is doubling every year and will increasingly eat into gasoline demand.

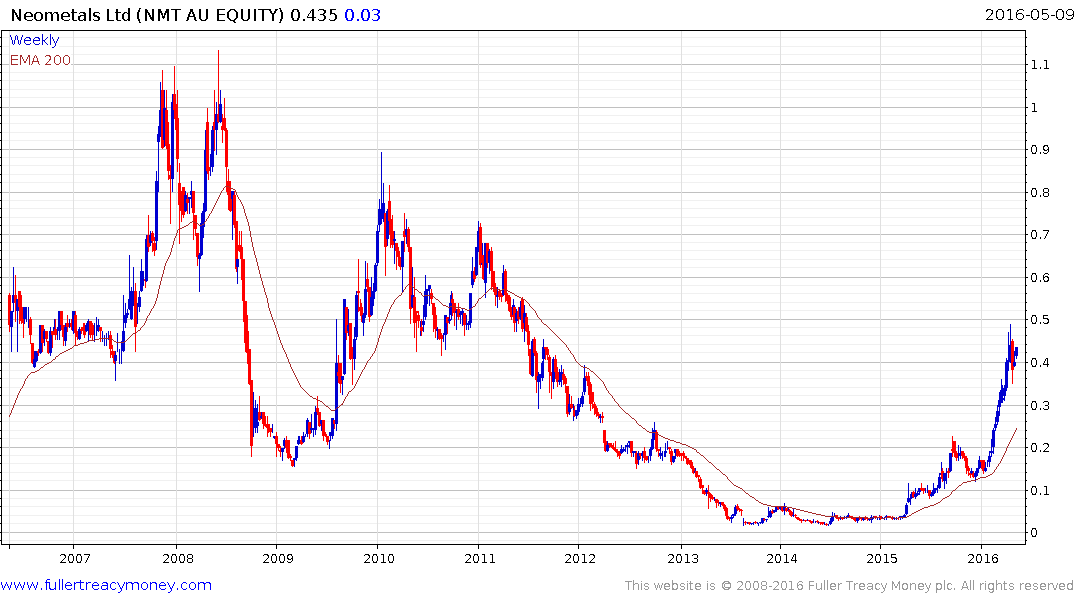

Albemarle, Orocobre and Neometals have been leading the market higher. Meanwhile FMC Corp pulled away from the region of the trend mean last week to complete a six-month base and a sustained move below $42 would now be required to question recovery potential.