Beyond Algiers

Thanks to a subscriber for this report from Goldman Sachs which was issued on the 27th, ahead of the OPEC meeting. Here is a section:

Nonetheless, our 4Q16 oil supply-demand balance is weaker than previously expected given upside surprises to 3Q production and greater clarity on new project delivery into year-end. This leaves us expecting a global surplus of 400 kb/d in 4Q16 vs. a 300 kb/d draw previously. Importantly, this forecast only assumes a limited additional increase in Libya/Nigeria production of 90 kb/d vs. current estimated output. As a result, we are lowering our 4Q16 forecast to $43/bbl from $50/bbl previously. While a potential deal could support prices in the short term, we find that the potential for less disruptions and still relatively high net long speculative positioning leave risks skewed to the downside into year-end. Importantly, given the uncertainty on forward supply-demand balances, we reiterate our view that oil prices need to reflect near-term fundamentals – which are weaker – with a lower emphasis on the more uncertain longer-term fundamentals.

Despite a weaker 4Q16, our 2017 outlook is unchanged with demand and supply projected to remain in balance. We expect demand growth to remain resilient while greater than previously expected production declines in US/Mexico/Venezuela/ Brazil/China are offset by greater visibility in the large 2017 new project ramp up in Canada/Russia/Kazakhstan/North Sea. While our price forecast remains unchanged at $52/bbl on average for next year with a 1H17 expected trading range of $45- $50/bbl, we continue to view low cost and disrupted supply as determining the path of an eventual price recovery with our forecasts conservative on both. As we wait for headlines from Algiers, it is worth pointing out that Iran, Iraq and Venezuela have each guided over the past month to a 250 kb/d rise in production next year.

Here is a link to the full report.

Saudi Arabia’s commitment to support a production cut by OPEC of 750.000 barrels made headlines and has influenced the oil market by disrupting the perception, described above, of a balanced market overall. What appears to have made fewer headlines is that Iran will be omitted from the agreement and is therefore free to continue to increase supply in order to regain the market share it lost due to sanctions. Therefore the most likely result is a limited supply cut overall while any boost to prices will encourage unconventional drilling suggesting a cut may be short lived.

Perhaps more important however is the perception that the Saudi Arabians are willing to put their animosity with Iran aside in favour of making money to support their economy. That also represents an Achilles’ heel to their geopolitical position since it clearly highlights just how dependent the kingdom is on high oil prices. As a result it would be rash to assume they will continue to make concessions to support higher prices

Brent crude experienced a sharp rebound from the January low, almost doubling, in a Type-2 massive reaction against the prevailing downtrend. It has since moved into a predicable ranging phase or right-hand extension and is currently firming from the region of the trend mean. A clear downward dynamic wold be required to question potential for some higher to lateral ranging overall.

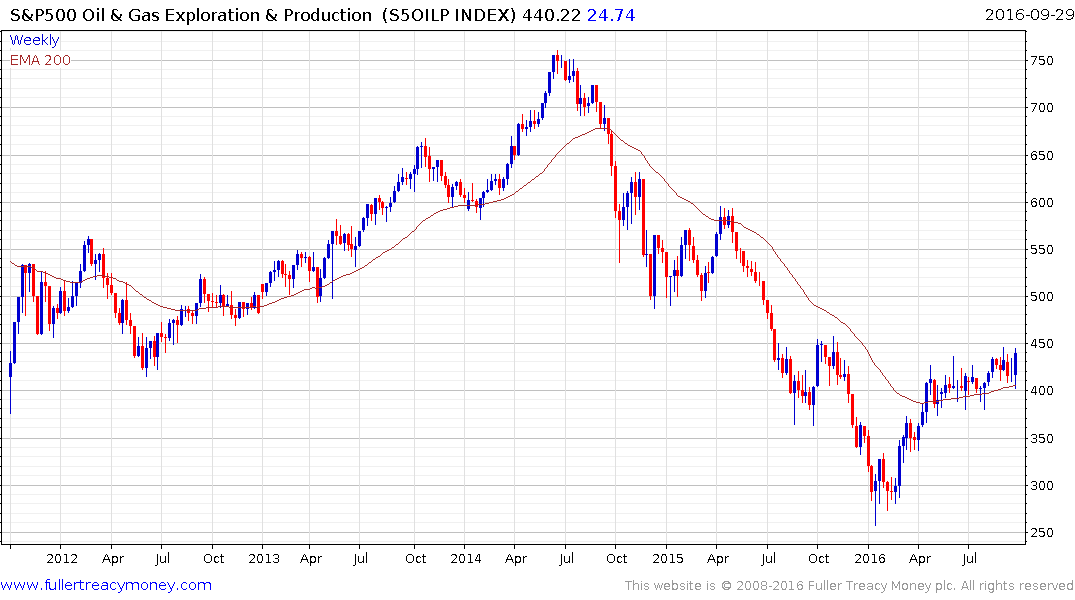

The S&P500 Oil & Gas Exploration and Production Index bounced emphatically from the region of the trend mean today and a sustained move below 400 would be required to question the upward bias.

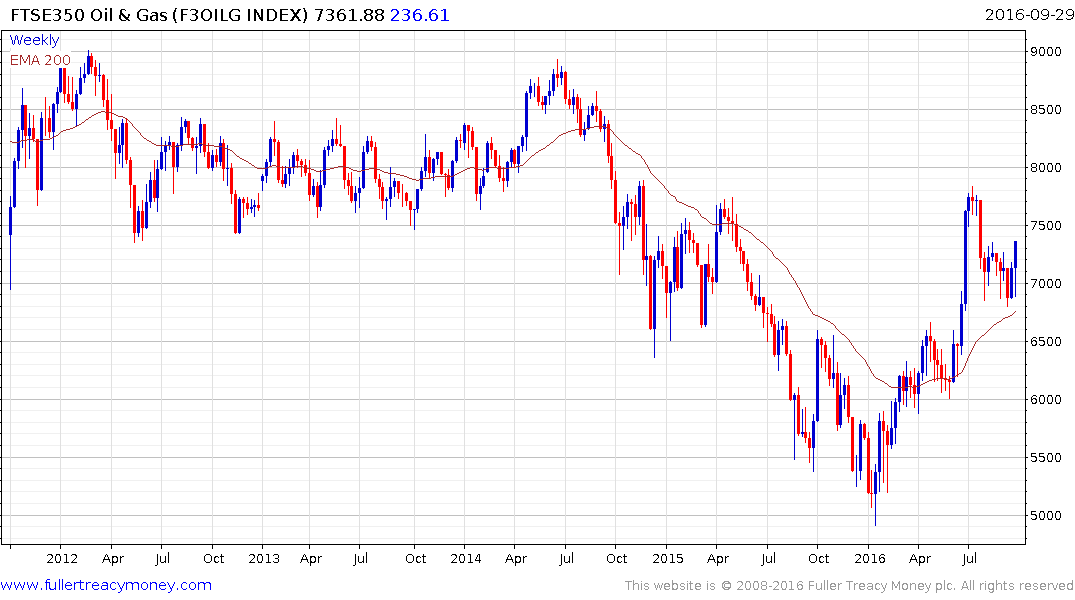

The FTSE 350 Oil & Gas Producers Index has also now bounced from the region of the trend mean.

Somewhat higher oil prices represent a headwind for refiners with both Marathon Petroleum and Tesoro among the worst performers on the S&P500 today.

Back to top