Adobe Expertly Balances Growth and Profitability

This article from MorningStar following Adobe’s results on September 20th may be of interest to subscribers. Here is a section:

Third-quarter revenue rose 26% year over year to $1.46 billion, driven by 51% growth in the firm’s subscription revenue base. Creative Cloud continues to serve as the company’s key revenue driver, as both greenfield customers and cloud migrators are providing a consistent lift in the annual recurring revenue base. We believe ample growth opportunities remain across both Creative Cloud and Digital Marketing, particularly as consumer users migrate and enterprise customers consolidate digital content creation and marketing spend around suites of applications versus point solutions.

The company is beginning to show the two main benefits of renewal billings in its subscriber base, which are higher prices and substantially lower customer acquisition costs. As a result, GAAP operating margin exceeded our forecast by more than 300 basis points at 25%, the firm’s best quarterly mark since the fourth quarter of fiscal 2012. While we suspect the firm will need to maintain aggressive investment in sales and marketing, particularly as competition for digital marketing wins remains intense, we think the increasing renewal mix of Creative Cloud billings will smooth this effect, yielding mid-30s operating margins in the long run.

I’m reminded of an old adage that “you can sheer a sheep every year, but only send him for slaughter once” when looking at the success of Adobe’s subscription pricing model. A significant number of companies are now adopting the same policy, opting for the relative security of payments over the long-term versus relying on “lumpy” sales of new software.

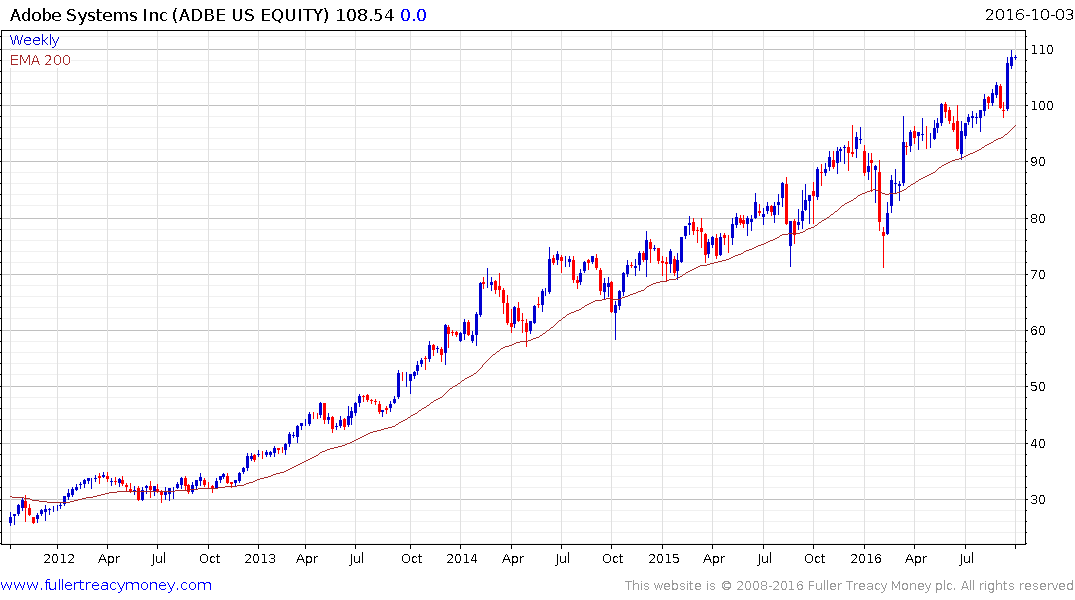

Adobe Systems has been trending consistently higher since 2011 and is somewhat overextended relative to the trend mean at present. While some consolidation is looking increasingly likely, a sustained move below $95 would be required to question potential for additional upside.

Microsoft has been rolling out a subscription model for its various MS Office products over the last few years. The share broke out of its most recent medium-term range in July and a sustained move below $53 would be required to question potential for additional upside.

Dassault Systems is also introducing a subscription pricing model and has so far held the breakout to new highs.

Autodesk now employs a subscription model for its market leading Maya animation software. The share has been the subject of a great deal of volatility over the last decade but moved to a new high in August and a sustained move below $65 would be required to question potential for additional upside.