Treasuries Soar Most Since Post-Brexit as Market Volatility Hits

This article by Brian Chappatta and Edward Bolingbroke for Bloomberg may be of interest to subscribers. Here is a section:

Treasuries extended gains across the curve, driving down benchmark yields by the most since the days after the June Brexit vote, as traders across financial markets backed away from crowded bets.

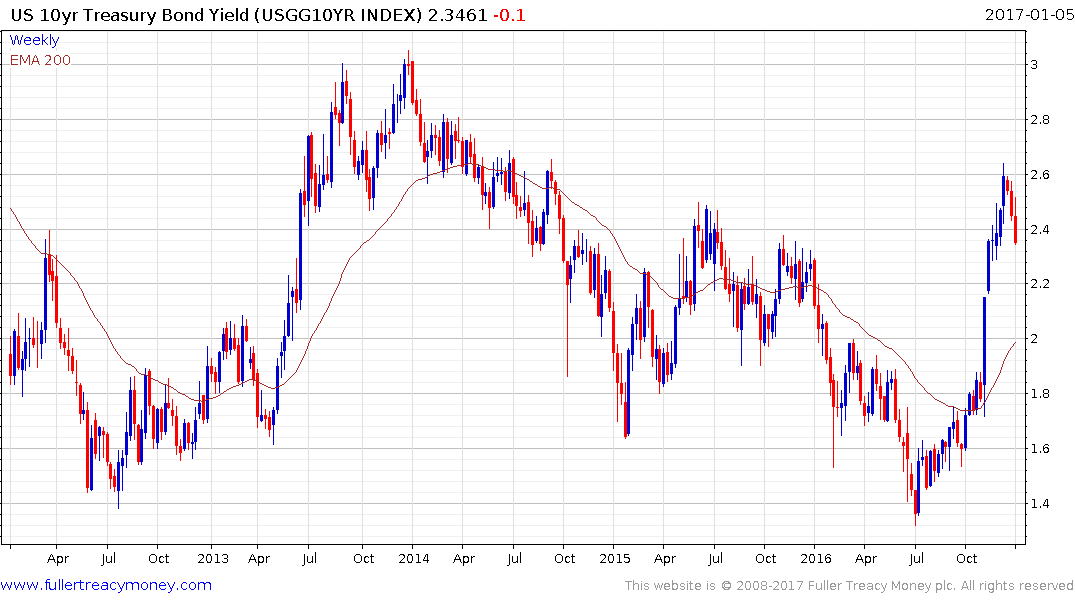

The benchmark 10-year U.S. yield plunged about eight basis points to 2.36 percent at 12:15 p.m. in New York, touching the lowest level since Dec. 8, according to Bloomberg Bond Trader data. It’s on pace for the biggest decline since June 27. The 10-year break-even rate, a market measure of inflation expectations, fell from close to the highest level since 2014.

Across financial markets, trends snapped Thursday as investors weighed the risk of a lackluster payrolls report Friday and the prospect that trades based on Donald Trump’s impending presidency had gone too far. Data from the ADP Research Institute on Thursday indicated companies added fewer jobs in December than forecast. The figures come a day before the Labor Department releases its monthly payrolls report.

“A bunch of the widely predicted trades for this year are all being broken at the same time, with oil going lower, investment-grade corporates widening out, TIPS break-evens tightening, and then rates rallying as a result,” said Mike Lorizio, a Boston-based senior trader at Manulife Asset Management, which oversees about $343 billion. “Some key levels being broken just inspired further buying.”

The odds are in favour of the view that the 35-year bull market in bonds is over, however it would be a mistake to think that such a lengthy expansion will end overnight. Inflationary expectations might well be justified in the medium-term but they have run ahead of the market and Treasury yields in the region of 2.5% are competitive with many equities and therefore desirable by bond investors conditioned over generations to buy the dip.

It is looking increasingly likely that the run-up in yields relative to the trend mean will be unwound. If this is in fact a completed top formation the yield will find support in the region of 2%.

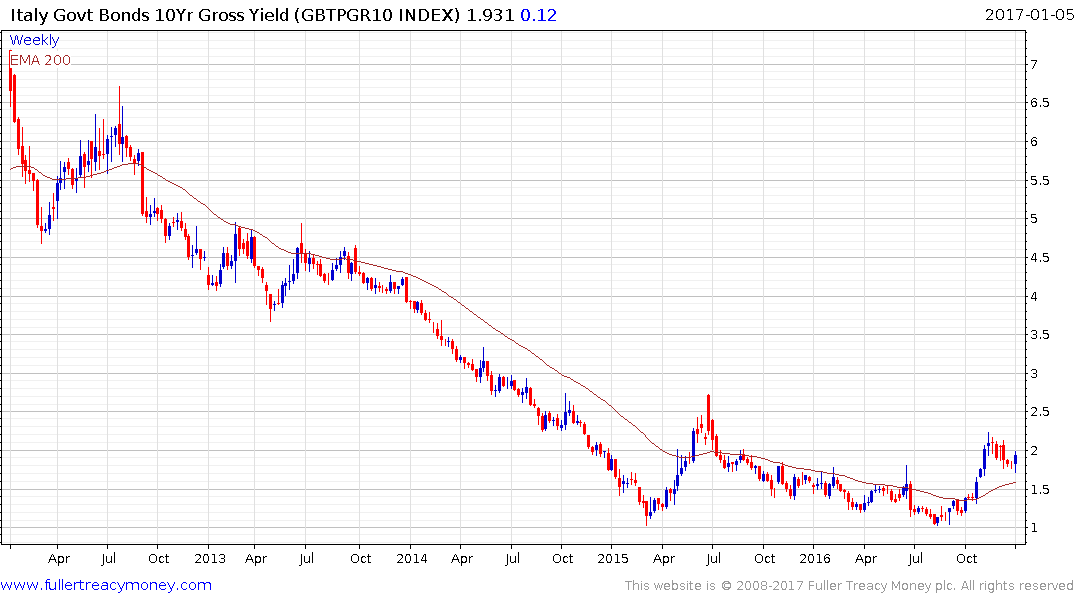

A condition had evolved in the bond markets towards the end of last year where US Treasuries had a higher yield than Italian BTPs. By shorting Treasuries and buying BTPs macro traders could play the Fed against the ECB. The pullback on Treasuries will have forced the liquidation of those types of trades and probably contributed to selling pressure in Italian bonds today.

One of the knock-on effects of Italy’s illegal bailout of its banks is that it highlights there is one set of rules for large countries and quite another for small countries within in the EU. Markets appear eager to test that theory because Portuguese bond yields broke out today suggesting bearish bets are being taken on the country’s prospects to self-sustain a recovery.