The Impact of the NSFR on the Precious Metals Market

This letter sent by the London Bullion Market Association (LMBA) and the World Gold Council to the Bank of England for the attention of the Bank of International Settlements may be of interest to subscribers. Here is a section:

An 85% RSF charge would:

• Undermine clearing and settlement – The required stable funding for short-term assets would significantly increase costs for LPMCL clearing banks to the point that some would be forced to exit the clearing and settlement system, which may even be at risk of collapsing completely.

• Drain liquidity – The required stable funding would dramatically increase costs for remaining LPMCL members taking gold on deposit to be held as unallocated metal relative to the cost of providing custody of allocated metal. This would prevent LPMCL clearing banks from holding unallocated metal and drain essential liquidity from the clearing and settlement system. These unallocated balances are the only material source of liquidity in the clearing and transaction financing systems. Without this liquidity, there would be a material deleterious effect on the global precious metals market.

• Dramatically increase financing costs – The required stable funding would penalise LBMA members who hold unallocated balances of precious metals. This would increase the cost of short-term precious metals financing transactions as stable funding costs are passed through to non-bank market participants. Such cost increases would impact miners, restrict refining and raise the costs of an inelastic key input to industrial and consumer goods. This includes some essential medical equipment and technologies required to reduce pollutants (such as catalytic converters).

• Curtail central bank operations – Fewer LPMCL clearing banks may curtail central bank deposit, lending and swaps in precious metals. These operations are essential to offset the costs of storing gold reserves and generating income. In addition, this provides important liquidity to the market. The effects of an 85% RSF charge would not just be limited to the London OTC market, but would be felt globally across the entire gold value chain. While London acts as the default settlement location for most global OTC spot transactions, the precious metals market is international. An undermining of the clearing and settlement system, reduced market liquidity, significantly increased financing costs and curtailed central bank activity would fundamentally alter the structure and attractiveness of this market.

Here is a link to the full report.

Most gold is trading is through fungible non allocated bars. Reducing liquidity in this over-the- counter market, while also elevating gold to a tier 1 asset could have the potential to create demand while reducing supply. That’s the recipe for a bull market; assuming the Basel III rules as they are currently envisaged pass into effect this month.

The big question is whether the bull market advance from 2019 was in response to central bank demand for gold in anticipation of the rule changes under Basel III. After two years of anticipation, how much of this change is already in the price? I suspect the impending reclassification was a contributing factor in the advance but the questions about liquidity and the LBMA’s protest are new pieces of information.

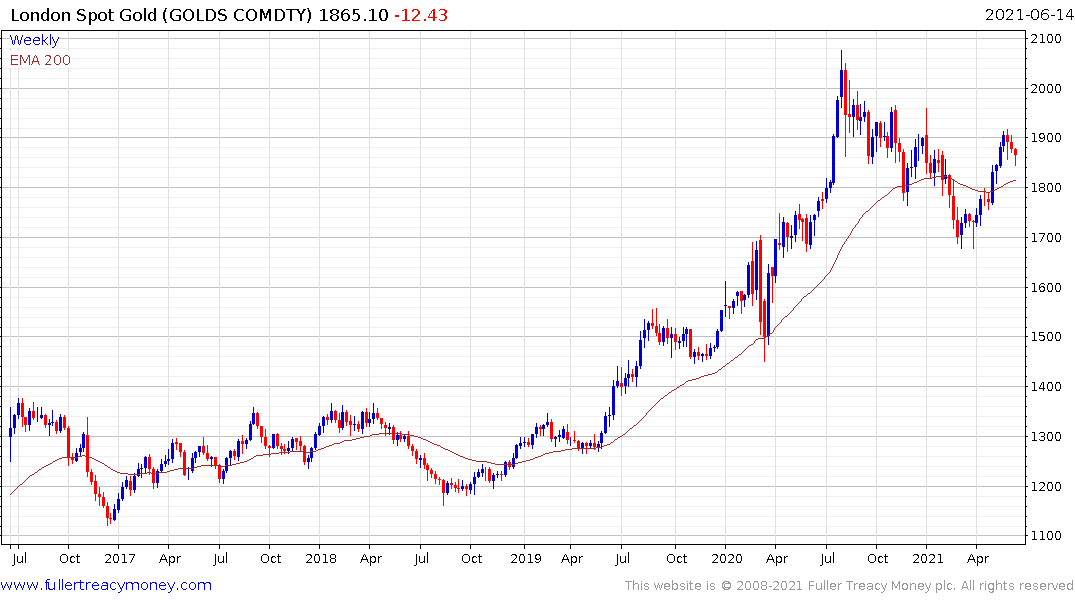

Gold rebounded today from the intraday lows and the region of the trend mean. This is positive action and contrasts with the large downward dynamics posted in November and January. If this pause is limited in nature, it is very supportive of the recovery hypothesis.

Silver remains a relative strength leader and also rebounded impressively from its intraday lows today.