Nature of Crisis Drives Bigger Bailout and Truncated Credit Cycle

This report by Mike Wilson for Morgan Stanley may be of interest to subscribers. Here is a section:

Here is a link to the full report and here is a section from it:

Minsky moment and health crisis elicit extraordinary policy. We believe excess leverage – both in corporate credit and in shadow banking – is why the move has been so ferocious. With forced liquidation now behind us, unprecedented monetary and fiscal support, and elevated equity risk premia, we stick to our view that the worst is behind us and current levels are buying points on a 6-12 month horizon. We're not saying it's a straight line up from here, and a pull-back is likely in order after last week's rally. However, our base case is that the lows are in for this bear market for most stocks.

Debating 2021 earnings. Investors are understandably focused on earnings. 2020 is likely to be substantially below 2019 but we're not as negative as others. Even in a bearish outcome for 2020 EPS (down 20% or more), we think 2021 will see a strong rebound. Benchmarking against the financial crisis, and adjusting for some of the areas of the market uniquely hard hit by this recession, scenario analysis suggests 2021 S&P 500 EPS should reach the $150s. Part of our view is based on our assertion that we have already been in a broad and severe earnings recession. With the government effectively underwriting the labor cycle, operating leverage could be extreme on the other side of the recession.

People are still people. Let’s not forget that. They will still want to go on holiday. They will still eat, drink and make merry and they will still want to get up and leave the house in the morning to go to work, school or to meet friends. That is never going to change.

The Federal Reserve is now monetising vast quantities of debt through a series of programs with the Treasury and these programs are open ended. Liquidity has been the defining characteristic of the bull market since 2009 and access to liquidity continues to drive the rebound from the deep short-term oversold conditions reached last week.

The stock market followed through on the upside today following last week’s upside weekly key reversal which suggests scope for further unwinding of the oversold condition and it helps to confirm a near-term low. The 1000-day MA is the first area of potential resistance and following that the 200-day MA, around 3000 is the next significant technical level.

A recession is largely inevitable considering the decline in the velocity of money. However, over the weekend the swift test developed by Abbott Laboratories greatly enhances scope for widespread testing. With positive results in 5 minutes the potential for activities to ramp back up is being enhanced. That has to be seen as a positive for the wider market because it improves potential for the recession to deep but also short lived.

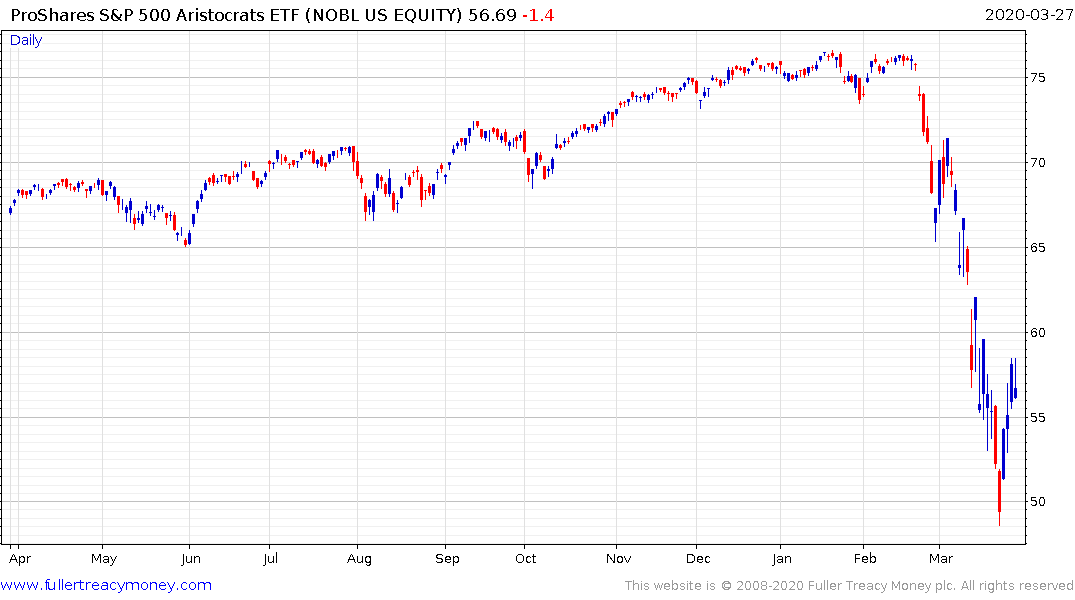

The ProShares S&P500 Dividend Aristocrats ETF (NOBL) has sold off aggressively and many of these shares in the Index have been consistently raising their dividends for decades.